This is how they are piggy backing on us.Check out the chart below for the ONLY other uranium enrichment technology company on the ASX... Silex Systems.

Silex increased over 3,000% in a 5-year timeframe and now has a market cap of over $1BN:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

With the nuclear power thematic heating up, and a greater focus on the security of supply, we think that the time is now for this technology to be carried forward.

Here are the key points from GUE’s Ubayron update:

- In the next four months: Ubaryon is targeting a transaction “with selected organisations involved in the Nuclear Fuel Cycle production industry” which have “expressed interest in reviewing technology and potentially investing”.

- From late February: site visits are planned for appropriate independent experts to review the details of its technology.

The Ubaryon shareholder update that GUE released on Wednesday says that Ubaryon is confident that the current strategic organisations engaging with Ubaryon can speed up and enable the commercialisation of the technology and a “commercial outcome”.

That could be a valuable thing for GUE which is Ubaryon’s largest shareholder.

We also think that this update is incredibly timely given Trump’s new energy policy stance which has nuclear energy, along with oil as some of its cornerstones.

First though, what’s the “secret sauce” that helped GUE’s peer, Silex Systems achieve a +3000% re-rate?

The Silex Systems story - what would success look like for GUE?

With its 21.9% stake in Ubayron, GUE is looking to become the next “Silex Systems”.

Silex stands for Separation of Isotopes by Laser EXcitation - yes, they actually use lasers to enrich uranium.

GUE’s tech works slightly differently, it is a chemical process of enriching uranium - which if it works, could use less energy, be more environmentally friendly and simplify the enrichment process.

Silex was first listed in 1998, and it has been a long journey for the company to reach its current +$1BN valuation, mainly on the prospect that its laser can help revolutionise what is now a +$6BN uranium enrichment market.

Things started getting interesting in 2006 for Silex though when Silex signed a partnership deal with General Electric (GE)-Hitachi:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We did a deep dive into the history of Silex, and in the simplified timeline below, we’ve noted a few major moments for it:

- 2006: A partnership deal with GE-Hitachi partnership - helped take it from a share price of ~$1 to ~$12.50 in a year (deal terms noted below) (Source)

- 2008: Global Financial Crisis

- 2011: The Fukushima disaster in Japan (by this stage the Silex share price is close to ~$2)

- 2016: An attempt at a deal re-cut with GE-Hitachi - GE-Hitachi had different “business priorities” (Source)

- 2018: Silex moves to abandon the tech and partnership with GE-Hitachi (Source)

- 2019: Deal revived with Cameco where Silex retains a 51% ownership (deal terms noted below) (Source)

- 2022: Ukraine Russia war starts - share price back to ~$1.50

- 2023: Inflation Reduction Act allocates US$700M to enriched uranium - share price at ~$4.50

- 2024: US legislation moves to ban Russian enriched uranium imports - share price at ~$6.60

As you can see, getting uranium enrichment technology off the ground can take many years, but the macro tailwinds have never been stronger for these types of technologies.

We think a mix of investor and government interest will mean capital enters the sector fast enough to speed up the development of enrichment technologies...

And we are betting that GUE’s Ubaryon benefits from these tailwinds.

Why we think GUE’s enrichment technology is well placed

We’re hoping that GUE can move much quicker than Silex in achieving a major re-rate through a commercial outcome for a number of reasons:

- It’s a chemical process and doesn’t require “fancy lasers” (like Silex’s technology does)

- It isn’t encumbered with a commercial partner that has different business priorities (like the GE-Hitachi partnership was)

- Unlike Silex, GUE hasn’t had to navigate the GFC (2008) and Fukushima (2011), and as far as geopolitics go, the case for nuclear power and uranium is much stronger now than it has been in decades

Back in June 2024, GUE announced that its enrichment technology had achieved “a separation factor approximately three times higher than the enrichment factor.”

An “important measure for commercialisation.”

Read more about GUE’s stake in an enrichment technology partner in the article below:

GUE: Uranium enrichment technology achieves 3x “separation factor” in enrichment process

Enrichment tech is crucial to energy supply

The markets interpreted that the recent kerfuffle around the new Chinese AI model “DeepSeek” would reduce forecast AI power demand (and thus nuclear demand and uranium demand).

The uranium price did soften a little bit BUT is still at 14 year highs.

Longer term, this is about geopolitics and competition by great powers for control of energy supply in the uranium and uranium enrichment market, as well as the long term demand for nuclear power and uranium as a way of decarbonising as more reactors come on line.

