Oil Search (OSH)

Company and quality overview: Oil Search, in partnership with ExxonMobil, is the leading Papua New Guinea LNG producer. The company has generated nearly USD2b in free cash-flow since the commissioning of its large-scale conventional gas and condensate PNGLNG project in 2015. The company has large growth opportunities both within PNG and Alaska, in order to take advantage of a shift toward less carbon-intensive sources of electricity generation.

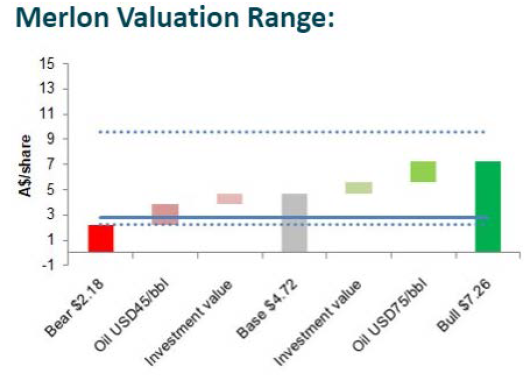

Valuation & market reasoning: We value OSH at AUD4.72/share, within a range of AUD2.18-7.26 per share, based on its sustainable free cash flow under a range of scenarios. The stock is trading towards the bottom end of this range, with the market concerned about the impact of COVID on near-term oil prices (via weak demand) and political uncertainty in PNG. OSH also has reasonably elevated debt, despite raising capital earlier in the year.

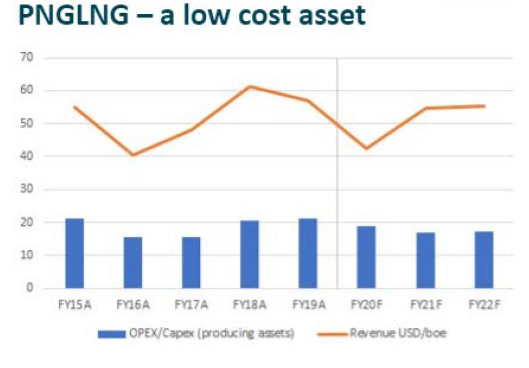

Merlon view: Lower oil prices in the short-term typically lead to deferred investment in production capacity, resulting in a decline in supply, and price normalisation. We see upside to this price from a phase of underinvestment in conventional oil and gas globally, and more recently across US unconventional oil and gas activity. At current oil prices, OSH continues to generate positive cash-flows, as at USD21/boe, OSH costs are highly competitive.

Ampol (ALD)

Company and quality overview: Ampol is the leading Australian supplier of petrol and diesel product. The company has a sizeable commercial business, accounting for 50% of total volumes, combined with a one-third retail market share position, via 700 company owned and operated sites, and supply agreements to non-owned Ampol-branded sites. The industry structure is highly favourable with the top three operators supplying or retailing more than 80% of total volumes. Over time, the company has reduced its exposure to the more capital-intensive refining segment, focusing on its marketing division, with an integrated cash return on invested capital above 10%.

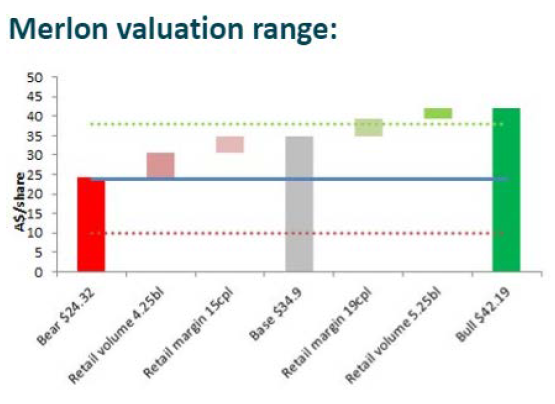

Valuation & market reasoning: We value Ampol at between $25 and $42 per share ($35 central case), with the stock currently trading towards the bottom of this range as the market is concerned about the impact of COVID on retail volumes, longer term declining fuel volumes (including the effect of electric vehicles), the sustainability of premium fuel margins, the ability to extract value from convenience sites, and weak refining margins.

Merlon view: ALD is trading at nearly 50% below our central case. We believe historically cyclical refining margins, currently 40% below mid-cycle, will revert to normal levels. More importantly, the industry structure has enabled retail fuel margins more than offset COVID driven volume declines (1H20 retail earnings before interest and tax was higher than pre-COVID levels). Further, we believe the market is not factoring in the growth in premium fuels consumption, the recently announced Woolworth’s Metro-branded and supplied convenience strategy, or the company’s superior infrastructure position and regional sourcing scale.

OSH