weible1980

Investment thesis

I am bullish on (NYSE: NYSE:CCJ) from the uranium production angle, where the company plans to produce over 22.4 million pounds of Uranium in 2025.

CCJ

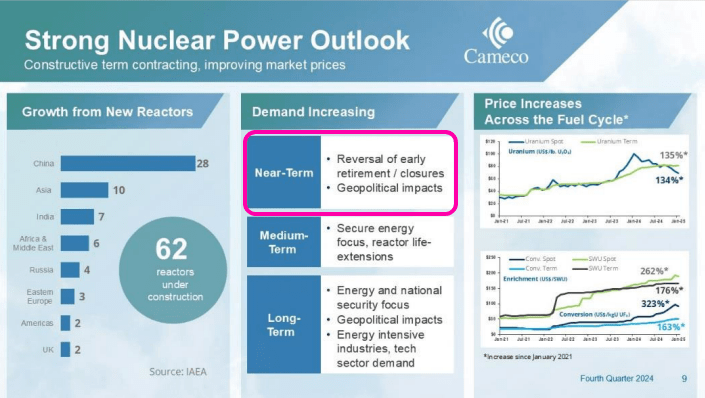

By looking at the production of Uranium by Cameco, I am convinced that despite the reduced Uranium production guidance from a total of 23.4 million pounds in 2024 to 22.4 million pounds in 2025 from its major production mines (McArthur River/Key Lake and Cigar Lake), the company has a high bullish potential. The company has executed varied contracts that position it to sell over 220 million pounds to 41 customers globally. However, the western region, America at 44% and Europe at 39%, takes the largest share of its customers, 83%. With only a small customer base in Asia at 17% and adding the ban on Russian uranium imports into the US in the picture, Cameco has a high bullish potential from Western dominance. At the new record high uranium production hitting 20.3 million at McArthur/Key Lake, surpassing any global mining operation, Cameco is best positioned to supply the most Uranium to Western utilities. Digitization and automation optimization of projects at the Key Lake have played a key role in this success.

I am also considering Cameco's edge in uranium production and its commitment to exploring reactor and fuel supply. This adds an aspect of engineering, operating, and maintaining the development of new reactors. At the moment, in terms of Uranium production, there are only 3 entities that match Cameco production in the western region. Its competitors in terms of Uranium production are Russian Rosatom, which has been barred under the Russian uranium import ban, China Atomic Authority, and French Orano. Orano faced challenges at their SOMAIR mine in Niger following the coup d’état in July 2023, and China Atomic Authority faced Tariffs and other geopolitics challenges that best positioned Cameco for the western region market. I have explained in more detail my basis on why Cameco is bullish, looking at its uranium production capacity and its market dominance in uranium supply in the western region.

Company brief

Cameco is a uranium production company based in Saskatoon, Canada. Uranium production is mainly used to generate electricity. The company operates three segments: Fuel Services, Uranium, and Westinghouse. The uranium segment focuses on mining, milling, and purchasing and selling Uranium. The Fuel Services segment converts, refines, and fabricates uranium concentrate, purchases, and conversion services. Westinghouse segment operates nuclear reactor technology and originally manufactured equipment and provides products and services to government agencies and commercial utilities. The company also provides engineering services around nuclear utilities, such as instrumentation, maintenance, plant modification, and engineering support.

Cameco has an edge in Uranium market growth

Let's first look at the global perspective of nuclear energy demand and later market Cameco, which is dominating. On a global scale, the demand for nuclear power in 2024 was USD 435.54 giga-watts. In 2025, nuclear power is estimated to hit 2.76tn kWh globally at a CAGR of 1.56% between 2025 to 2029. This increase is driven by the increased uptake of energy-sustainable generation sources, leading to the nuclear sector regaining its interest due to the low carbon it emits.

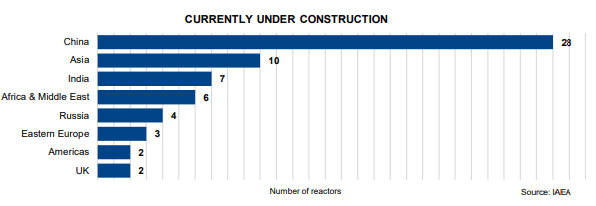

While China is leading in the number of installed large-scale reactors, Cameco still has 17% sales in Asia.

CCJ

In Eastern Europe and the UK, large-scale reactors have declined from 34% in the 1990s to 23%, necessitated by running and maintenance costs. This decline is matched with efficient, cost-effective nuclear energy models known as SMRs, the new generation of reactors. SMRs are the new catalysts of nuclear energy, and the plan is to marry maturity up to 25GW capacity.

