RHJ

(A Lengthy) Introduction

...Where I explain why uranium is the place to be

Ever since the global energy transition was accelerated in 2020, we have discussed a wide variety of energy sources, including fossil fuels, renewables, and nuclear energy.

Although I am massively overweight oil and gas stocks, I am a big believer in the importance of clean energy. In this area, I am a fan of nuclear energy.

While I have to agree with critics who say that nuclear reactors are expensive to build, there is no denying that nuclear energy can deliver something (most) renewable energy sources lack, which is significant energy density and supply reliability.

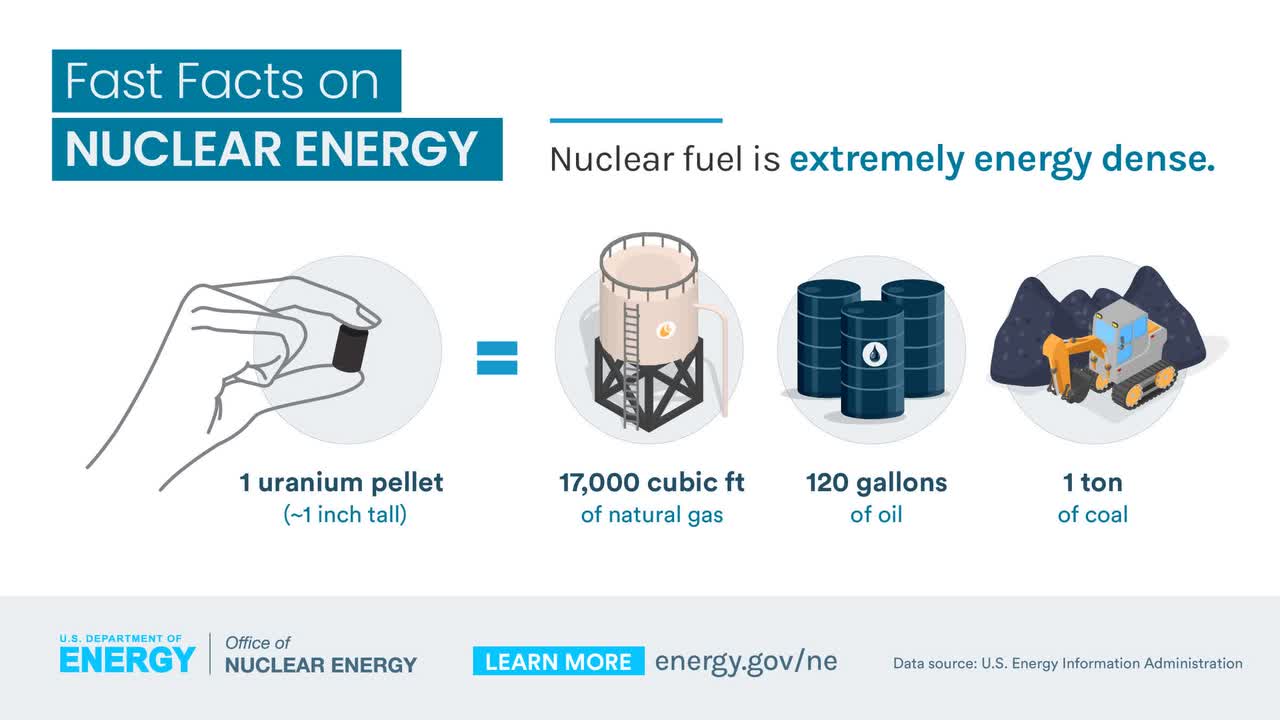

As we can see below, one uranium pellet has the same energy density as one ton of coal, 120 gallons of oil, and 17 thousand cubic feet of natural gas.

U.S. Energy Information Administration

It is also the safest form of energy.

Sure, the Chernobyl disaster and Fukushima are two infamous examples of risks that come with nuclear energy - Fukushima triggered Germany's nuclear energy exit - which have resulted in long-term opposition.

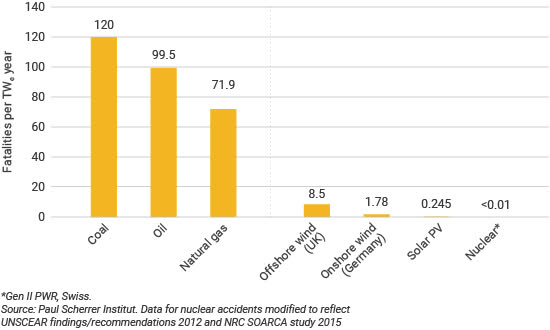

Nonetheless, as we can see below, we see that nuclear energy is even safer than solar, with coal and oil being the most dangerous sources of energy.

World Nuclear Association

Here's a part from the World Nuclear Association report (they may sound biased, but use third-party facts only):

Coal-fired power generation has chronic, rather than acute, safety implications for public health. It also has profound safety implications for the mining of coal, with hundreds of workers killed each year in coal mines (see Appendix).

