An interesting article posted on Seeking Alpha on Galaxy by new kid on the block Anton Tyumin.

Goes into a fair amount of detail. Recommend having a read.

Very conservative in terms of some assumptions - at least he admits it - but a thorough and interesting analysis report, if not terribly helpful in terms of wide range of price targets etc.

---------------------------------------- http://seekingalpha.com/article/403...ne-galaxys-correction-will-buying-opportunity

SUMMARY

After facing the standard early-stage lithium producer difficulties, Galaxy Resources emerges as a future growth play.

As the company’s growth prospects did not remain unnoticed, the stock has just demonstrated a sharp-paced rally towards new all-time highs.

However, despite trading near an all-time high, the stock remains reasonably valued and might be viewed as a compelling buy-on-weakness pick throughout 2017.

This is the third article in my lithium series. Among the stocks discussed in previous articles, Galaxy continues to maintain the title of a top performer.

Introduction

As it has already been approximately 400 days since the publication of the famous "What if I Told You" research note by Goldman Sachs which touted the industrial metal as "the new gasoline", we are already witnessing skeptical media headlines highlighting the speculative investor activity that takes place in the lithium sector.

It is true that it has been a fascinating year for the majority of top-grade lithium companies. The table below summarizes the performance of the lithium's Big 3 - the largest U.S.-traded producers worldwide - and that of Galaxy Resources (OTCPK:GALXF) and Orocobre (OTCPK:OROCF), which are oftentimes viewed as the 2 leading players in the emerging producer niche. All of the companies have been demonstrating strong performance lately, raising concerns of a speculative bubble emerging in the sector. Source: made by the author using the data from Google Finance.

As the table above greatly summarizes, newcomers' stocks are prone to higher volatility due to:

Higher exposure to lithium revenues in comparison with the Big 3.

Nonetheless, the risks of investing in early-stage natural resource companies are well-known as investors are no strangers to leverage and liquidity issues, shareholder dilution and make-or-break pre-feasibility study results industry's newcomers are so famous for. Although risk aversion might vary considerably among different investor groups, it is true that it made less sense to consider such players as Galaxy or Orocobre before the companies' progress was evident. However, as the companies mature and early-stage difficulties diminish, high reward is met with falling risks. In the meantime, market's judgment (as well as investor sentiment and analyst coverage) is likely to improve and result in gradual institutional holding accumulation once the stocks' trading liquidity allows for that. Source: HotCopper forums. Overview

According to the December 2016 Cannacord Genuity report on the current state of the lithium market, robust industrial demand continues to outpace the suppliers' efforts. Despite the notable progress, the sector is estimated to have an 8% supply deficit in 2016, mainly as a result of slower-than-expected production dynamics at Mt Cattlin (Australia), Salar de Olaroz (Argentina) and Mt Marion (Australia).

Even though the agency now forecasts the deficit to run up until the end of 2018, I would be less optimistic on that estimate due to a 12% average demand growth forecast for 2017-2025. For as long as cash continues to be mercilessly burnt throughout the emerging producer sector, elevated lithium demand growth is likely to drive the lithium spot rates high enough to force the emerging players hurry up before investor capital flees to producers who are the closest to achieving positive cash flow dynamics.

One of the good things associated with rising investor interest in lithium comes from improved analyst coverage and data availability. The figure below charts the agency's supply forecast. Source: Cannacord Genuityreport(December 2016).

The firm seems to be rather conservative on its pricing forecast. Lithium carbonate:

$12,000/t (+60%) in 2017;

$9,243/t (+32%) in 2018;

$10,300/t (long-term).

Lithium spodumene:

$904/t (+67%) in 2017;

$745/t (+55%) in 2018;

$727/t (long-term).

In the meantime, the latest Chinese pricing data demonstrates certain spot price stabilization that is accompanied by a gradual convergence between the spot and producer contract agreement prices. Source: Cannacord Genuityreport(December 2016). Medium-term prospects

It is not a secret that lithium production is not going to be exceptionally profitable for long. Most importantly, one should also acknowledge the fact that a large portion of emerging producers is likely to be late to the party, starting production after the lithium supply/demand balance gets gradually fixed. Finally, one cannot be entirely sure that the widely-used lithium-ion battery is not going to meet any direct substitutes. Although the technology is likely to maintain its leadership in the portable battery niche due to lithium being the most optional battery component from the weight standpoint, energy storage business doesn't care that much about weight. There will be alternatives (Bill Gates, Total and Shell are already backing this one). As a side note, interested readers might also want to read about the lithium-ion battery cost components on Qnovo.

Growing contrast as a potential contributor to the stock's performance?

As I've been arguing above, the rising cash flow dynamics differences between the lithium developers and producers are likely to result in some of the investor capital fleeing to producers who are the closest to achieving positive free cash flow.

