We felt it was time to provide an update on Paradigm Biopharmaceuticals Ltd (PAR.ASX), given how far the company has progressed since our last update. We believe Paradigm is shaping up to be the next major Australian biotech success story. With minimal risk of failure and huge revenue potential, Paradigm could propel to become one of the biggest Australian listed biopharmaceutical companies on the ASX. In our research below, we reference our previous research note, as we assume our readers have already read it. If not, you can access it HERE. INVESTMENT HIGHLIGHTS

We see a less than 1% risk of failure for the upcoming Osteoarthritis Phase 2b clinical trial - based on the Special Access Scheme (SAS) patient data compared against Placebo effect in similar trials.

Zilosul® (Paradigm’s drug) appears to be the best in class for treating OA and will become a blockbuster.

We estimate a big pharma will seek a licensing deal for Zilosul® above US$2 Billion [total deal size] in 2019.

Paradigm’s new licensing deal for MPS can be commercialised quickly for an orphan indication with revenue potential per year of over US$1 Billion.

Once commercialised, we estimate MPS could attract a US$1 Billion licensing deal.

Should Paradigm successfully sign licensing deals or commercialise all three indications (OA, MPS & Ross River) and accounting for an additional dilution of 15%, we believe Paradigm could trade over $30 per share or an estimated AUD$5 Billion Market Cap.

Future licences for other indications or success in Paradigm’s existing suite of patents could see additional upside in the share price.

TESTING THE THESIS

Debating companies is a great way to see where your thesis could be wrong. As money managers we think in terms of risk. Where are we wrong? What kills us on this investment?

We have not stopped asking these questions since we first found Paradigm (PAR.ASX). We feel that not many others have undertaken the same level of due diligence that we have done for Paradigm, and therefore, they do not understand what they own. As famous investor Peter Lynch once said, “Know what you own, and know why you own it”.

So, when we hear comments like “the risk is that they fail the clinical trial” we instantly recognise these investors probably haven’t adequately valued this business or weighted this risk with a probability. Not only is Paradigm likely to see success in their upcoming clinical trial for OA but given the safety and quality of the data being released - investors should ask themselves the question - what other indications that have inflammatory issues as a symptom could also be treated using iPPS?

Should Paradigm see success in their upcoming Phase 2b clinical trials (OA & Ross River) they could potentially develop a whole suite of drugs able to treat any disease with associated inflammation…of which there are many! Paradigm could quite easily become an Australian pharmaceutical success story with one drug reformulated to treat multiple blockbuster indications.

Hopefully our analytical research below goes some way to showing new and existing investors just how low the risk is, when considered next to the opportunity. We say this without reservation. This is the most extreme asymmetric risk/reward trade we’ve ever come across. “This is the most extreme asymmetric risk/reward trade we've ever come across”. OSTEOARTHRITIS (OA) PHASE 2B CLINICAL TRIAL

Estimated read out of results: 18th December 2018

Let’s start with the company’s leading indication – Osteoarthritis (OA) of which we think the below quote from Flavia Cicuttini, an arthritis expert from Monash University, summarises how big this could be. “It’s often said if you had to choose one disease, one drug, if you could find a drug to slow the progression of osteoarthritis you could be home and hosed for a decade”.

“At the moment osteoarthritis is the last frontier of big diseases with no treatment, if this drug (Zilosul® works, even if it just slows the progress, you don’t need to cure it, you could change the pattern of the disease”. – Flavia Cicuttini, Monash University

As we know OA is extremely common. There is currently no drug on the market that treats the cause of OA. People get addicted to opioids treating the chronic pain associated with this disease. Some patients have joint replacements which also have serious health ramifications. They can use corticosteroid products to treat the symptoms, but this is not a long-term solution and also has many negative side effects. There is platelet enrichment therapy, stemcell treatment, NSAID’s (non-steroidal anti-inflammatories) and interarticular injections to try and help treat the symptoms – none of which resolve the issue for a long period of time.

Paradigm’s Zilosul® however, not only treats the symptoms, but it acts on the cause of the symptoms. The bone marrow edema (BME) lesions (bruising) cause pain and inflammation, of which Zilosul® shows to effectively remove. Zilosul® also has a long lasting effect and no material side effects being reported. Paradigm’s Zilosul® treats the symptoms by acting on the CAUSE of the pain & inflammation.

Pre & post PPS treatment.