Hydro power generation has a record of few but very major events causing thousands of deaths. In 1975 when the Banqiao, Shimantan & other dams collapsed in Henan, China, at least 30,000 people were killed immediately and some 230,000 overall, with 18 GWe lost. In 1979 and 1980 in India some 3500 were killed by two hydro-electric dam failures, and in 2009 in Russia 75 were killed by a hydro power plant turbine disintegration. Early in 2017 nearly 200,000 people were evacuated due to the potential failure of the Oroville Dam in California.

So far, so good.

What is happening now is that nations are figuring out that an energy transition solely based on renewable energy is impossible.

We are even acknowledging that oil demand is here to stay, according to OPEC and independent producers.

Bloomberg

That's where uranium comes in, which has rallied extensively in recent years.

According to the Wall Street Journal last month, the "Uranium Rally Still Has Fuel."

In its article, the Journal noted that uranium prices have experienced a remarkable surge in recent times, hitting $92.50 per pound for triuranium octoxide, a form of uranium that is extensively traded.

This surge represents a doubling in price since Russia's invasion of Ukraine in 2022 and marks the highest level seen since 2007.

Wall Street Journal

The primary driver of higher uranium demand is electric utilities.

Contracts for nearly 160 million pounds of uranium were signed last year, representing the highest annual volume since 2012.

This surge in demand has coincided with a tightening of the market, as commercial uranium reserves have been steadily declining in both the United States and the European Union since 2016 and 2013, respectively.

This is great news for producers - not only for obvious reasons.

According to the Wall Street Journal, one notable aspect of uranium as a commodity is its resilience to high prices when compared to other commodities.

Despite the significant increase in prices, demand for uranium remains robust, largely due to its indispensable role in nuclear power generation.

Furthermore, supply risks add another layer of uncertainty to the market. Disruptions in uranium exports from Niger, coupled with production setbacks in major producing countries like Kazakhstan and Canada, pose challenges to supply stability.

Looking ahead, there are expectations that the uranium market could ease somewhat by 2025.

For example, Kazatomprom plans to lift its self-imposed output restrictions by that time, which could alleviate some of the supply constraints.

However, until then, uncertainties surrounding geopolitical tensions and supply disruptions may continue to fuel the commodity's rally.

That's where the Cameco Corporation (NYSE:CCJ) comes in, Canada's largest uranium producer.

My most recent article on the company was written on November 2, 2023, when I went with the title "Up, Up, And Away! Cameco Confirms The Uranium Bull Case."

Since then, shares are up 2%, lagging the market by almost 14 points.

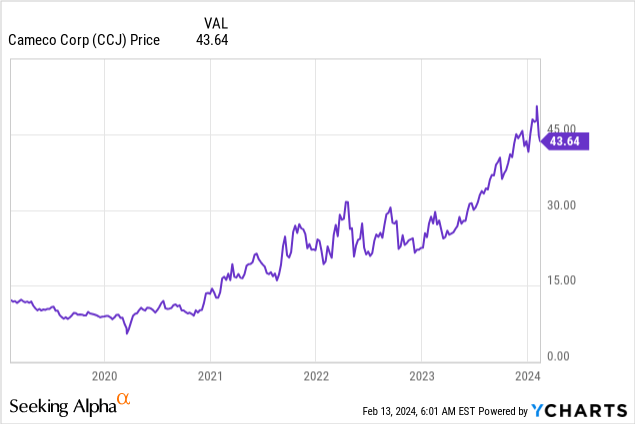

While the recent performance hasn't been great, New York-listed CCJ shares have doubled from their 2023 lows.

Data by YCharts

Data by YChartsIn light of recent developments, including the surge of CCJ's stock price and uranium, I will use this article to discuss the potential future of this company and its industry.

So, after having written one of the longest "introductions" in a long time, let's dive in!