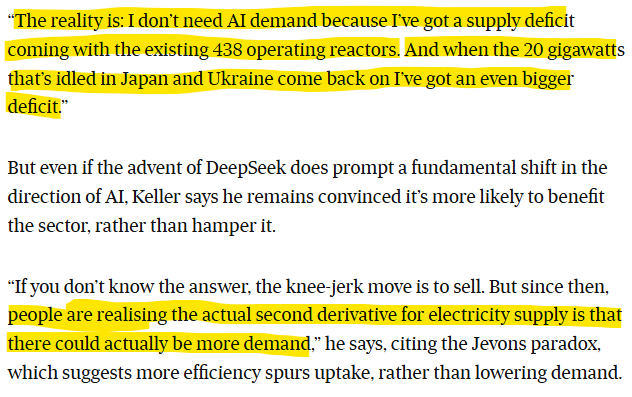

Guy Keller of Tribeca Investment Partners recently noted that the AI debate may not be material to the longer term picture for nuclear power and uranium:

(Source)

We think that’s an excellent point.

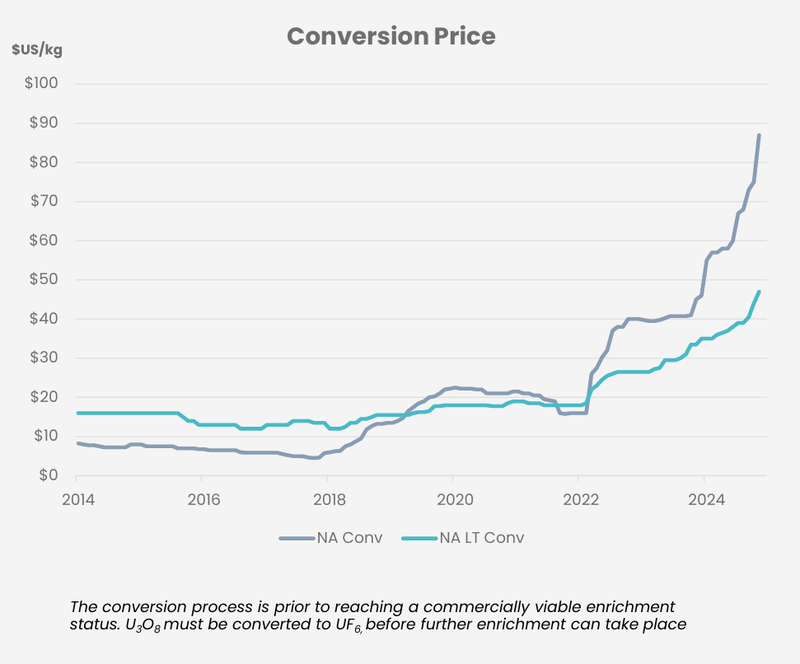

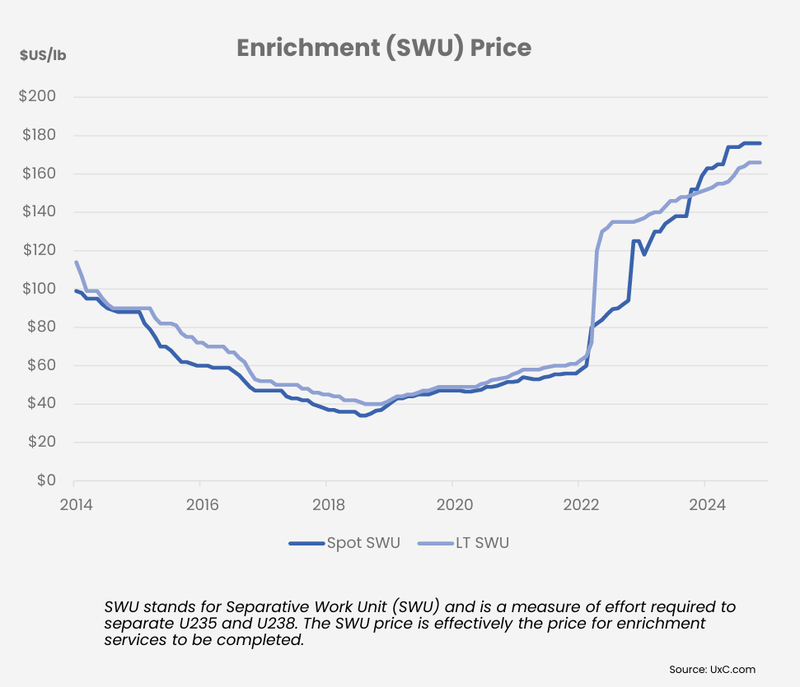

And then of course, there are the current uranium enrichment market fundamentals which we think could drive any potential negotiations that GUE’s Ubaryon enters into.