From the data that has been released to date, we’ve had discussions with doctors, key opinion leaders and those who have been treated with the drug. The consensus is that Zilosul® is likely the best, most effective drug for treatment of OA. Read that again: Paradigm’s Zilosul® is likely the most effective drug for treatment of OA.

To give this some perspective, imagine going back in time to 2006 and I tell you that this little Apple iPhone I’m holding is going to be the best phone on the market. In the future it will probably be the most popular smartphone in the developed world. Do you ignore it? Or do you confirm that the power of this smartphone technology is far superior to everything else on the market and buy Apple stock?

From what we have seen so far with Paradigm and Zilosul®, it feels a lot like we are holding an iPhone in 2006.

If you have the best product on the market, people will buy it. When it comes to our health, the demand is far higher than iPhones. Given how common OA is and the lack of solutions to fix the disease, the demand for Zilosul® is likely going to be extremely high. If both you and your friend have OA, and your friends’ OA improves after being treated with Zilosul® - are you going to try it, or remain in pain? Did you buy an iPhone or stick with the Blackberry/Nokia?

Investors can already see this demand from how quickly people are signing up to be treated under the Special Access Scheme (SAS) in Australia. The numbers have grown from nothing to over 500 people wanting to be treated at only a limited number of sites. We’ve heard stories of people travelling hours by train in order to get the treatment. Paradigm have done very limited marketing and it’s difficult to gain access - yet the numbers have grown exponentially from word of mouth and positive referrals.

Some of the most successful investing is done by just owning the companies that make the products people want. While this is very early stages, the feedback and signs we are seeing are evidence of what could become a multi-billion dollar per year drug. It’s not even commercialised, and people are desperately seeking treatment from just word of mouth. Just think, how many people do you know with OA or with pain in their joints, that could benefit from Zilosul®? How many people do you know with OA or joint pain, that could benefit from Zilosul®?

The incredible thing about Zilosul® is the length of time it lasts. While there is limited data on this, our estimates are that a treatment will typically last between 6 and 12 months (depending on the person).

As the positive impacts of taking Zilosul® wear off, the patient will seek follow up treatment to avoid the OA associated pain. Most patients feel the need for six monthly or annual treatments with Zilosul® to maintain their lifestyle activities (walking, jogging, exercising, travelling etc) which had been restricted prior to the accessibility of this treatment.

While Zilosul® will be in extremely high demand for all people suffering from OA, there is a huge recurring revenue potential for those patients who need repeat treatments to continue enjoying pain free lives. Once a patient uses Zilosul®, they will continue with treatments for as long as possible. RESULTS

The data released under Paradigm’s Special Access Scheme (SAS) has seen an average pain reduction of 51.2% in 145 patients (N=145). Investors must remember, the SAS is similar to the Phase 2b trial, but also very different. We believe that the results of the upcoming clinical trial will exceed those from the 145 patients treated under the SAS program. We believe the results of the upcoming clinical trial will exceed those of the 145 patients treated under the SAS program.

The clinical trial has very specific eligibility criteria- it requires a different dosage regime than those in the SAS program. Patients in the SAS program could have much more severe OA & receive a lower dosage (which means less responsive to treatment).

The below is an excerpt from the release on 15th August 2018 and details what we believe is a more likely outcome for the results in the upcoming Phase 2b clinical trial:

ASX release 15th August 2018 - PAR achieves 60% reduction in OA pain

The current Phase 2b clinical trial will only treat 55 patients with Zilosul®, with the remaining 55 patients receiving a placebo. In the SAS program, there are nearly 3 times the amount of people being treated than in the clinical trial, so Paradigm have already provided a taste of things to come through their regular reporting of the SAS results.

Number of patients being treated under the SAS program, compared with the Phase 2b clinical trial.

The data that Paradigm have obtained through the treatment of SAS patients has allowed them to “road-test” the Zilosul® treatment course concurrently with their Phase 2b OA clinical trial. Obtaining the SAS data is a unique approach that has allowed Paradigm to de-risk the clinical trial and incorporate predictability on the clinical trial outcome. CLINICAL TRIAL & PLACEBO

The biggest catalyst for any biotech stock is success/failure in a clinical trial. Below is our research to help investors understand just how low this placebo risk is when compared to the SAS results that have been released.