CCJ Remains Well-Positioned For Success

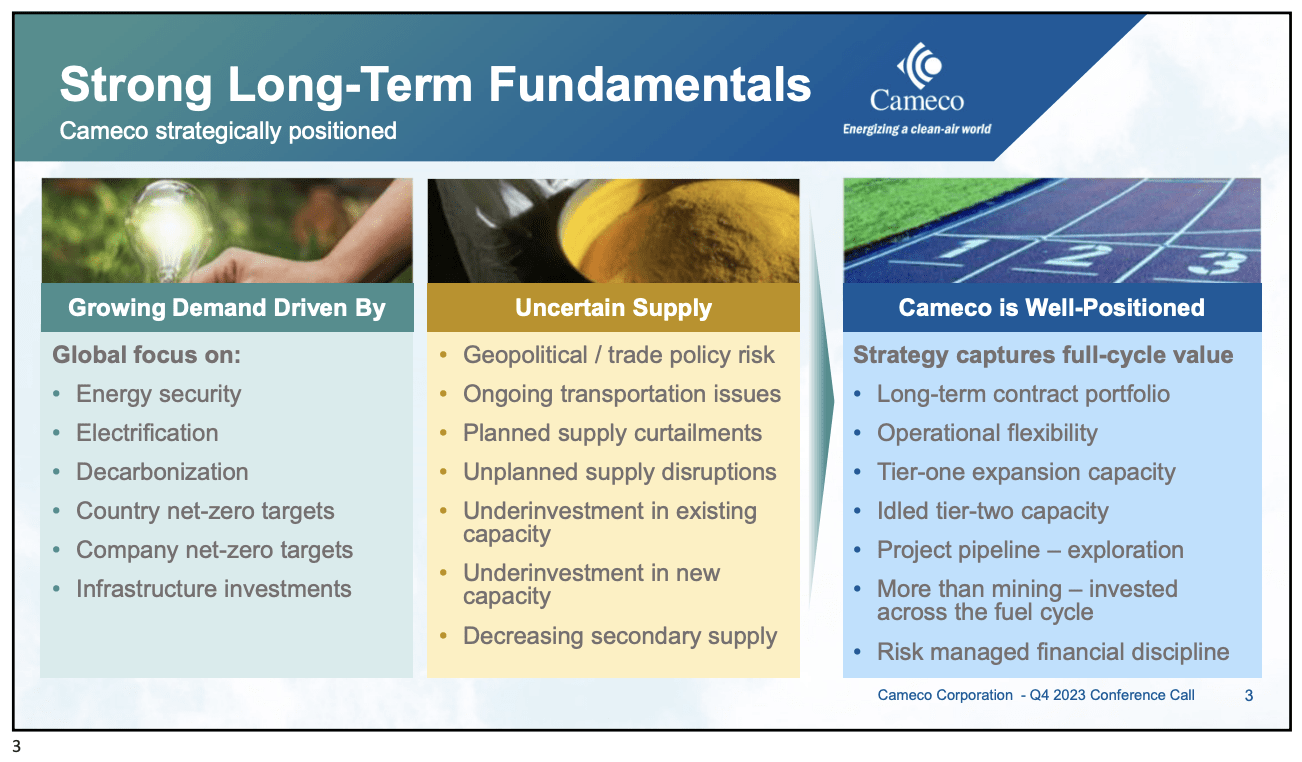

During its recent 4Q23 earnings call, the company updated us on its industry.

The company sees the same developments we discussed in the first part of this article, as the demand for uranium and nuclear fuel is driven by various global factors, including geopolitical tensions, energy security concerns, and climate change imperatives.

Meanwhile, political support for nuclear energy, evidenced by international commitments to expand nuclear capacity, further fuels demand.

Unsurprisingly, this creates a favorable environment for Cameco to capitalize on sustained growth in demand for its products.

Furthermore, the company noted that despite robust demand, the supply of uranium and nuclear fuel faces challenges such as geopolitical tensions, logistical disruptions, and underinvestment in exploration and mine capacity.

