Speculator: Aurelia well supported but is it undervalued?

By Trevor Hoey. Published at Sep 27, 2018, in Opinion Speculator aims to target stocks that tend to fly under the radar, perhaps due to the fact that they don’t suit the risk-averse investor, or simply because they are small, emerging, potentially next big thing stories where the market moving news is yet to break. Finfeed will be looking to uncover such stocks on a weekly basis.

Aurelia Metals Ltd’s (ASX:AMI) share price certainly doesn’t resemble the type of ‘under the radar’ stories that we tend to focus on when identifying Speculator prospects.

In the last six months its share price has roughly doubled from less than 40 cents to recently hit a 10 year high of 79 cents.

It has been an exceptional year for Aurelia as the company transitioned from its established Hera project to a dual asset precious and base metals producer following the April acquisition of Peak Mines.

Management excels at Peak

The successful acquisition of Peak Mines on April 10, 2018 transformed Aurelia into a larger more diversified gold and base metal producer.

The company now has a dominant position in the highly productive Cobar Mineral Field, with two processing facilities capable of producing gold, lead, zinc and copper.

The total purchase payment to NewGold was $93.4 million, however the company acquired the business with a net cash and working capital position of $34.6 million, leading to an effective purchase price of $58.8 million.

Highlighting management’s astute purchase of Peak Mines, net cash flow during the first quarter of ownership was approximately $50.5 million (after capital and tax payments).

The acquisition was funded through $85 million of new equity and a $45 million debt facility. The strong operating performance in the second half of the financial year enabled the company to repay all existing Glencore debt and all debt drawn to fund the acquisition.

As at June 30, 2018, Aurelia was debt free.

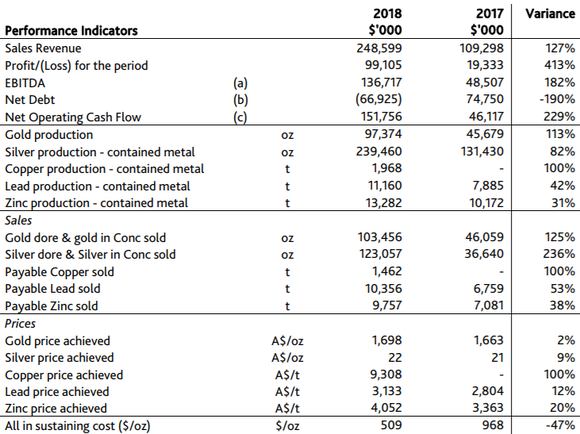

While the following is an impressive set of numbers for fiscal 2018 in terms of revenues, earnings, cash position, production and costs, it is the company’s near to medium-term growth potential that could potentially trigger a substantial rerating.

Aurelia has net cash of approximately $67 million, providing it with the capacity to fund internal projects under consideration such as a lead/zinc process expansion at Peak and copper circuit modifications at Hera, as well as mine development at Great Cobar and Nymagee.

Overall this is an early stage play and as such any investment decision should be made with caution and professional financial advice should be sought.

Premier address with great neighbours

Both Hera and Peak are situated in the prolific precious and base metal producing Cobar Basin region of NSW.

Glencore operates the CSA copper project just to the north of the Peak deposit, and it is worth noting that the global mining giant has a 5.4% stake in Aurelia.

The CSA underground mine produces more than 1.1 million tonnes of copper ore and in excess of 185,000 tonnes of copper concentrate per annum.

The concentrate contains approximately 29% copper metal and is exported to smelters in India, China and South East Asia.

Glencore holds approximately 820 square kilometres of tenements in the local Cobar area.

The company’s presence on the register is likely to increase in significance as a potential share price driver as Aurelia grows its resource at both projects and progresses towards being one of Australia’s most prominent mid-tier precious and base metals producers.

Aurelia’s profile was lifted in September through its inclusion in the S&P/ASX 300 index effective from September 24, 2018.

This no doubt contributed to the recent share price rally (shown in yellow) as savvy investors are aware that the company is now positioned for investment from large fund managers who previously wouldn’t have been able to consider the stock given they are in many cases index bound.

Source: CommSec The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Sustainable low costs and production growth

Both Peak and the company’s flagship Hera project are low-cost multi-commodity producing assets that benefit from silver and base metal credits which drive down the costs of the core gold production operations.

Management’s efficiency in quickly integrating the Peak Gold Mines project has impressed analysts, a factor that has not only cast the company in a good light in recent months, but it also augurs well for the future given that there is substantial scope for resource growth through exploration, as well as the potential for production increases which would be facilitated by expansion of its current plant facilities.

(20min delay)

(20min delay)