Have a look at the costs of conversion (where yellowcake is converted into a gas) and enrichment prices from a recent GUE presentation:

(Source)

That looks like the start of a pretty aggressive trajectory.

So that's the price to consider - but there’s also geography involved as well.

That is, which countries hold the largest share of the uranium enrichment market.

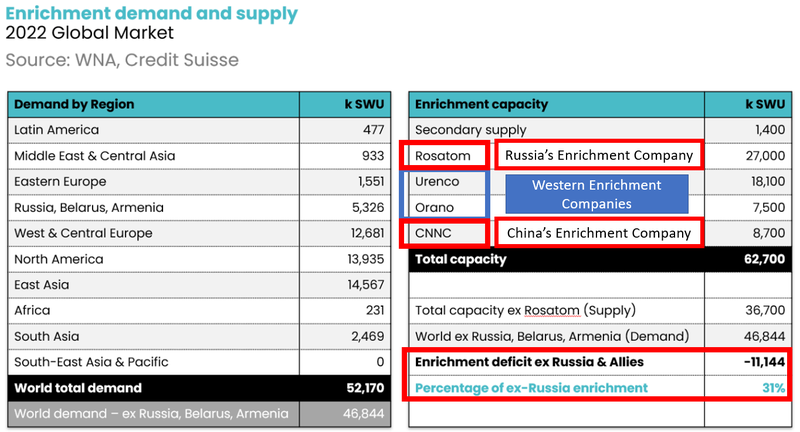

In our initiation note (read it here, note: at the time GUE was called OKR), we mention that the enrichment market is dominated by Russia and China.

Below is a quick summary of the companies that have enrichment capacity in the world matched up against sources of demand:

Quick takeaway: As of 2022, Russia and China dominate the global uranium enrichment market with a combined 63% of global capacity - and there’s a big squeeze going on in the West for enrichment capacity.

We think Silex’s current +$1BN valuation is based on the fact that its technology has the potential to revolutionise or dominate a growing +$6BN uranium enrichment market.

Deal terms are important here for Silex, as we anticipate they will be for Ubaryon (of which GUE is the largest shareholder with a 21.9% stake).

Silex has a 51% stake in a JV with Cameco, and importantly the agreement that Silex struck in 2019 with Cameco sees it retain a perpetual 7% royalty.

(Source 2019 Silex-Cameco JV Announcement)

The Silex-Cameco JV also includes access to a large ~300,000 metric ton uranium tailings facility in Kentucky, USA, which assuming the Silex technology works at scale, is equivalent to a Tier-1 uranium deposit with a ~40 year mine life according to previous Silex announcements. (Source)

All of this, we think points to potential valuation upside for GUE based on its current market cap of $25M and its 21.9% stake in Ubayron (not to mention its existing ~52Mlbs of uranium resources and its ambition to grow that to +100Mlbs).

While the technology is a black box, as it remains heavily regulated and subject to the most stringent government controls, the Silex story gives us some good clues as to how much the market values enrichment technologies.

In other words, we just can’t know exactly how “good” it might be.

So the site visits conducted in late February (this month) will further confirm to independent experts just how good it is.

Then we hope that Ubaryon, as part of its strategic partnership planning, can secure a good commercial outcome for themselves (and by extension, their largest shareholder in GUE) with any negotiations.

The proof will be in the pudding, as they sa

This is how they are piggy backing on us. Check out the chart...

Add to My Watchlist

What is My Watchlist?

(20min delay) (20min delay)

|

|||||

|

Last

$4.01 |

Change

-0.100(2.43%) |

Mkt cap ! $954.8M | |||

| Open | High | Low | Value | Volume |

| $4.10 | $4.11 | $3.91 | $3.919M | 977.4K |

Buyers (Bids)

| No. | Vol. | Price($) |

|---|---|---|

| 1 | 12315 | $4.01 |

Sellers (Offers)

| Price($) | Vol. | No. |

|---|---|---|

| $4.05 | 4987 | 1 |

View Market Depth

| Last trade - 16.10pm 18/06/2025 (20 minute delay) ? |

| SLX (ASX) Chart |