Cameco Corporation

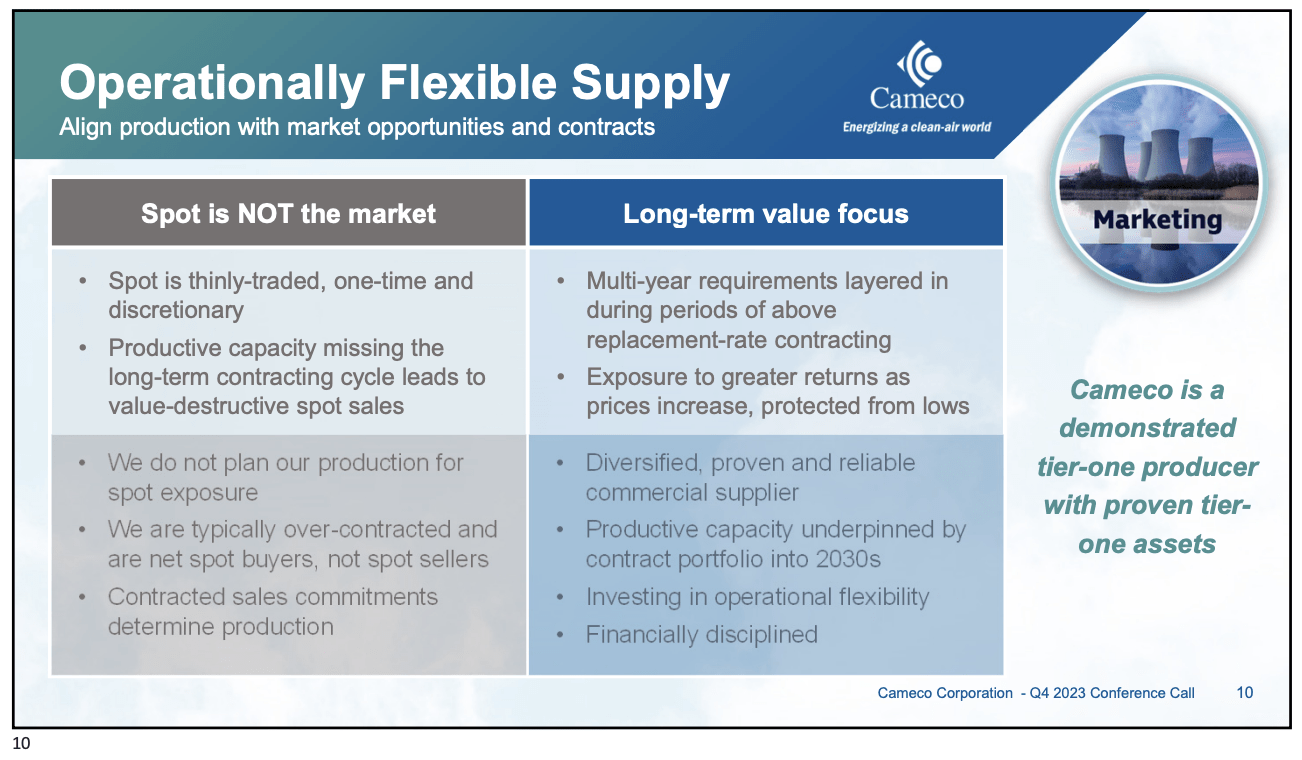

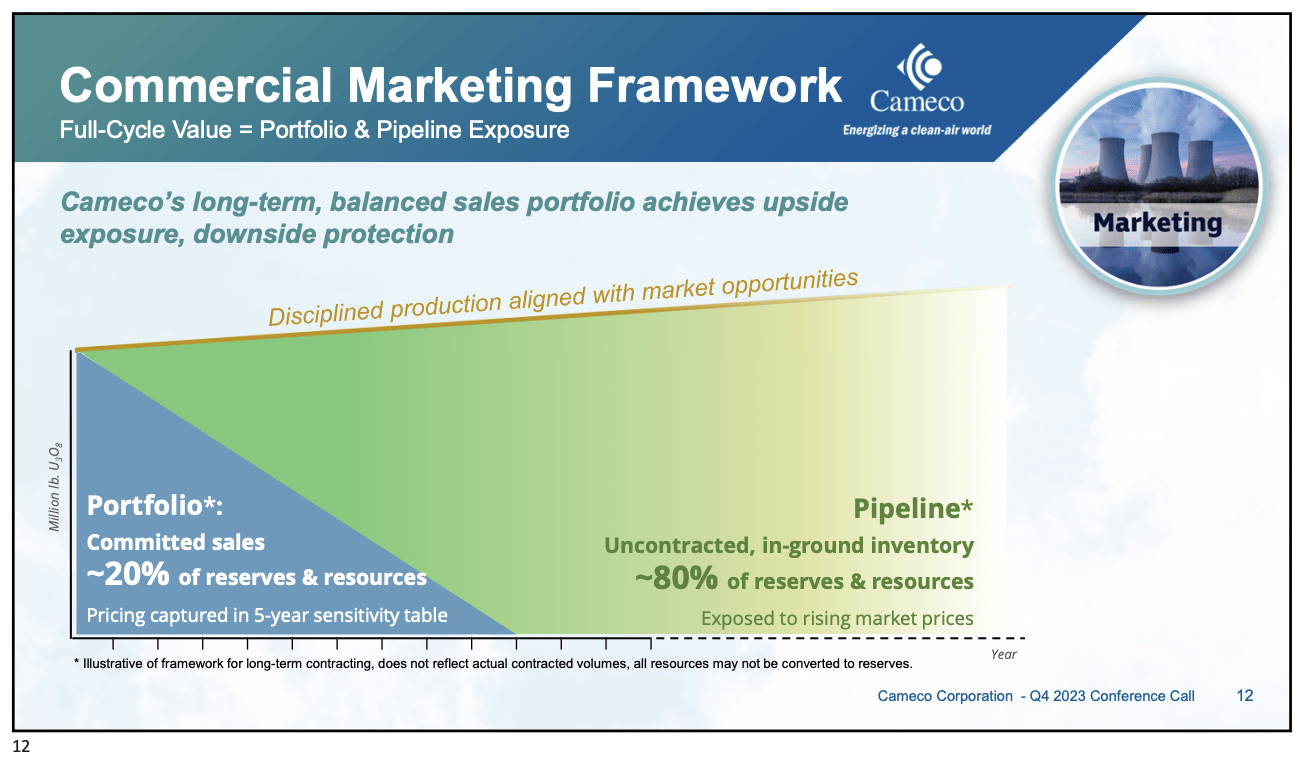

In order to ensure alignment with customer needs and long-term market trends, Cameco employs a multi-faceted contracting and supply strategy.

This includes leveraging production from existing mines, managing inventory levels, and entering into strategic storage agreements.

By optimizing its supply chain, Cameco seeks to fulfill long-term contractual commitments while maximizing revenue and profitability.