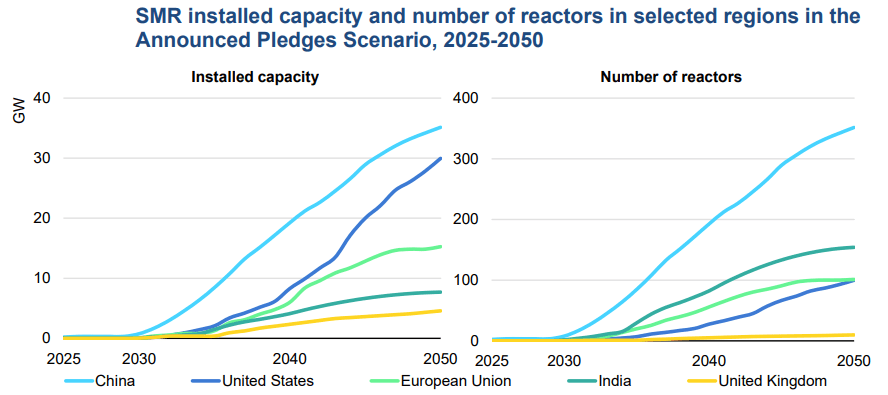

The growth of nuclear power adoption by data centers is still solid, going by the projected SMR capacity to hit 40 GW by 2050. The United States is leading in SMR research at 35%, and Europe is expected to account for 15% between 2025 and 2030. The growth of nuclear energy driven by SMRs and varied advanced nuclear reactors plays a key role in low carbon energy supply, which is an added advantage. For example, in the northeast of the United States, data centers are driving electricity demand. On the other hand, in Europe, electricity demand is accelerating rapidly, and a case in point shows that in 2022, 17% of Ireland’s total electricity was used on data centers. This consumption in Ireland is expected to double by 2026.

Based on my thoughts above, my pick on the western uranium market as a solid market for Cameco is based on the projected SMR installed capacity between 2025 and 2040.

International Energy Agency

From this take on the SMR evolution of uranium usefulness, I hope you note that since uranium production is the core of the Cameca business, it has an ample productive capacity to meet the demand of expanding nuclear energy and fuel needs. For example, Tier-one operations in the McArthur River mine/Key Lake mill have estimated reserves of 251.0 M lb in its estimated mine life by 2044, when the SMRs are expected to skyrocket.

Clearly, Cameco is prepared to meet the demand for uranium projected by the SMR revolution and other nuclear reactor technologies. This goes with Cameca Management Discussion and Analysis forward-looking statement on SMR to participate in SMR commercialization and deployment among other fuel cycle value chains.

Financials: Annual and Q4 highlights shows optimistic signs

The company has strong financials, with annual net earnings hitting $172 million after cash from operations generating $905 million. This delivered an adjusted EBITDA increase of 73% from $884 million in 2023 to $1.5 billion in 2024. Westinghouse recorded an adjusted EBITDA of $483 million from $101 million in 2023. However, the full year recorded a net loss of $218 million attributed to inventories revaluation on market prices compared to the acquisition time.

For the quarter, the company recorded net earnings of $135 million, an improvement from $80 million in net earnings in Q4’23. This delivered an increased adjusted net earnings in the quarter from $90 million in Q4’23 to $157 million adjusted net earnings.

The company continued to generate value for its shareholders with an increased annual dividend at $0.16 per common share in 2024 from $0.12 per common share in 2023. From the company's promising business, it expects an increase of $0.4 per common share in 2025 and 2026, achieving a double-digit dividend in 2023 from $0.16 to $0.24 in 2026 per common share.

Analysts estimate the Cameca projection of double-digit EPS of $0.24 in 2026 to be achieved in the next quarter, June 2025, and the yearly EPS will hit between $1.26 and $1.7. Going by the near-term risks such as geopolitical issues, the company may likely not achieve the analyst's estimates, but it is poised for this performance in a perfect or ideal business environment.

CCJ

The company also has a strong balance sheet with available cash liquidity of $600 million and a $1 billion undrawn credit facility. The prices of Uranium are forecasted to rebound mid-2025 to around $90-$100 per pound, so Cameco expects more cash flow in 2025. The company also made the final repayment of $200 million in credit used to finance Westinghouse, and the loan is now fully paid. This reduced the company's debt burden to the current $1.3 billion. This good credit score is seen in the 5.88 Altman Z score, which is above 3, which means that the company has a strong going concern aspect and is not becoming insolvent in the near future.