Although a potentially faulty assumption, the prospects of continued share and debt issuance coming to an end might make investors reconsider their riskier lithium holdings. At a later point, the emerging lithium producer market will most probably face a certain contrast effect, resulting from a growing (short-term) difference in producing and non-producing companies' financials. Benefiting from increased investor confidence and analyst coverage, producers demonstrating higher financial strength are likely to experience improved institutional ownership dynamics. Although the players with the most speculative risk/reward combinations will be subject to enormous volatility and some of them might demonstrate an even stronger short-term performance, it still makes sense to remain overweight the top-tier players for as long as leading positions have their own perks. Stated differently, there is little need to search for additional risk while the leading emerging players remain small enough to outperform. Now, let's concentrate on Galaxy and its lithium concentrate. Galaxy: breaking down the risks

Despite the fact that investor sentiment has been predominantly positive for Galaxy's stock of late, multiple risks continue to prevail. It is true that multiple factors have considerably improved since the publication of my introductory article on emerging producers when the majority of investors (including yours truly) would have considered Galaxy's stock to be too risky.

As time was passing by, the changes in risk that have materialized throughout the period could best be described as follows:

Changes in risk:"Even though the risk of severe liquidity issues and/or production failure has decreased dramatically..."

Summarizing current risks:"…Current risks continue to signal a large probability of a near-term correction as the company has to issue additional equity and/or debt in order to fund its near-term liquidity and production requirements."

Liquidity and financial health

A key concern and a crucial factor for the stock's medium-term performance, liquidity risk is expected to be significantly reduced throughout 2017. Supportive of this statement is the expected revenue from Galaxy's first Mt Cattlin spodumene concentrate shipment totaling 6 million AUD.

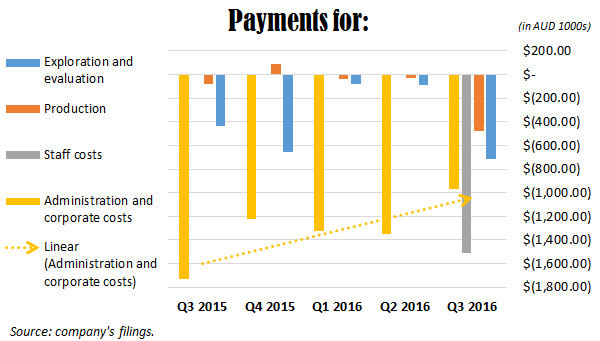

Since the cash burn rate remains a significant issue, let's have a more detailed analysis of the cash flows. The sudden spike in staff costs was related to the hiring of the first staff for the new office in Catamarca, Argentina, which represents one of the commitments the company agreed upon with Catamarca Mining Secretary in 2016. In its most recent Q3 2016 cash flow report, Galaxy estimated its Q4 2016 staff costs at a cash outflow of 0.5 million AUD.

The Q3 2016 decrease in administration/corporate costs seems to have something to do with the one-time increase in staff costs. Even though the Q4 estimate of an outflow of 1.5 million AUD would represent a quarterly increase of 54.8%, the total of staff, administration and corporate costs is estimated to fall by 19.42% in Q4 2016 - a positive development.

Another significant cash burden - exploration and evaluation costs - are expected to rise 5.2% in Q4 2016.

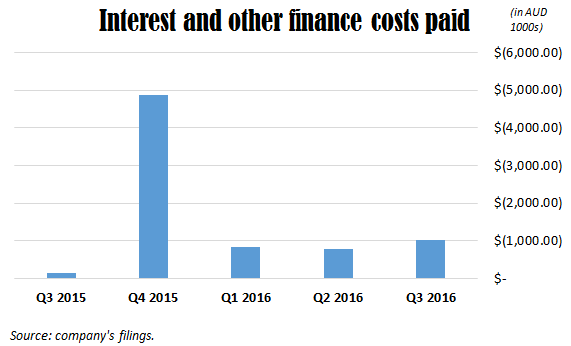

Interest payments have been on the rise lately, with a large probability of this trend continuing as the company continues to assume new debt.

The company is expected to demonstrate increased cash outflows in Q4 2016. In the quarterly cash flow review for Q3 2016, the company emphasized the 80% state of completion of Mt Cattlin construction works: "Galaxy reported that the refurbishment and upgrade of Mt Cattlin had passed 80% completion. Primero mobilised their team to site in late August to finalise the construction and completions packages and to begin implementing their planned commissioning and start-up program […] Galaxy and Primero undertook a detailed assessment of the capital costs expended to date and forecast to complete the construction and commissioning of Mt Cattlin until first revenue is received from Mitsubishi, now scheduled for December 2016. The total capital cost is now forecast to be A$22.4 million compared to the A$15million previously announced by General Mining, resulting from the throughput capacity upgrades together with the other plant modifications as outlined."