Cameco Corporation

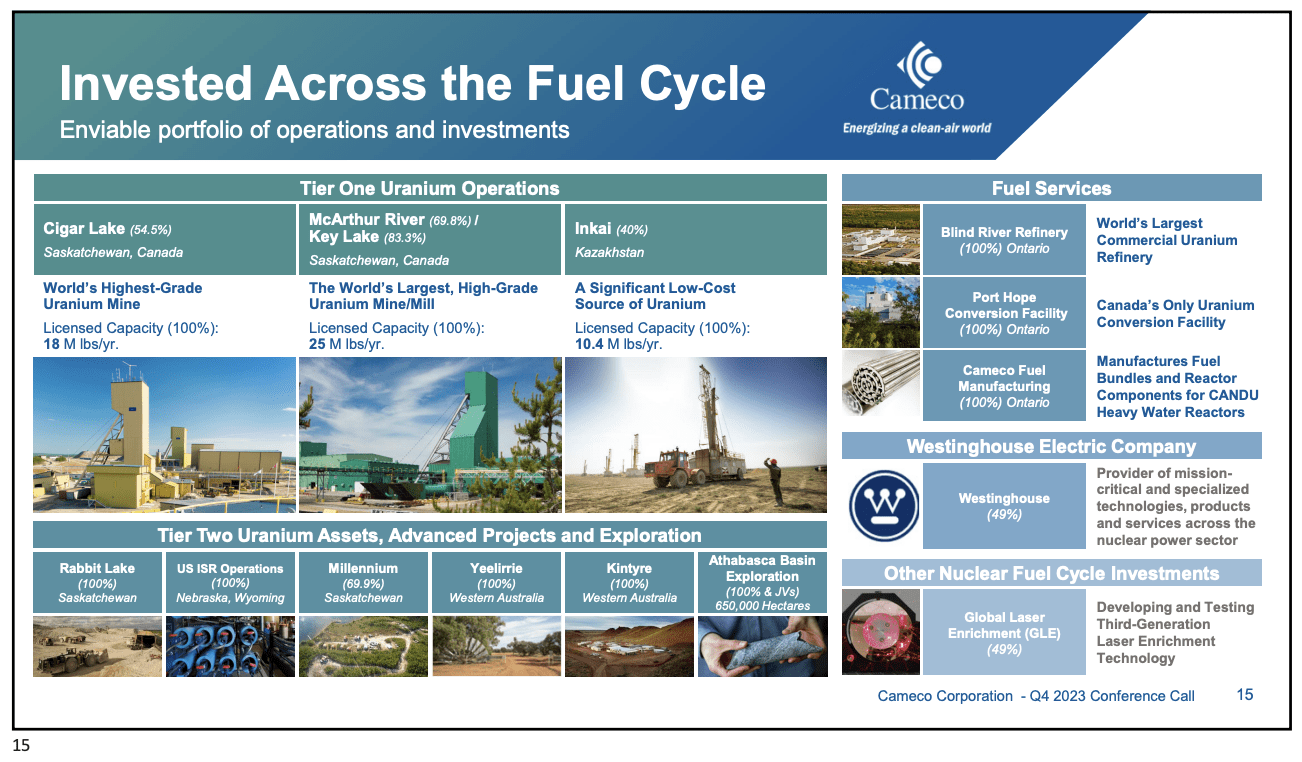

Cameco's growth strategy focuses on expanding Tier 1 capacity, evaluating Tier 2 assets, and advancing exploration activities. This includes investing in capacity expansion projects and exploring new mining opportunities to meet growing demand.

When it comes to contracting, Cameco has a low-risk, high-reward strategy, as its approach ensures it refrains from increasing fuel services production or capacity without securing customer commitments.

This strategic decision positions Cameco to seize market opportunities effectively, particularly amidst customer aversion to Russian supplies.

Cameco Corporation

Furthermore, Cameco announced plans to expand its Fuel Services segment by increasing UF6 production at its Port Hope facility to 12,000 tonnes in 2024, setting a new record production level.

The company's success in securing contracts for UF6 conversion, totaling 75,000 tonnes with 33 customers worldwide, provides a solid foundation for the operation of the Port Hope conversion facility in the coming years.