End Points: Paradigm’s OA trial needs to show a 15% reduction in pain as its primary end point. To be commercially significant this figure should exceed 30%. Paradigm are currently seeing on average a 51.2% reduction in pain from the SAS cases that have been reported.

Paradigm’s Phase 2b OA Clinical Trial end points

To further demonstrate our confidence in a successful result, a previous study done by Dr Peter Ghosh in 2005 to test if iPPS (the major ingredient within Zilosul® was effective in treating OA, showed a statistical significance and would have passed a clinical trial.

Not only was that trial significant, but the difference between the Ghosh trial and Paradigm’s trial (and SAS results) are that patients now receive double the dosage of iPPS. As you would expect, the results being released from Paradigm are significantly better than from the Ghosh study.

Put simply - on half the total dose used in a treatment course (Ghosh study) Paradigm would have met the endpoints of the trial against a placebo-controlled administration. The current study is using double the total dose in the treatment course with a far better trial design.

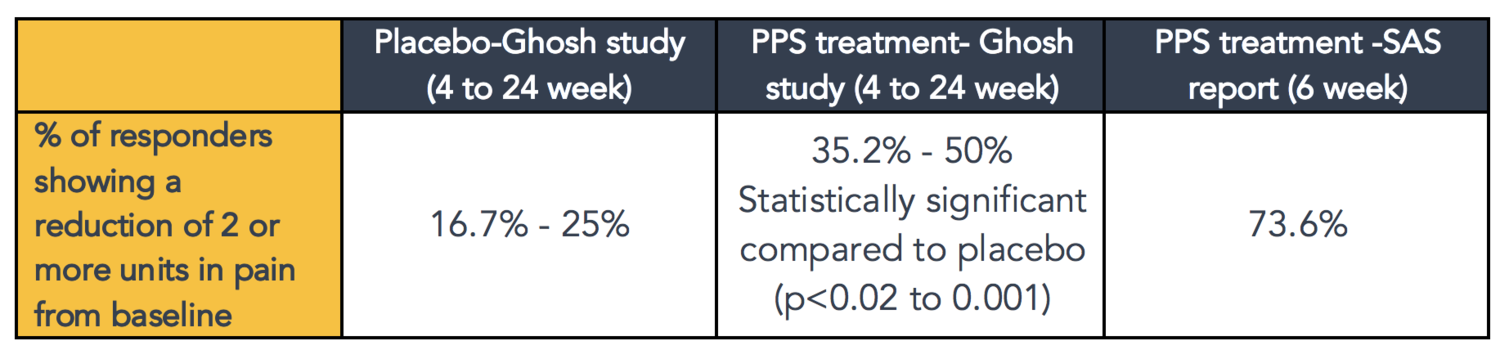

To further demonstrate the likelihood of a highly statistically significant result, we have used the placebo results from the Ghosh study, and compared these against Paradigm’s SAS data. In the Ghosh study, pain measurements were taken at 4, 8, 12 and 24 weeks. Within the SAS data, the pain scores have been recorded after the final 6-week injection. NOTE: Our discussions with doctors as well as patients who have been treated with Zilosul® state that the pain reduction and benefit of the drug typically continues after the last injection. This is why in Paradigm’s clinical trial the pain measurement is taken 6 weeks after the final injections. We anticipate the placebo effect in the Paradigm trial will be significantly lower than the Ghosh study and the pain reductions will also be materially higher due to an improved trial design.

The table below is a summary of the percentage of subjects that responded to either placebo or PPS treatment in Ghosh’s study, with a pain reduction score of greater than or equal to 2 from baseline using a VAS pain scoring system. The percentage of SAS patients treated with PPS who responded by showing a pain reduction score of a greater than or equal to 2 using the NRS were compared in the table below.

The Ghosh study showed there was a statistically significant increase in responders in the PPS treatment group compared to placebo.

The SAS data compared to Ghosh’s data showed a higher response with iPPS treatment, which is due to differences in dosage. The Ghosh study dose was 3mg/kg of iPPS weekly for 4 weeks (total dose for a 50kg person is 3 x 50 x 4 = 600mg) versus the SAS study/Phase 2b OA trial dose of 2mg/kg of iPPS twice weekly for 6 weeks (total dose for a 50kg person is 2 x 50 x 2 x 6 = 1200mg). Based on these comparisons, we expect that the OA trial should yield data demonstrating a statistical significance for iPPS treatment versus placebo and meet its primary end point of a change in pain score from baseline.

