Summary

Perseus Mining had an exceptionally strong quarter on the back of a good production result and selling gold at a 10% premium.

This allowed the company to generate a positive free cash flow and add cash to the balance sheet, despite spending money at Sissingué.

The performance will weaken though, as the average hedge price of the gold is roughly 5% lower.

The company remains in an enviable position as its working capital is now approximately equal to its market capitalization.

Introduction

Seeking Alpha readers who have been following me and my articles for quite a while will undoubtedly know I have become

cautiously optimistic about Perseus Mining (

OTCPK MNXF

MNXF) which is operating the Edikan gold mine in Ghana. The company has turned a corner and after several years of overpromising and underdelivering, the times have changed and the mine is now free cash flow positive. For now.

PRU data by YCharts

Perseus Mining has more liquid listings on both the

Toronto Stock Exchange and the

Australian Stock Exchange where the company is listed with PRU as its ticker symbol. The combined average daily volume on both exchanges is approximately 3.3M shares, so I would suggest you to use one of both platforms to execute your trades in Perseus Mining.

Perseus Mining seems to be cashing up

Perseus Mining described its first quarter of the financial year 2016 (which ends in June next year) as '

sound', and not only do I tend to agree with this statement, I also think it's an understatement. The quarterly production was almost 45,000 ounces which effectively means the company is on track to meet the production guidance for the first half of this financial year. Not only will the production guidance be met, the cost guidance might actually be proven to have been quite conservative. The all-in site costs in Q1 FY 2016 were $1060/oz and that's lower than the $1100 the company had been guiding for.

There was an additional positive surprise as the entire quarterly production had been hedged at $1291/oz, resulting in a much higher operating margin than what Perseus would have achieved without hedges. This also confirms my thesis that hedges aren't per definition 'bad' (which is the general point of view of the markets these days). It could be worthwhile to hedge a part of the intended output at a decent price which is what Perseus effectively has done.

(click to enlarge)

Source: financial statements

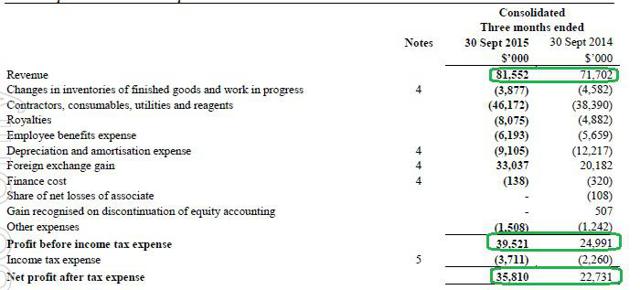

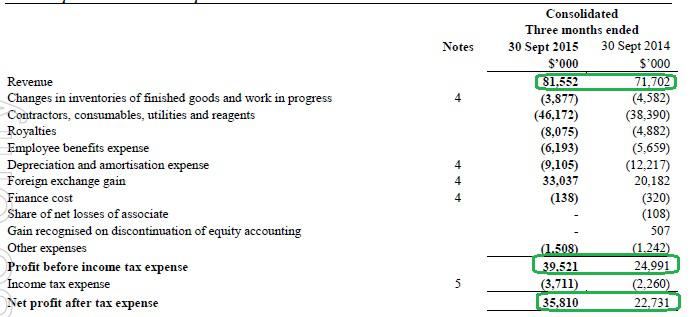

The company's

total revenue was A$81.6M ($58M), resulting in a pre-tax income of A$39.5M ($28M) and a net income of A$35.8M ($25.5M) in the first quarter and not only is this 'pretty good', it's also better than last year on the back of a decent production performance and a weaker Australian Dollar (Perseus is selling its gold in USD but reporting its financial statements in the weaker Australian Dollar).

(click to enlarge)

Source: financial statements

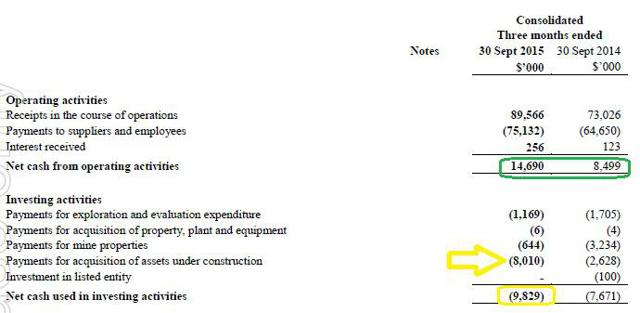

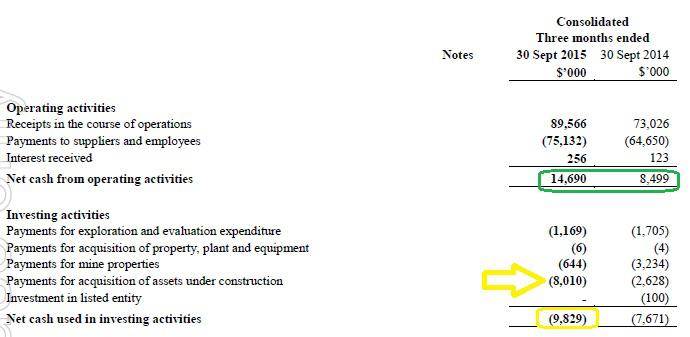

The cash flows were also very strong with an operating cash flow of A$14.7M ($10.5M) of which A$9.8M ($7M) was spent on exploration, equipment and 'acquisition of assets under construction'. As the latter is much higher than in the corresponding period of the previous financial year, I'd hope this also already includes some expenses made for the new Sissingué gold mine in Ivory Coast. No official breakdown has been given, but as the sustaining capex per produced ounce of gold in Ghana was $83, it looks like the sustaining capex was less than half of the total amount the company has spent on capital expenditures.

(click to enlarge)

Source: press release

Additionally, it looks like Perseus Mining has been able to push forward with some additional cost savings, and the mining and processing/maintenance expenses fell by respectively 50% and 23%, boosting the financial performance.

The strong balance sheet will be needed to fund the construction of its newest mine

The strong free cash flow in the first quarter resulted in a very welcome boost of the company's working capital position. Not only did the working capital increase to A$191M ($137M), the cash position also jumped by 20% to A$123.4M ($88M) as of at the end of September.

That's great and not only does this mean Perseus Mining's market capitalization is now approximately the same as its working capital position, the increased cash component of the working capital will be very helpful to contribute to the funding mix to finance the new Sissingué mine in Ivory Coast.

Keep in mind Perseus' financial results will be weaker in the next few quarters (and years) as the current spot price of gold is lower, whilst the impact from the positive excellent hedging strategy will be lower (the

remaining hedge book consists of hedges at $1240/oz, approximately 5% lower than the hedged price in Q1 FY 2016). This could be compensated for by an expected production increase and production cost decrease, in line with the official guidance.

(click to enlarge)

Source: company presentation

Investment thesis

Even after what's supposed to have been a 'difficult' start of the financial year 2016, I remain positive about Perseus Mining as the company generated a substantial amount of sustaining free cash flow (in excess of US$7.5M, after deducting the growth capex at the Sissingué mine). The company isn't doing anything stupid with this cash and just keeps it in the bank account as it knows it will be useful to fund the development of the Sissingué project.

I'm starting to consider Perseus Mining as an interesting potential buyout target for any producer trying to get exposure to Africa. The Edikan Mine should really see a performance boost from 2018+ on whilst the Sissingué mine in Ivory Coast is supposed to have a low production cost. Perseus Mining remains relatively high on my 'tax loss selling season' priority list.

(20min delay)

(20min delay)