Cameco Corporation

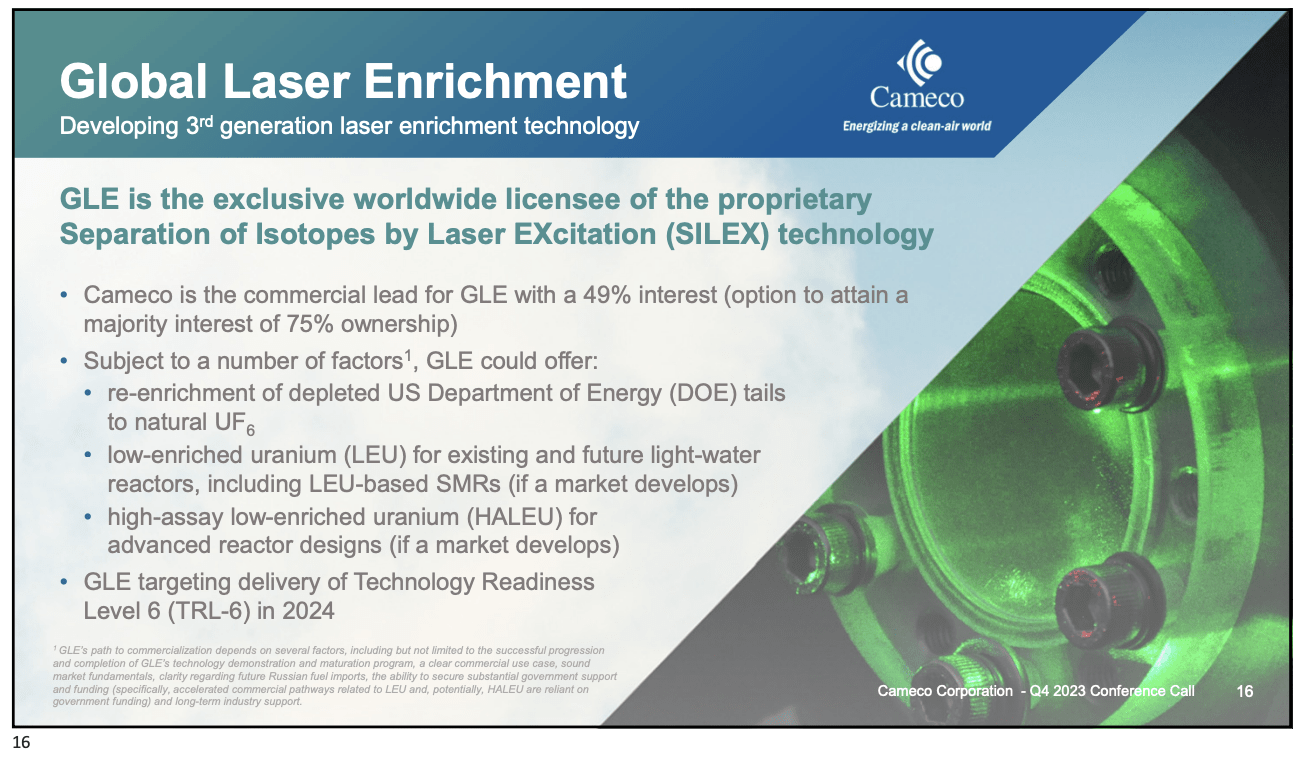

In general, Cameco is diversifying and enhancing its operations. With a 49% interest in global laser enrichment ("GLE"), Cameco supports its commitment to investing in advanced technologies within the nuclear industry.

Essentially, GLE holds the exclusive license to deploy third-generation uranium enrichment technology, offering promising solutions to address evolving industry needs.

From re-enriching depleted uranium tails to producing low-enriched uranium for the global reactor fleet, GLE presents significant opportunities for Cameco to stay at the forefront of technological innovation and meet the changing demands of a market that is quickly turning nuclear energy into an even more efficient source of energy.

Cameco Corporation

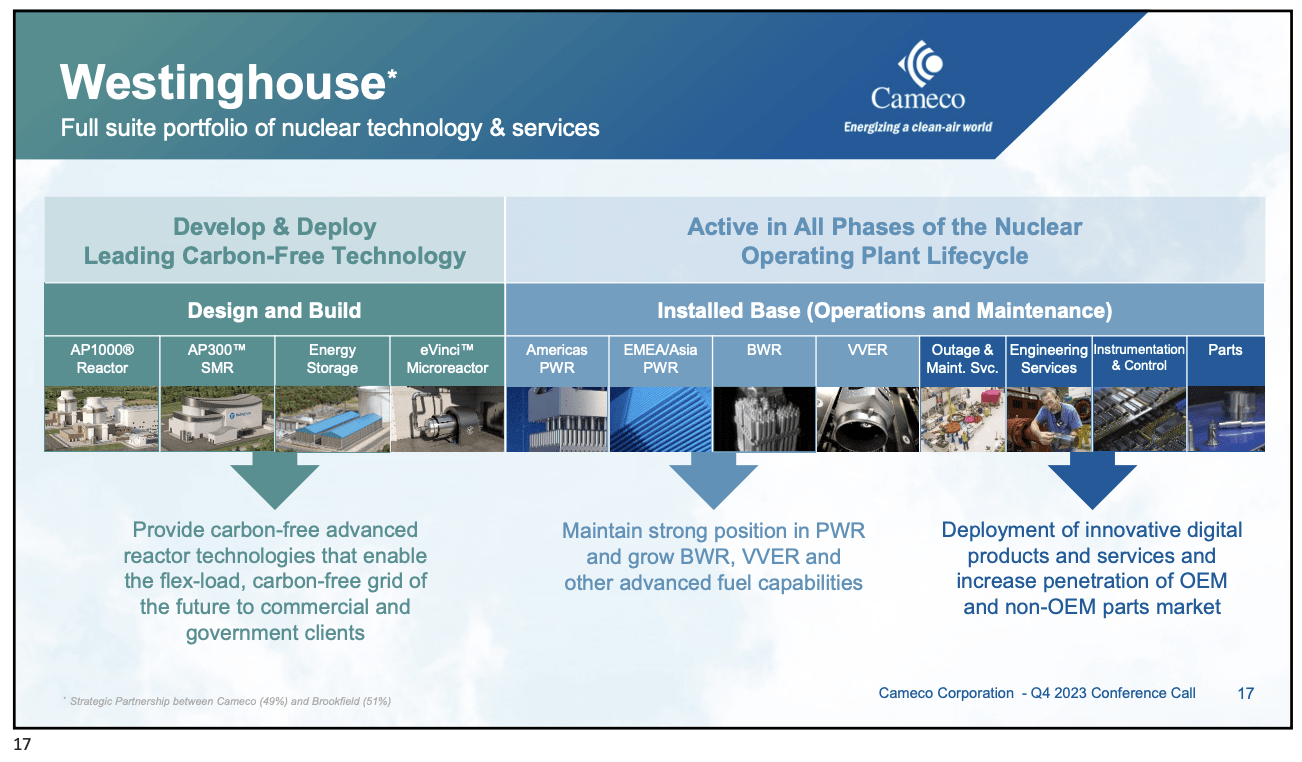

Adding to that, the company's acquisition of a 49% share in Westinghouse demonstrates its strategic efforts toward portfolio diversification.

