These a-holes keep getting air time

https://roguefunds.substack.com/p/asp-isotopes-technology-is-provenQuantum Leap Energy (QLE)

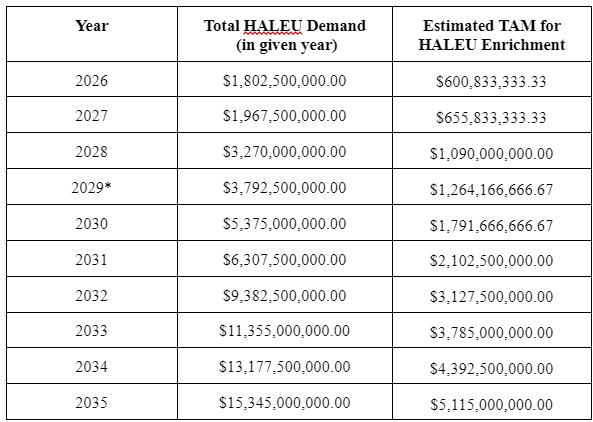

In my first blog post on ASPI, I discussed the market possibilities of HALEU intensively. I will utilize some of the things I have already said here along with new information while also trying to keep the scope to the immediate 3-5 year future. Lets bring back the chart I used in that post showing US HALEU demand:

Obviously these numbers are very hard to guess because we don’t actually know what the actual TAM of HALEU is right now. Companies such as Natura and Rolls Royce are using LEU+ to make up for the fact that there is no supply of HALEU but if there were to be a steady supply their commercialization of their reactors, we would most likely see them switch to HALEU. We also don’t know what type of demand we will see outside of the US which makes this even more intriguing.

QLE believes they can be profitable well below $10,000/kg implying gross margins of well above 70% at current prices (these get crunched considerably when considering the structure with ASP Isotopes). QLE will be able to produce enough HALEU to address all global needs. This implies a revenue of $500m at $25k/kg for a 20 MTU plant. This amount will be rapidly ramped up based on additional HALEU facilities in the UK (which should begin working on the license process in 2024/2025), South Africa (which should be licensed this year), and the US (TBA).

The initial facility will be able to process 20 mt of uranium by 2027 but this can be rapidly expanded or reduced due to the modular plant construction model of their facilities. Management is under the impression that they will be able to meet all HALEU demand by 2028 of 100+ mt of uranium per year. Management believes they can produce a 750,000 SWU facility (20 mtu) for $100mm. This blows out current ROC for centrifuges which usually cost $1b per 1mm SWU. Absolutely no one in the industry can compete with this with ROC.

The company believes that due to their high selectivity they will be able to reuse nuclear tails from past enrichment to create HALEU. No other company will have this ability (Silex says at best they will be able to produce LEU from this waste not HALEU) so the odds of others competing on price is unlikely. Most companies will give them this uranium waste for free or might even pay them to take it. This should allow them to produce HALEU at highly competitive prices with extremely large margins. Without depleted tails, operational costs are almost identical with centrifuges.

Competition

Centrus

Need about $4b to produce 4mm SWU worth of HALEU which is roughly 100 MTU of HALEU

Will be using centrifuge technology.

Haven’t produced contract for 900kgs of HALEU yet.

My best estimate is they won’t be producing truly competitive quantities of HALEU until 2032, if ever. They will need quite a lot of debt and if QLE is already supplying the market I am not sure how they will get it.

Has to created high risk, highly enriched uranium in the US which means it will be highly regulated.

Valuation of $1.4b with inevitable dilution and debt coming.

Rosatom

They can already produce some HALEU but the US and most countries will be looking to diversify away from Russia.

Their main focus is LEU and do not have enough HALEU production to supply the current market needs.

Centrifuge Technology.

Need about $4b to produce 4mm SWU worth of HALEU which is roughly 100 MTU of HALEU

LIS Technology

Will most likely be the only true competitor in ~10 years.

CRISLA only has a selectivity of ~2 but stages can be cascaded very easily.

$/SWU will be cheap but most likely can’t compete on higher SWU isotopes.

Currently at a TRL of 4.

Trying to enrich in the US via a new technology that has high proliferation risks will be an up hill battle.

Inventor of the technology is wanting to retire and is extremely old (Jeff Eerkins).

Tech is nowhere near being proven at a commercial level and then production plants will have to be built out. Production at the earliest will most likely be 2032.

Urenco

Behind schedule for HALEU (so much so that the NRC has publicly called them out for it).

Currently building an extremely small plant in Europe for HALEU by 2031 but I question both the timeline and the willingness to commit capital to this.

Silex

I am including Silex here because most individuals believe Silex will be producing HALEU before 2035. Per Silex’s CEO their sole focus will be on LEU before 2035. Silex is NOT a realistic competitor in HALEU.

Add to My Watchlist

What is My Watchlist?

(20min delay) (20min delay)

|

|||||

|

Last

$3.22 |

Change

-0.330(9.30%) |

Mkt cap ! $766.7M | |||

| Open | High | Low | Value | Volume |

| $3.42 | $3.45 | $3.12 | $7.674M | 2.386M |

Buyers (Bids)

| No. | Vol. | Price($) |

|---|---|---|

| 1 | 310 | $3.20 |

Sellers (Offers)

| Price($) | Vol. | No. |

|---|---|---|

| $3.22 | 2017 | 1 |

View Market Depth

| Last trade - 16.10pm 13/06/2025 (20 minute delay) ? |

| SLX (ASX) Chart |