Lately, oil markets have been finely balanced. Both the bulls and bears can make a compelling argument for their respective cases. Russia has vowed not to flood the oil markets while the compliance rates remain high. Inventories have fallen. Prices touched post 2014 highs at $71 a barrel (Brent) and $65 a barrel (WTI). Bears peddle the clichéd, yet not at all insignificant, story of U.S. Shale.

The IEA in its recent report said that U.S. oil production could reach 11 mbpd this year. Rigs are being added across the country, taking the total number of oil rigs to its highest level since April 2015. Much of the current situation is thanks to the Vienna deal that saved oil prices after they tanked below $26.

One might ask what will become of the markets after the deal expires. In other words, how long can the OPEC-NOPEC producers continue to cap output? With a rising U.S. production and the possibility that one day, and that day might come very soon, the oil producers will open their taps anew. On top of that, the lack of any drastic upbeat demand figures makes a bearish case for oil more than possible.

Credit can be given to the technological improvements and resilience of shale producersthat kept pumping oil even when prices were low. But the Vienna accord, spearheaded and held together by Saudi Arabia and Russia, still managed to raise oil prices. Both OPEC and Russia have their interests in maintaining a healthy oil price. For every one dollar oil prices fall, Russia loses $2 billion in revenue. OPEC’s leader, Saudi Arabia, needs higher oil prices to ensure the successful IPO of Aramco. For these reasons, the deal was extended last year until the end of 2018. There are chances it might be extended further, but how much?

One can make an educated guess that the current production cuts can certainly hold until Aramco’s IPO, which is a huge bet on the country’s future. Once the IPO is done, we might expect weakness in the Saudi resolve to continue the deal. Russian executives are also losing confidence.

Last year in November, many energy industry executives expressed their concernregarding rising U.S. shale production. It remains to be seen for how long they can allow others to free ride on their efforts. The IEA reported that the U.S. will be a net exporter of oil and gas by 2022. Revising its estimates, it said that U.S. production will touch 11 mbpd this year (earlier estimates suggested this wouldn’t happen until 2019).

The members meet in June for a review meeting. Inventory levels are still above the five-year moving average, showing that they have work to do, but some members may be tempted for an early exit.

Dr. Mamdouh Salameh, International Oil economist and World Bank Consultant on oil & energy, is positive about oil prices. He says “Oil market fundamentals are positive enough to sustain an oil price ranging from $70-$75 in 2018. By this I mean that the global economy is projected to grow by 3.9 percent in 2018 and 2019 compared with 3.5 percent in 2017 according to the IMF. The global demand for oil is projected to add 1.7-2.0 million barrels a day (mbd) this year over 2017.”

Dr. Salameh was very upbeat when discussing the strength of the commitment between Russia and Saudi Arabia, saying that “OPEC and Russia have suffered a great ordeal with the steep decline of oil prices since 2014. That is why they never want to suffer that experience again.”

To rely on a single deal that limits production from certain members is not a good idea. Not to mention the fact that the production cuts continue to face challenges in the shape of rising U.S. production offsetting the effects. There is only one way to get out of this vicious circle of supply and price: Demand.

The IMF says that the world economy will witness growth this year. Eurozone economy is also picking up. Demand is also expected from India and China. Electrification of transport and policy changes supporting climate change are other factors to consider. The transportation sector is a major consumer of oil. China, with the biggest car fleet in the world, plans to ban conventional cars by 2022. France, India and other countries are following.

The recent talks about forming an OPEC Super group, a marriage between OPEC and Russia, has uplifted the sentiments again. However, it remains to be seen whether Russia will go along with this plan. Even if it does, the fact remains that such deals cannot be a permanent solution for stabilizing oil markets.

The threat from the U.S. is real and production cuts are not a long term solution to stabilize oil markets.

Oil prices have increased, but this is just the beginning.

U.S. oil production is expected to drive the global oil supply this year.

Where is the rig count surge that bears expected?

Investment Thesis

Oil prices have increased substantially in the last six months, but this is just the beginning. After a seasonal swoon in the winter, I expect oil prices to continue upward in 2Q18 into the summer driving season. Recent Performance

Brent crude oil prices have fluctuated in recent weeks following a substantial rise in the second half of last year:

$65 Was Not Enough To Boost Supply

Despite substantially higher oil prices in recent months, the global oil supply has remained below global oil demand, causing a strong imbalance, which has led to continued inventory draws across the world. The International Energy Agency included the following paragraph in its latest Oil Market Report:

OECD commercial stocks fell in December by 55.6 mb, the steepest drop since February 2011, to reach 2 851 mb. Stocks drew by 154 mb (420 kb/d) during 2017 and ended the year 52 mb above the five-year average. In 4Q17, stocks fell sharply by 1.3 mb/d across the OECD.