As we have discussed in prior articles, Westinghouse, a major player in the nuclear power industry, provides exposure to the light water side of the nuclear fuel cycle and offers growth opportunities related to conventional and advanced reactor sales.

This allows CCJ to own bigger parts of the nuclear supply chain as it diversifies beyond basic feedstock.

Cameco Corporation

Even more important is that CCJ is offering investors exposure to this market without elevated financial risks.

In a market where so many younger companies have high-risk business models and poor balance sheets, I like to stick to proven players.

For example, the company anticipates adjusted EBITDA from its recent acquisition of Westinghouse to range between $445 million and $510 million in 2024.

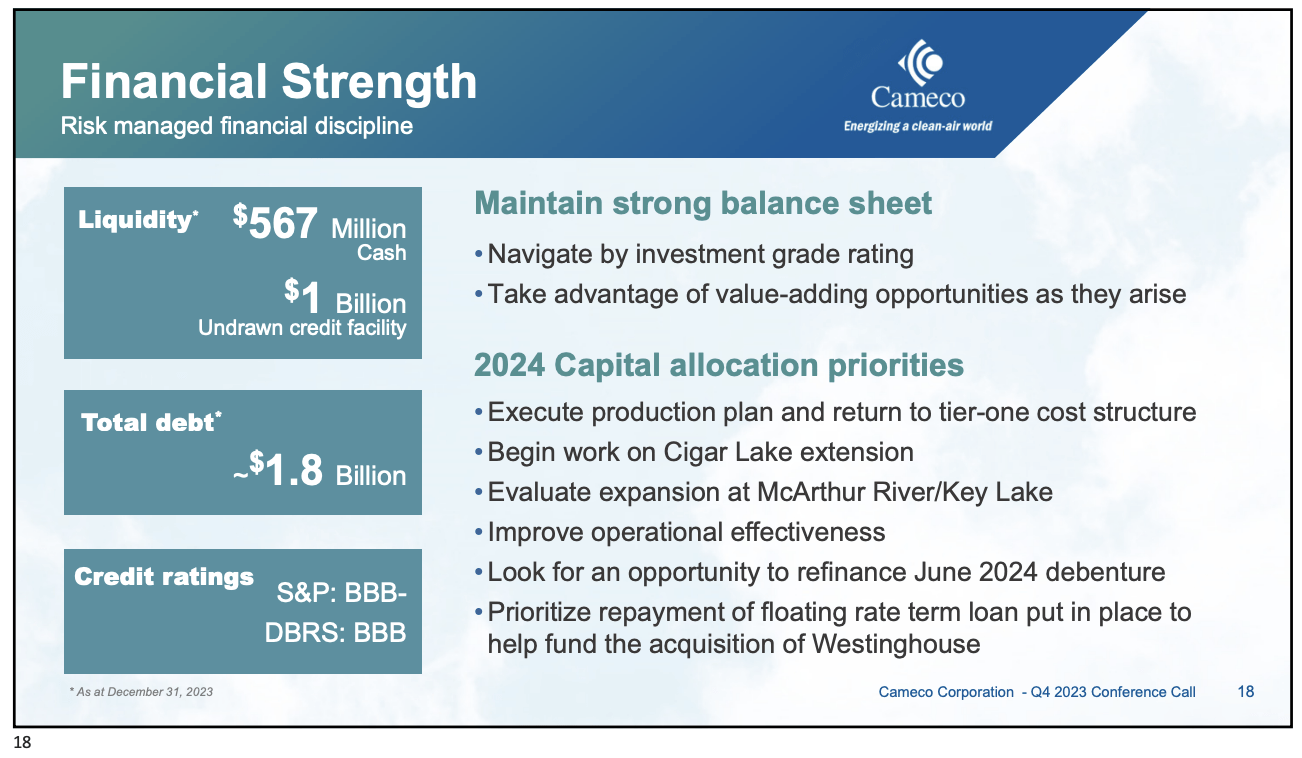

In addition to its projected adjusted EBITDA, Cameco's balance sheet remains robust, with $567 million in cash reserves, which provides the company with financial flexibility to pursue strategic initiatives and capitalize on emerging opportunities in the market.

Cameco Corporation

Moreover, Cameco's undrawn credit facility of $1 billion further enhances its financial flexibility and liquidity, enabling the company to access additional funds if needed for investment or operational purposes.

Adding to that, analysts expect the company to end next year with $1 billion in net cash, which implies more cash than gross debt.

All of this is supported by an investment-grade credit rating of BBB- from Standard & Poor's.

Future Growth & Valuation

Analysts agree with the company's upbeat comments.