Based on the SAS data presented on 145 patients, we believe that Paradigm will pass their upcoming Phase 2b clinical trial for OA. As demonstrated above, the risk of failure in this clinical trial we estimate is below 1%, yet the pay-off from current valuations appear materially higher than what the current share price represents.

Paradigm Investor Presentation 25th October 2018.

PAY-OFF: OSTEOARTHRITIS

Now that we have shown investors that you can forecast success in the clinical trial, what is this company worth? Remember, price and value can be materially disconnected.

We feel Australian investors (who make up the majority of Paradigm’s shareholder base) drastically undervalue how big this new drug will be. One word – Blockbuster!

As defined by Investopedia - OA is a common problem!

How can you work out the value of this drug? Our view is that price and value are two different things. Eventually the share price investors see will reflect the value of what this drug will be worth to a big pharmaceutical company. While Australian investors are extremely conservative on these valuations, soon enough this company will begin to be valued by American funds and pharmaceutical companies.

Looking at comparable deals that have already been done in the indication of OA, we believe that the starting bid for any deal with Paradigm on Zilosul® will be in excess of US $2 billion.

The total deal size could potentially exceed US$4b. BIG DEAL: ANTI-NGF’S VERSUS ZILOSUL®

Before people discount these numbers, let’s look at some facts.

The most significant area that has been explored by big pharma to treat OA has been the development of Anti-NGF (Nerve Growth Factor) drugs. Pfizer has collaborated with Eli Lilly on a drug called Tanezumab.

This collaboration sees an equal share of product development expenses. Pfizer received an upfront payment of $200m in March 2015 from Lilly for this collaboration. Lilly would commit another $350m in regulatory milestones and $1.23b in sales milestones. All up, this deal is worth US$1.8b before the drug is even commercialised. Tanezumab has had a number of issues and was put on clinical hold by the FDA for safety concerns. It’s now in a phase 3 trial and has been granted fast track designation from the FDA. Their initial results have been released and it looks to be statistically significant. However, when comparing these results to Paradigm’s SAS data, Tanezumab does not appear as effective as Paradigm’s Zilosul® in the treatment of OA.

The difference in composition of the drug also favours Paradigm’s Zilosul®. Tanezumab is a biological and monoclonal antibody directed to act against NGF and would need to be refrigerated when stored. Zilosul® is a polysaccharide and is stable at room temperature. The cost of production of Zilosul® when compared to the manufacture of the biological Tanezumab would also be significantly lower. Zilosul® is administered at a dose of 2mg/kg twice weekly for 6 weeks. Tanezumab is given at a dose of 10mg/kg and administered every 8 weeks.

Comparisons between Paradigm’s SAS patients (Real World Evidence in N=145 patients) and Pfizer’s Tanezumab (anti-NGF) from their trial (Birabara et al 2018) are summarised in the table below.

In summary, the data demonstrates that 53.5% of Tanezumab subjects versus 60.8% Zilosul® subjects responded with a 50% reduction in pain from baseline.

As demonstrated below, Tanezumab saw statistical significance in a double-blind placebo controlled trial. Yet as we show, the pain reduction being recorded from Tanezumab next to Zilosul® is not as good. This gives us further evidence that even against a placebo it’s likely Paradigm will pass their upcoming Phase 2b OA trial.

Tanezumab achieved statistical significance against placebo. Paradigm’s Zilosul® achieves a higher level of pain reduction than Tanezumab, so should also be statistically significant.

In the Tanezumab clinical trial the adverse event of rapidly progressing Osteoarthritis was observed in the treatment group and not in the placebo group. Pfizer was forced to cut back doses from 20mg to 10mg in order to overcome the severe safety challenges - but reduced efficacy was observed for the lower dose.

So not only does Zilosul® demonstrate a comparable reduction in knee OA pain relative to Tanezumab, Zilosul® also has the advantage of improving knee function without further deterioration of the knee joint as demonstrated with Tanezumab.

Table showing percentage of patients who suffered Adverse Events (AE) as a result of treatment with Tanezumab.

The real-world data from Paradigm’s SAS program is clinically meaningful and in association with Paradigm’s Phase 2b results would be of interest to the FDA. Of particular interest, is that Zilosul® does not induce accelerated OA as is reported for Tanezumab.

Therefore, to put it simply, Tanezumab is the only NGF product that currently looks like it may be able to be commercialised as a treatment for OA, in a deal that is worth US$1.8b (before it has even been brought to market) as valued by two of the largest pharmaceutical companies. Tanezumab has previously been put on clinical hold by the FDA and has seen numerous adverse events to patients being treated. This drug next to Paradigms Zilosul® is essentially like comparing a Nokia (Tanezumab) to the iPhone (Zilosul®.

Try selling a Nokia against the iPhone…

Another Anti-NGF drug developed by Teva and Regeneron, who spent US$250m to develop their anti-NGF Drug (Fasinumab), is another contender. Their drug was put on clinical hold from the FDA for safety concerns. A drug they were ready to spend over $1.3b on developing (maybe they can re-invest that towards Paradigm’s Zilosul®?)

Or perhaps Johnson & Johnson might be interested? They shelved their Anti-NGF after safety concerns after being placed on clinical hold by the FDA. J&J are also familiar with PPS from their current use of it in their drug Elmiron (to treat bladder infection) so they would be comfortable with the safety profile of PPS and the supplier Bene pharmaChem.

There is also Sanofi, AstraZeneca, Merck or Amgen to name a few. These are extremely large bio-pharmaceutical businesses who have tried and failed to successfully bring an OA drug to market. When comparing what is out there next to Zilosul®…if you don’t have Zilosul®, you have a Nokia!

The table below shows the market cap/revenue/cash holdings of some of these companies who might be interested – measured in billions.

Again, price and value are very different. It is our estimate that when Paradigm have a successful Phase 2b trial for their OA drug, these major pharmaceutical companies are going to be extremely interested in licensing Zilosul® from Paradigm. We realistically estimate this deal is going to exceed US$2b in total deal size given Tanezumab was worth US$1.8b.

Given the safety and efficacy data from Paradigm’s real-world evidence we can also see Zilosul® gaining fast track approval from the FDA. This means a smaller Phase 3 trial (estimated around 500 people) and getting the drug to market faster. Big pharma could have a fully approved and commercialised drug by the end of 2020. Given the sheer demand for a non-opioid based product to treat OA, it is likely that this opportunity is far too valuable for a big pharma to pass up.

Paradigm have also just signed a deal to treat elite sports players in the US. Having positive headlines from super star sports players will also appeal to the likely acquirer (great marketing that will rapidly ramp up sales). When this feedback starts next year, we anticipate a significant increase in demand – as witnessed from the TGA SAS program in Australia.

Which one would you buy? The one used by sports legends or the one that could see rapid joint deterioration? This also likely attracts a premium when pricing the drug.

News articles comparing Tanezumab and Zilosul®.

When you consider that Zilosul® will also be able to treat other OA indications outside of the Knee, you have a patient population with OA of over 30 million in the US alone. Even if it could only achieve a price point of US$1000 this is a total addressable market in excess of $30b in revenue per year. SUMMARY

Zilosul® will become the standard first line treatment for OA once commercialised.

As demonstrated, we consider the risk of failure in Paradigm’s Phase 2b OA clinical trial as less than 1% when you compare the results already being seen via the SAS data. Compare them against prior trials with placebo control and against other NGF drugs, it’s starting to look like Paradigm are going to have the best OA product for the foreseeable future.

When this trial is successful, we believe the negotiations from Big Pharma will result in a deal too good to refuse. This deal size will likely need to exceed US$2b in order to be reflective of the Anti-NGF deals done (remembering these appear to be inferior next to Paradigm’s Zilosul® – demanding a premium for Zilosul® over Anti-NGF drugs). We see upside risk to the size of this deal given the competitive tension that is likely to result as big pharma understand that Zilosul® should become the preferred treatment for OA around the world. To put this into perspective in terms of PAR.ASX share price, a US$2 billion-dollar deal on the current issued capital would result in an AUD equivalent price of $19.80 per share (140m shares on issue).

We are confident that US based investors who are familiar with US big pharma will very quickly realise the value of a successful Phase 2b trial.

Remember, value is what someone is willing to pay and to big pharma, if you don’t have Zilosul® – you have a Nokia.

iPhone released - Nokia & Apple both have market capitalisations of US$100 Billion PARADIGM - SO MUCH MORE THAN A ONE HIT WONDER

Paradigm announced on the 22nd of November that they have In-Licensed a treatment for Mucopolysaccharidoses (MPS).