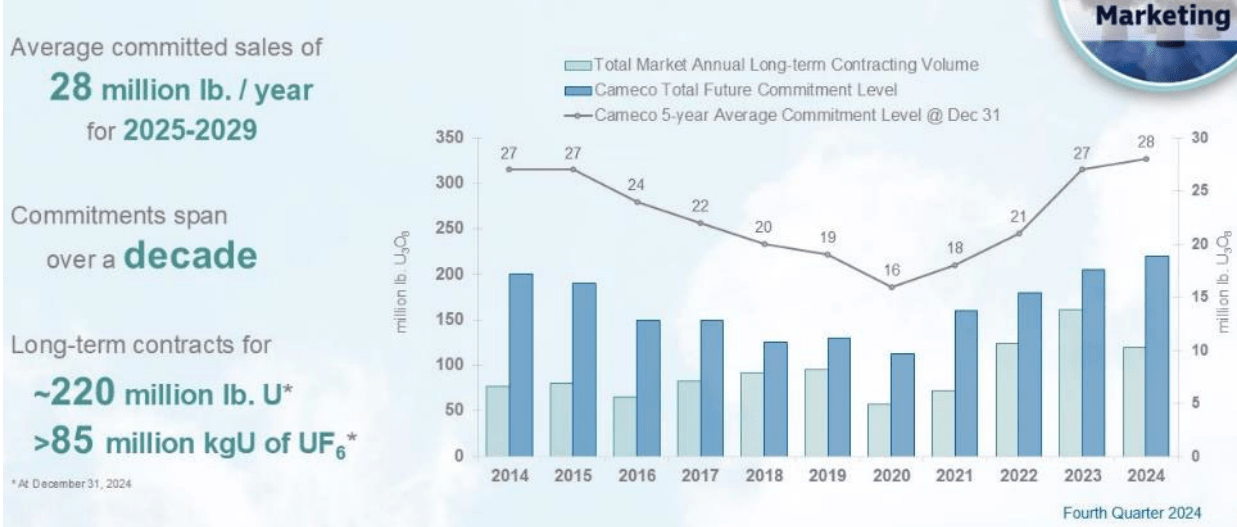

I am also optimistic, following the strong uranium contract portfolio. The company closed Q4’24 and FY 2024 at 220 million pounds. The breakdown is 28 million lb/year between 2025 to 2029.

CCJ

Valuation

From the financials above, I have noted that the company estimates EPS improvement, and analysts’ forecasts EPS projection reveals optimism. From this context, I value Cameco using cash flow from operations and its Price-to-earnings (P/E) ratio (EV/EBIT). This is amongst its competitors Uranium Energy Corp (NYSE: UEC), Energy Fuels Inc (NYSE: UUUU), and Centrus Energy Corp (NYSE: LEU).

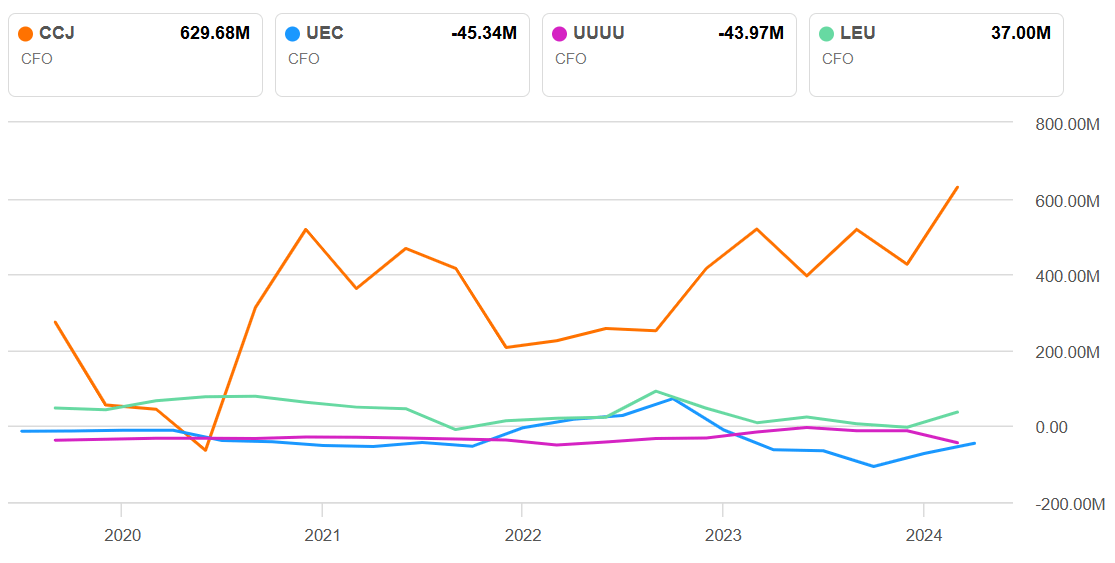

Cash from operations shows the following:

Seeking Alpha

This reveals that CCJ is leading amongst its competitors in cash generated from its operations. The difference from $629.68 million to the second company, LEU, at $37 million indicates Cameca's lead in selling Uranium.

Also, Cameco's P/E ratio will show whether its current price matches its earnings. Using EV/EBIT, the competitors demonstrate the following:

Seeking Alpha

At the current dip, Cameco is not overvalued at a P/E ratio 52.75. Instead, the company is setting high expectations for its future growth. The high P/E ratio amongst its competitors shows investors are willing to buy its shares at a premium. This explains why the company has a positive EPS and projection of a double-digit EPS of $0.24 per common share by 2026, which shows the high expectation. This confirms why I am reiterating Cameco's optimism.

Investment risks

- Geopolitical risks – Despite the ban on Russian Uranium from entering the US, the current tariffs by the US on Canada, China, and other listed nations are likely to halt Cameco operations.

- Fluctuating currency exchange – the company could be adversely affected by changes in currency rates due to royalty rates, tariffs, inflation, and interest rates. This would affect the performance of company financials.

- Regulatory risks – risks associated with 1the inability to enforce company legal rights under the current agreements, licenses, and permits may delay mining operations.