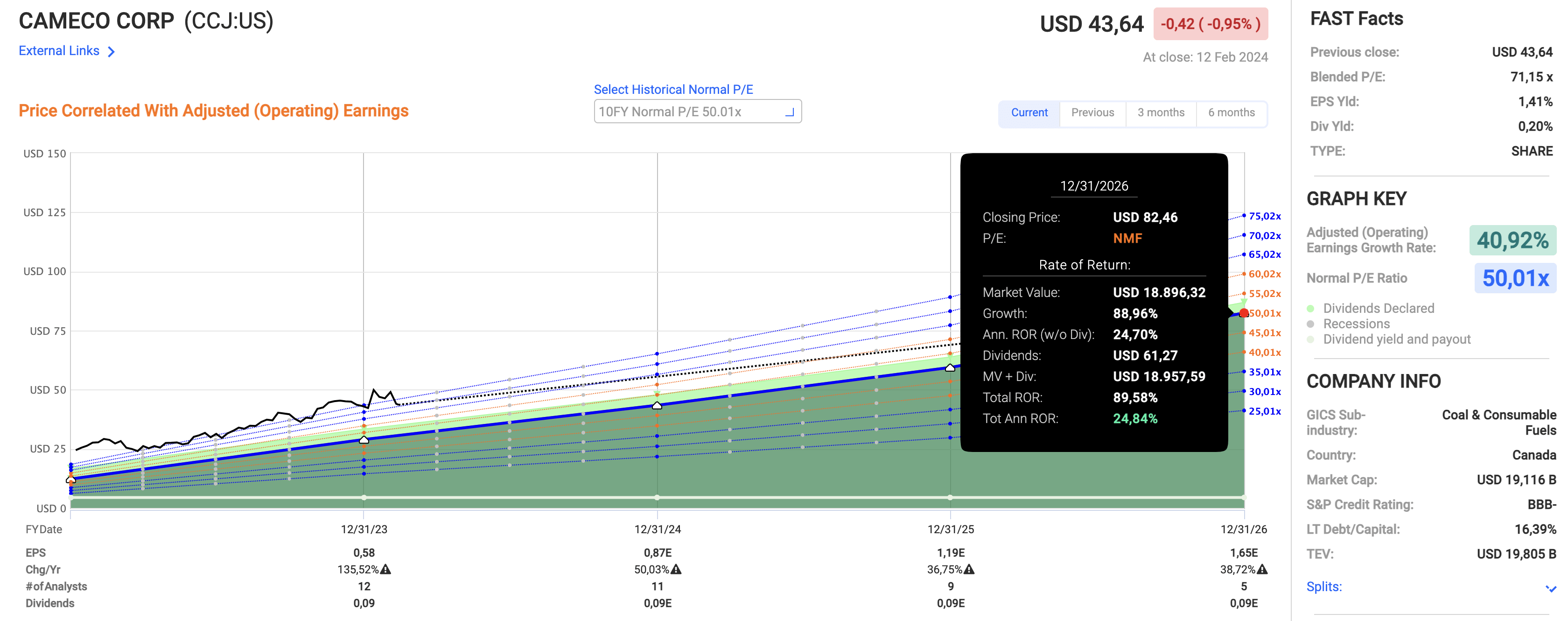

Using the data in the chart below:

- This year is expected to see 50% EPS growth, potentially followed by 37% growth in 2025 and 39% growth in 2026.

- Currently, CCJ trades at a blended P/E ratio of 71.2x.

- While a 71x multiple may seem lofty, even if we give the stock a 50x multiple going forward, it has a 25% annual total return potential if we combine it with expected EPS growth.

FAST Graphs

The current consensus price target is $54, which is 23% above the current price.

Given the favorable bigger picture and its potential total return over the next few years, I believe that my $60 target is still a very valid target.

Takeaway

Uranium's resurgence is undeniable, fueled by a global push for cleaner, more reliable energy sources.

While the path to nuclear power isn't without challenges, it offers unparalleled energy density and safety compared to alternatives.

With uranium prices soaring and demand outpacing supply, companies like Cameco are poised for substantial growth.

By diversifying operations, securing contracts, and investing in advanced technologies, Cameco remains a stalwart in an ever-evolving energy landscape.

With robust financials and optimistic growth projections, investors have reason to be bullish on CCJ's future.

Pros & Cons

Pros:

- Exposure to Growing Uranium Market: With uranium prices surging and demand outpacing supply, investing in CCJ offers direct exposure to this lucrative market.

- Robust Financials: CCJ boasts a strong balance sheet with substantial cash reserves and an undrawn credit facility, providing financial flexibility for strategic initiatives.

- Diversified Operations: The company's strategic diversification, including investments in advanced technologies and acquisitions like Westinghouse, positions it for long-term growth and resilience.

Cons:

- Market Volatility: As with any investment, CCJ's stock price can be subject to volatility, influenced by factors like geopolitical tensions and fluctuations in uranium prices.

- Regulatory Risks: The nuclear energy sector is heavily regulated, and changes in regulations or public sentiment towards nuclear power could impact CCJ's operations and profitability.

- Geopolitical Uncertainties: CCJ's global operations expose it to geopolitical risks, such as disruptions in uranium supply chains due to political tensions or trade disputes.