MPS is a group of metabolic disorders caused by the inherited absence or malfunctioning of lysosomal enzymes that are needed to break down large complex sugar molecules like Glycosaminoglycans (GAGs). Basically, people with this disorder don’t produce enough of these enzymes and over time it causes joints to become stiff and painful. This disease has a lot of symptoms that are commonly associated with OA.

This is a very rare disease, however, it is estimated around 1:26,000 births would have one of the MPS types. This would mean that across the world, an estimated 300,000 people would have a type of this disease.

There is currently no cure for MPS, only symptomatic treatment to try and improve the persons quality of life. Currently the only treatment involves enzyme replacement therapy (ERT) which has been useful in reducing non-neurological symptoms and pain. However, the ERT does not treat the accumulation of GAGs which are stored in the cells and tissues (joints). This accumulation of GAGs lead to inflammation in the joints causing pain and immobility.

A recent Phase 2a study (Hennermann et.al.) was undertaken using iPPS (Pentosan) to treat the accumulation of the GAGs and associated pain in patients with MPS - which yielded significant results.

The iPPS has already been granted orphan designation status (by both the US FDA and European EMA) in the treatment of MPS and as such has an expedited pathway to market. We anticipate Paradigm will conduct a double-blind, placebo-controlled Phase 2b trial in order to commercialise the drug. As the disease is an orphan indication and very rare, it’s likely the size of this trial would not be excessive. It is unlikely a Phase 3 would be needed to bring this to market due to the severity of the disease. This means that the drug could be commercialised, and sales ramped up very quickly.

We weigh any trial in this indication with a high probability of success based on the data released to date from the MPS animal studies, MPS Phase 2 clinical study and from Paradigm’s SAS results in patients with moderate to severe knee Osteoarthritis.

The below results are taken from the recent MPS study (Hennermann et.al.) and show the positive effects for treating MPS with iPPS.

PEER COMPARISONS

Orphan indications are very small markets, and MPS is a great example of a small market where successful drugs can have a material impact on a patient’s health, while generating significant revenues for the owner of the drugs patent.

In our research and discussion with key opinion leaders, we believe Paradigm is likely to have a product that will be able to treat most of the MPS genetic variants. Initially the MPS variants 1, 2, 6 and 7 and second line for MPS 3 and 4.

However, given the results seen to date, it could be argued that any lysosomal storage disease that has associated joint mobility, stiffness and pain issues associated with inflammation and GAGs may see benefit from treatment with PPS.

Working on the ratio of 1:26,000 births for MPS and only looking at the developed world, we estimate the total addressable market of ~50,000 people.

Discussions around pricing at these early stages is always difficult. However, the initial indication from key opinion leaders ranged from $50,000 to $100,000 per year per patient for treatment. The current therapies we explore further on typically cost between $200,000 & $400,000 per year (depending on the patient’s weight). It is worth noting that iPPS won’t replace the current therapy but could be used concurrently with ERT (as demonstrated by Hennermann et.al.) or as a mono-therapy in MPS sub-types where ERT is not approved for use.

To outline further the revenue opportunity, it is worth exploring the current Enzyme Replacement Therapy (ERT) used for MPS. These are drugs made by NASDAQ listed BioMarin.

BioMarin is valued at ~US$18 Billion and focuses on enzyme technology for rare diseases.

The 3 drugs BioMarin have on the market for MPS treat only 3 of the 7 MPS strains. These are:

Aldurazyme (MPS 1)

Naglazyme (MPS 6)

Vimizin (MPS 4)

Below is a graph showing the revenue each one of these product lines generate for BioMarin (Note Aldurazyme is a 50/50 JV with Genzyme (Sanofi) – sales of Aldurazyme were $207m in 2017). Total revenue from these 3 drugs was US$952.5m in 2017.

The pricing for each drug varies based on the patient’s weight, however through our research we determine the average cost is around $200,000 per year.

BioMarin revenue earned from MPS ERT drug.

We estimate this US$952.5 million in revenue was generated from between 4,000 – 6000 patients.

Ascribing value to these drugs, we look at BioMarin’s 3 MPS drugs as a percentage of total revenue and a percentage of their enterprise value (EV). This shows a value of US$10.5b that is attributed to these 3 MPS drugs.

The key difference between BioMarin’s drugs and Paradigm’s will be price. So, depending on the sensitivity we need to discount back this potential value as it will ultimately sell for a lower price.

However, it must also be remembered that the addressable market for Paradigm’s drug could be far larger than the three being sold by BioMarin and Genzyme – which probably adds significant value, but for the sake of conservatism we will assume no additional patients to be treated.

Assuming this is the addressable market (5,000 people) for Paradigm’s potential new drug, this would generate the following revenue at the below price points:

On our most conservative estimates (treating only current ERT patients and at a price point of only $25k) we estimate Paradigm could generate around US$125m per year.

Although we believe pricing is more likely to be around $50,000 per year per patient on average, which would generate $250m on only the existing patients being treated with ERT. Revenue of $750m could be earned assuming treatment of a larger patient population using this same price point.

Upon a successful Phase 2b trial and commercialisation of the product, the value could increase materially. Should Paradigm achieve revenue/EV valuations similar to BioMarin the valuation could be somewhere in the range of $2b to $10b based on the above sales range. Although we believe it will be on the lower end of this range given ERT is a higher priority treatment.

The real question investors should ask: What is the discovery and potential commercialisation of this drug worth to BioMarin or Sanofi - (Sanofi acquired Genzyme for US $19.6b in 2011).

Paradigm’s PPS doesn’t compete with these companies, rather it is used concurrently with ERT, so it would not cannibalise sales. Not everyone is eligible for ERT treatment. ERT hasn’t been shown to reduce the joint pain and dysfunction in MPS so this is complementary to the ERT as demonstrated by Hennermann et.al.

As a result, Paradigm’s PPS likely has a far larger addressable market. Another likely benefit to BioMarin is the possibility of a ramp up in sales very quickly given their existing patient population. So, what is this worth to BioMarin?

Realistically, we believe the addressable market is far larger than BioMarin’s existing patients, and the drug would be priced more aggressively than our lower estimates. In terms of revenue, this is potentially a recurring revenue opportunity of >US$500m to BioMarin once commercialised. Given Vimizin has an attributed value of an estimated US$5b on sales of similar magnitude, it could be argued BioMarin could pay a significant premium for such a product.

We think Paradigm will undertake the necessary steps to reach commercialisation. At that point we think BioMarin or Sanofi would be very interested in doing a deal for this drug.

Given the recurring nature of this revenue, orphan status of the drug (giving a monopoly) and demand from these big pharma, this deal could easily exceed US$1b in total deal size. We estimate the deal might look similar to the Aldurazyme deal whereby Paradigm would supply the drug and receive a 50% margin on sales.

BIOTECH BLOCKBUSTERS MOVE FAST!

We believe many investors don’t really understand just how quickly these biotech deals can evolve, or how significant the upside might be for investors.

While there are countless examples, we will use Paul Rennie’s (CEO of Paradigm) previous company – Mesoblast. Not only does this show that the team have experience executing billion-dollar deals, but just how fast valuations can extend.

Mesoblast is a company that focuses on Stem cells and in December 2010 they signed a US$1.7b deal with Cephalon to commercialise ‘Novel Therapeutic Products for Regenerative Medicine’. At the time Cephalon had an EV of around US$4.5b, revenue of US$2.8b and profits of US$500m.

Below are some excerpts from the announcement made on the 8th of December 2010 from Mesoblast.

After the deal was announced, MSB valuation went to an Enterprise Value (EV) of ~US$2.3billion (note the AUD to USD exchange rate was around $1 - $1.10 over this period). The deal involved issuing around 20% more stock to Cephalon which caused the issue capital to increase significantly. Should no equity component have been attached, the underlying share price may have extended even further.

Graph showing Enterprise Value (EV) of MSB (white line) and corresponding shares on issue (green line).

To illustrate how quickly the share price appreciated, the below chart shows the price of MSB in just one year. Perhaps the most amazing thing about this rapid price appreciation is that the product was prior to a successful Phase 2b trial.

Share price graph of MCB from May 2010 until June 2011 (1 year). OTHER DEAL COMPS

To reiterate how big these deals are, let’s look at some other comparisons: Flexion $1b: (US listed company NASDAQ:FLXN). Flexion have a drug called Zilretta, which is essentially a corticosteroid (being marketed as a better product than the current corticosteroid injections).

After passing a Phase 2b trial, it was rumoured Sanofi was going to offer US$1b in cash for the company. The stock went from a market cap of US$200m to US$1b. The share price has since faded as sales have not lived up to expectations (as you would expect trying to sell a product that is comparable to current treatment for a significant premium). Galapagos: Gilead (NASDAQ:GILD) entered a deal with Galapagos (NASDAQ:GLPG) for their drug Filgotinib after success in their Phase 2b trials for Rheumatoid Arthritis. This deal was US$2.075b with a US$725m upfront payment. Galapagos will also receive royalties starting at 20% on sales.

Rheumatoid Arthritis (RA) affects around 1.3m Americans. Whereas Osteoarthritis is estimated to affect 30m Americans. This deal was north of US$2billion.

Share price and market capitalisation of Galapagos after the deal with Gilead. Share price appreciated ~475% and market cap from ~$400m to $2.4b.

Given the size of the OA market compared to the RA market, this deal could also be a ‘base case’ for valuation. We believe Paradigm’s deal should be of similar magnitude, or larger… Oh, did we mention Paradigm are also looking at the Rheumatoid Arthritis market?

Taken from Paradigm’s investor presentation on 25th October 2018.

As we have already illustrated, Paradigm’s OA indication is likely going to fetch a deal in excess of US$2b (around $2.77b AUD at 72c exchange). Given a successful result in this trial investors may start to look at the other indications Paradigm have and assume further ability to commercialise products.

Realistically we expect a deal on their Ross River/Chikungunya of around US$250m - US$500m as we also believe this trial will see success (results are estimated to be read out January 2019). The MPS could easily be valued over US$1b and the OA for US$2b. This would give an AUD market cap equivalent of close to $5b or over $30 per share (while also accounting for an additional 15% increase in issued capital).

When you think about it, are these numbers that crazy? Or are investors grossly underestimating how big this could be and how quickly this can happen?

We believe this material disconnect between price and value is being fuelled from investor fears from other recent failures in Australian biotech. This has created an opportunity for those investors willing to roll up their sleeves and do the work.

As we have said, never have we seen such an extreme asymmetric risk/reward investment when the catalyst for such deals and re-ratings are potentially hinging on a successful Phase 2b trial result…which as we’ve showed, you already know works.

Let’s not even discuss the blue sky… Maybe next time? Below is a timeline for Paradigm’s upcoming news from their recent presentation.

ABOUT FIFTYONE CAPITAL AND THE PROGRESSIVE GLOBAL FUND - GIVING OUR INVESTORS MORE

When we set up our fund, we wanted to do something different, and change the way people look at our industry. Our view is that there is inherent conflict between standard sell side research and those who read it. This is because the company producing the research notes, is usually receiving compensation. Compensation that the clients don’t receive [as producing research is part of their business]. It becomes difficult to know why research was done, for what purpose and for who? Our business model seeks to change this – by giving back to our investors.

Putting our Fund’s name alongside the companies we invest in can have associated risk, so we are extremely selective on the companies we write research on. We take a quality over quantity approach and seek to build a strong track record for identifying under the radar companies, with significant upside potential relative to the risks.

This deep dive research is part of what we do as fund managers. So, to share this research we will receive compensation from the company usually in the form of options, or shares, as we prefer to leave the cash inside the companies we invest in.

These options we then allocate back to our fund, so our investors (unit holders in the fund) are able to share in the benefit of these options. So, our investors not only benefit from this stock selection, but will also benefit from this additional alpha we return from these deals. Should the investment community use our research and we maintain a strong track record for identifying undervalued companies, this strategy should continue to provide more return for our investors.

Hopefully by sharing research like this and remaining transparent with our business model we can make things better for everyone. We always strive to give our investors more and will seek to maintain our track record for stock selection.

If you would like to be part of our fund and access additional alpha and research like this, please don’t hesitate to get in touch [email protected]. Disclaimer: This information has been produced as part of our internal research on Paradigm. While extensive research has been conducted, please cross check the facts and sources of this information. This note is not a recommendation nor is it advice and should be considered general in nature. Please do your own research on the company and seek financial advice if required. We own shares in Paradigm Biopharmaceuticals (PAR.ASX) and have previously received compensation in the form of options to share our research on the company.

Sources:

Quote from Flavia Cicuttini of Monash University. LINK

Paradigm’s Phase 2b OA Clinical Trial end points. LINK

A personalised tool to help users track selected stocks. Delivering real-time notifications on price updates, announcements, and performance stats on each to help make informed investment decisions.

works, even if it just slows the progress, you don’t need to cure it, you could change the pattern of the disease”. – