The retreat of globalisation, the trade war between the US and China, as well as China's own economic problems are leading Australia into a trap, from which the only escape is higher household disposable income to lift domestic demand and an increase in productivity.

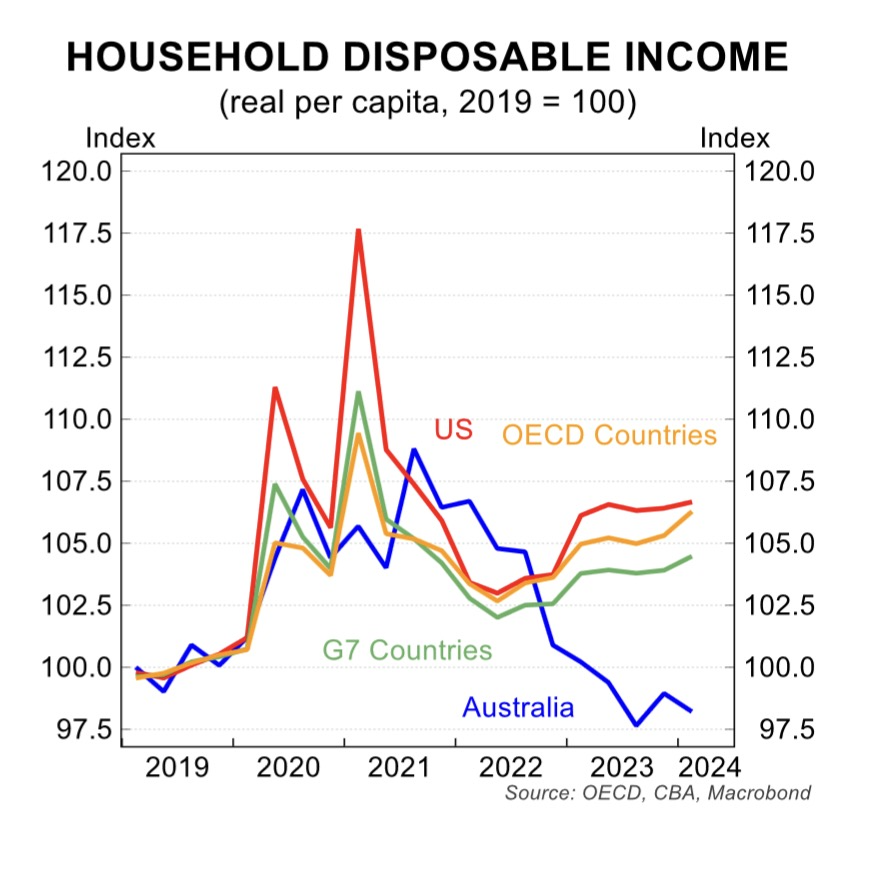

The first of those is dismal because of the large amount of household and mortgage repayments. We're starting a long way behind:

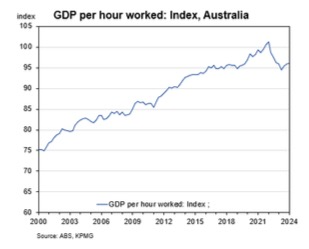

As for productivity, it collapsed during the pandemic and hasn't yet recovered:

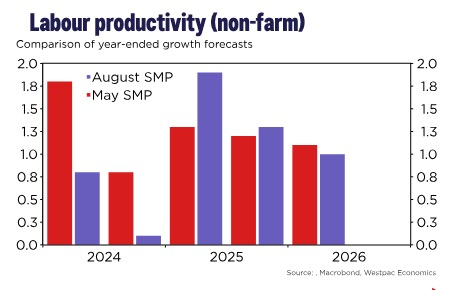

... and the Reserve Bank, at least, is quite pessimistic about the prospects of getting it back to the 1.5-2% growth. This chart shows the RBA's forecasts of productivity from the last two Statements on Monetary Policy:

Where is Australia's future growth going to come from, if not from rising terms of trade and productivity? Nowhere that I can see.