Source: company's filings.

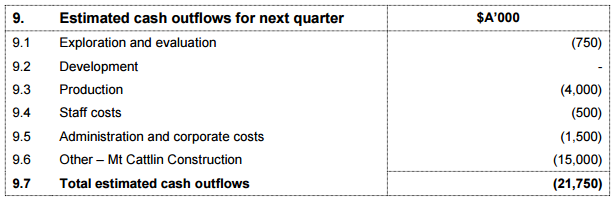

As expected, the revenue from Mitsubishi - estimated at 6 million AUD - would not cover the company's projected cash outflows with its total cash position accounting for just 9.3 million AUD as of the end of Q3 2016. Consequently, the company had to incur additional debt and issue more shares.

On October 31, 2016, the company announced the additional 16 million AUD facility from OCP, company's existing lender. Since the main purpose of the facility was to keep the company's liquidity afloat until it executes the first Mt Cattling spodumene shipment, the maturity date has been sent for March 31, 2017. With an annual coupon of 8%, the facility is secured against the company's assets and undertakings. Other terms included the 1-time facility fee (2%) and an establishment fee that led to an issuance of 40 million warrants with an exercise price of 0.3436 AUD.

On November 14, 2016, Galaxy announced the issuance of 25 million additional ordinary shares, increasing the total of fully paid ordinary shares to 1,832,545,826 (+1.38%). Additionally, a total of 0.5 million unlisted options (0.40 AUD strike price) and 1 million share appreciation rights (base price of 0.324 AUD) was issued.

On January 19, 2017, the company announced the $40 million secured debt facility with BNP Paribas (OTCQX:BNPQF).

Source: company's filings.

A total of 25 million ordinary shares was issued on January 20, 2017.

Breaking down the risks: discussion

No matter how you put it, it is clear that the most crucial risks associated with Galaxy's stock are gradually diminishing. Let's have a brief summary to look at the bigger picture. I will sort the bullet points based on relevance.

The company's short-term liquidity requirements are covered by the recently-issued debt. Since the construction works at Mt Cattlin should have already been finished, the capital expenditures related to Sal de Vida operations are going to be partially offset with positive cash flows. Having secured financing from BNP Paribas, company's management has just demonstrated increased confidence in the company's operations and financial health, which implies easier financing in the future.

Having just sent the first spodumene shipment and secured a contract agreement for 2017, the company continues to build its reputation as a reliable producer in the eyes of lithium buyers and investors (I am referring to the contrast point mentioned above). From now on, Galaxy's stock provides a certain margin of safety over the smaller lithium companies which, due to lack of production, can only be considered as asset plays at this point.

Truth be told, despite having just recently passed investor confidence test, Galaxy's stock continues to face the common risks associated with small cap investing. The stock is (1) strongly illiquid and (2) continues to face severe dilution, which consequently leads to (3) low shareholder control and (4) weak institutional interest.

Breaking down the potential reward

There is always another perspective. Some of the factors discussed in this section might present a different view on the risks presented above.

There are two crucial facts that have to be outlined in this section. After finishing the Mt Cattlin plant improvement works and executing the first spodumene shipment, Galaxy announced the terms for the 2017 contract agreement.

Firstly, the updated terms represented a significant pricing increase, upping the price from $600/t for a 5.5% lithium concentrate (Li2O) to $905 for 6% lithium concentrate (or $830/t for a 5.5% concentrate), effectively demonstrating a 38.3% price increase in 5.5% concentrate terms.

Secondly, a wise question to ask would be whether Galaxy is capable of producing higher-grade as efficiently as it's been operating with the 5.5% grade. As the company should have already finished all construction works at Mt Cattlin (construction and recommissioning were forecast to be complete before the first spodumene shipment), it now targets a 70% recovery rate, up from 50% before the optimization. Combating high mica content, Galaxy has upgraded its mica removal circuit, which had an adverse impact on operating performance due to higher transportation costs.

Relative valuation

I present my back-of-the-envelope assumptions below. I mainly rely on company's own estimates (converted into AUD) and Cannacord's long-term lithium price forecasts. Since the company described Mt Cattlin as a "high margin operation with current operating costs," I assume that Mt Cattlin operating margins will be between 20 and 40 percent for base and optimistic scenarios, respectively (approximately 0.33-0.66% of SDV margins). My optimistic case scenarios - which many might still find rather conservative - predominantly increase the base case estimates by 10 percent.

After having estimated TTM EBIT for Q2 2020 (which is expected to include 1 full year of SDV production) between 225.12 and 336.83 million AUD, I estimate the amount of cash the company would lack to start-up its Sal de Vida operations. It is important to mention that my calculations involve a crucial assumption that the company is only going to fund these expenditures with new debt and cash from operations as this would be the worst scenario from the shareholders' perspective (unless the share price tanks and the company continues to dilute its shareholders at significantly lower prices, which seems highly improbable to me). On a later stage, I estimate the amount of potential debt reduction after SDV production begins. Source: made by the author using the data from company's filings and Cannacord Genuity research reports.