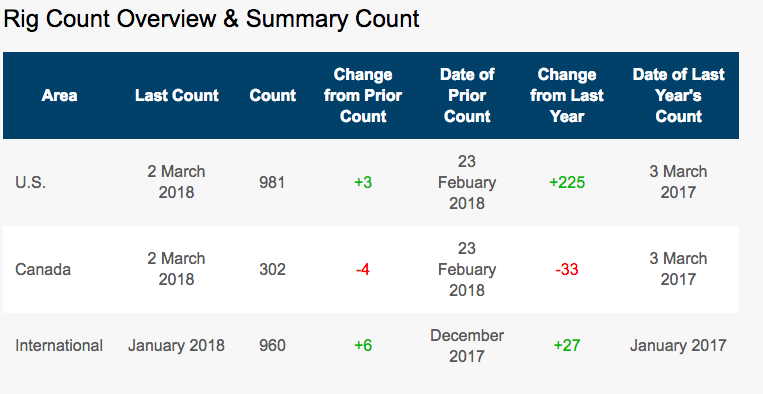

Global oil inventories have declined at a fast pace, dragging prices higher, but the global oil production still has not reacted. Today, we received yet another indication of near future constraints in global oil supply:

The above table from Baker Hughes shows that, although the U.S. rig count had surged from the year-ago period, which has led to rising U.S. oil production in 4Q17, the rig count has recently been muted. This trend is also confirmed by the DI Drilling Index, which has been flat throughout the last several weeks:

---------------

More troubles for Chinese oil firm as Nigerian govt moves to retrieve $3 billion

The Nigerian government has commenced legal proceedings against the Chinese-owned oil firm, Addax Petroleum Development Nigeria Ltd, over the company’s alleged under-remittance of $3 billion in taxes and royalties.

Court documents seen by PREMIUM TIMES show that the funds, according to the government, are outstanding claims against the troubled company under the Petroleum Profit Tax Act and Petroleum (Drilling and Production) Amendment Regulation 2003 over Oil Mining Leases (OMLs) 123, 124, 126, and 137.

Joined as respondents in the suit are Addax Petroleum Development Nigeria Ltd, Addax Petroleum Exploration Nigeria Ltd, the Nigerian National Petroleum Corporation (NNPC), the Ministry of Petroleum Resources/Department of Petroleum Resources, and the National Petroleum Investment & Management Services (NAPIMS).

According to the government, the $3 billion unremitted funds came as a result of the oil multinational’s alleged illegal and irregular reliance on Side Letters dated November 21, 2001; December 20, 2001; and August 24, 2004 which were “never gazetted.”

The government’s move to recover the funds from Addax Petroleum came three months after a PREMIUM TIMES report on how the Chinese firm allegedly paid millions of dollars in bribes to Nigerian officials to secure juicy contracts in the oil industry.

‘HALT ADDAX’S OIL ALLOCATIONS’

In its suit before a federal court in Lagos, the Nigerian government is seeking a court order directing the NNPC, Ministry of Petroleum/DPR, and NAPIMS from further allocation of crude oil explored from OMLs 123, 124, 126, and 137 to Addax Petroleum pending when the company furnishes the court verifiable Bank Guarantee from Nigerian banks to cover the monetary claims of the plaintiff.

Other prayers sought by the Nigerian government include an order restraining the NNPC, petroleum ministry, and NAPIMS from dealing with Addax Petroleum as wells as stopping them from transferring or assigning their interest in the OMLs to another person. Also, an order compelling the Nigerian agencies to file an affidavit of fact detailing the company’s assets, properties, and funds.

The government is further seeking a declaration that the side letters of 2001 and 2004 were never gazetted and, as a result, cannot substitute the subsisting fiscal regime covering the tax and royalty obligations of Addax Petroleum with regards to OMLs 123, 124, 126, and 137.

Another declaration being sought is for the company to remit $3 billion ($3,093,996,505), being the outstanding sum underpaid in tax and royalty obligations, to Nigeria’s treasury.

On Friday, Mojisola Olatoregun, the judge, granted an order for the government’s lawyers to serve court papers to the NNPC, the third respondent in the suit, whose office is situated in Abuja, outside the court’s jurisdiction.

The judge adjourned further proceedings in the suit till May.

CONTROVERSIAL SIDE LETTERS

In 1998, Addax Petroleum, now a subsidiary of China’s Sinopec Group, one of the world’s largest oil and gas producers, entered into a Production Sharing Contract (PSC) with the NNPC (as concessionaire) in respect of OPL 98/118 and OPL 90/225.

Four years later, the company discovered oil in commercial quantities and the OPLs were converted into Oil Mining Leases (OMLs) 123/124 and 126/137.

The PSC entered by the two parties required Addax Petroleum to pay royalties on any oil produced from the relevant oil blocks at the rate of 20 per cent as stipulated by law. It also provided that the Petroleum Profit Tax Act (PPTA) applicable to the contract areas shall be 65.75 per cent for the first five years, starting from the first day of the month of the first sale of the oil, and 85 per cent thereafter.

But, according to the Statement of Claim filed by D.A Awosika & Partners, the lawyers prosecuting the case on behalf of the Nigerian government, Addax Petroleum fraudulently obtained a Side Letter in 2001 and 2004 which were “never gazetted” and which they used in calculating their taxes and royalties.

The calculations in the side letters fixed the PPT payable by the company at 60 per cent and, rather than the 20 per cent flat rate of royalty, provided for a graduated rate depending on the volume of oil produced from the oil blocks.

The side letters were signed by Funsho Kupolokun, then Special Assistant on Petroleum and Energy to President Olusegun Obasanjo (in 2001) and Olabode Agusto, then Director General/Special Adviser on Budget to the President (in 2004).

“Several objections and protests were raised by FIRS (Federal Inland Revenue Service), NNPC, and DPR to the reliance on these side letters by the Defendants to bypass, supplant, and subvert the process,” the government’s lawyers stated in their claim.

“In 2003, in order to give effect to the graduated royalty regime stated in the side letters, the Minister of Petroleum Resources (Mr. Obasanjo) issued the Petroleum (Drilling and Production) Amendment Regulations which provided for graduated royalty rates for onshore and shallow offshore PSC which did not account for royalty by tranches.

“The Petroleum (Drilling and Production) Amendment Regulations 2003 when made was given retroactive effect from the first day of January 2000, which was the same date of commencement of the graduated royalty rates contained in the side letters.”

Several meetings between Nigerian government officials – represented by the FIRS, DPR, and NNPC – and representatives of Addax Petroleum to reassess and resolve the latter’s “colossal underpayment” to the government between 2007 and 2012 yielded no results.

In one of the meetings, PREMIUM TIMES learnt, it was discovered that the company’s application of the graduated royalty rates as provided for in the Petroleum (Drilling and Production) Amendment Regulations 2003 as contained in the side letters was erroneous.

Rather than relying on the applicable royalty rates in calculating their daily production volume, Addax Petroleum allegedly developed a practice of slicing their volume rate of royalty to different tranches of production thereby significantly reducing their royalty obligations.

Government calculations of under-remittance showed that the company withheld $1.3 billion in royalties and $1.7 billion in PPT.

But Addax Petroleum maintained its right to the use of the side letters for computing the taxes on its operations and dragged the government over accusations of a breach of their 1998 PSC on the oil blocks.

In suit FHC/ABJ/CS/1099/2014 filed before Ibrahim Auta, a judge, the company sought a judicial approval towards their continued use of the side letters to compute its financial obligations to the Nigerian government.

However, on May 26, 2015, three days before the administration of the then president, Goodluck Jonathan, handed over to his successor, Muhammadu Buhari; the government negotiated a controversial out of court settlement with Addax Petroleum, agreeing to pay the company $3.4 billion (about N1 trillion).

Court papers filed by the Nigerian government’s lawyers stated that Addax Petroleum “surreptitiously teamed up” with some officials of DPR, FIRS, and NNPC to execute certain terms of settlement which was eventually made the Consent Judgment of court notwithstanding the pendency of several applications yet to be heard by the same court.

“In executing the said terms of settlement, the authorities were not sought, no approval at Federal Executive Council level was given, the governing boards of the FIRS, NNPC and DPR did not authorise those officers that executed the bogus terms of settlement to so act,” the lawyers argued.

The lawyers now seek a court declaration to nullify the consent judgment and to set it aside.

FAR Price at posting:

7.9¢ Sentiment: Buy Disclosure: Held

(20min delay)

(20min delay)