In a combination with assumed liquidity positions of 10-15 million AUD, these debt estimates are used to calculate the market value of equity for different EV/EBIT values. Using the 10-quarter values of EV/EBIT valuation for the shares of Albemarle (NYSE:ALB), FMC (NYSE:FMC) and SQM (NYSE:SQM) and applying a large discount to Galaxy peers' valuation, I estimate the potential upside to Galaxy's current market capitalization at approximately 11-108%. It is important to note that my assumptions did not lead to any upside in base and medium case scenarios, which I view as a possible result of excess skepticism.

Source: made by the author using the data from company's filings and Cannacord Genuity research reports.

Nonetheless, assuming annual stock dilution rate of 5-10% (there was an 8.95% dilution in 2014-2015) and high valuation potential, I arrive at a June 30, 2020 price target of AUD 0.85-1.03 or $0.64-0.78. Even though one can easily come up with arguments supporting higher lithium pricing forecasts and lower EV/EBIT discount to Galaxy's peers with lower growth potential, I maintain the view that my assumptions reflect a balanced opinion and account for the potential of unexpected risks and headwinds.

In the meantime, here are some of the relevant developments this analysis does not take into account:

James Bay DFS recommencement is planned for Q1 2017.

The ongoing industry consolidation and Albemarle's optimistic goals for capturing 50% of the industry's growth might be of paramount importance in the medium-term. Even though I would highly encourage the readers to read the recent ALB posts by Joe Lowry ( link 1, link 2), a research note by David Wang at Morningstar greatly summarizes the current situation Albemarle's management has gotten itself into: "Without acquisitions, we think it will be difficult for Albemarle to capture half of incremental lithium demand, as management hopes."

Sentiment analysis

Now, let's study the recent history of Galaxy's main developments and the consequent share price trends. Material events - which are mostly taken from the company's press release titles - are divided into 10-day periods and plotted on the chart. Note: "new share issue" might also include unlisted options, warrants and rights issues.

It is not a secret that the stock remains highly volatile.

All data in AUD. Source: made by the author using the data from the company's filings and Investing.com

Even though the share price was in an uptrend prior to the General Mining acquisition, bidders statement seems to have diminished investors' optimism for quite some time.

All data in AUD. Source: made by the author using the data from the company's filings and Investing.com

There were multiple buying opportunities as investors have been largely ignoring the positive developments at Mt Cattlin, preferring to concentrate on the company's ongoing acquisition throughout the whole summer and the first half of autumn.

All data in AUD. Source: made by the author using the data from the company's filings and Investing.com

However, once the acquisition was complete, the stock experienced a strong trend reversal, accompanied by increased newsflow on Mt Cattlin. As we are currently approaching the quarterly and annual earnings results, a cyclical correction began to take place in mid-January. I conclude that the current price trend is likely to reverse significantly by the end of March, presenting a buying opportunity as investors await the annual financial and annual report, currently scheduled for March 31 and April 30, 2017, respectively.

All data in AUD. Source: made by the author using the data from the company's filings and Investing.com Conclusion

My relative valuation analysis implies a potential upside of 37-66 percent. I predominantly rely on lower lithium pricing estimates and maintain a skeptical view in order to adjust for potential risks and headwinds. Even though the calculations will have a large margin of error due to overly simplistic assumptions and multiple moving parts, stretched peer valuation demonstrates investor confidence and will have a positive impact on Galaxy's stock over the medium-term.

Updates on James Bay progress and Mt Cattlin margins are likely to have a significant influence on the share price once they are published. In the meantime, decreased newsflow will most probably have a negative effect on the short-term stock price dynamics.

The company's near-term liquidity requirements have already been met. Involvement of a large international bank demonstrates rising investor confidence and institutional interest.

As the industry continues to consolidate, Galaxy and/or its assets in Argentina and Canada might be viewed as an attractive acquisition target for the larger players.

Even though the stock might continue following the downtrend in the coming weeks, the correction represents a buying opportunity for investors focusing on an investment horizon of at least 6-12 months. While the new all-time highs are likely to follow later this year, the U.S.-listed stock is currently 8.65 percent below the record level. Although the technicals are mixed, additional downside and break below the SMA20 is more than possible.

I assign a "Buy" rating to GALXF.

Source: BarCharts Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in GALXF over the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. Additional disclosure: This is not an investment advice. I am not an investment advisor. Please be aware of the fact that small cap investing involves additional risks and consider the ASX listing for higher liquidity.

Editor's Note: This article covers one or more stocks trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks.

GXY Price at posting:

63.5¢ Sentiment: Buy Disclosure: Held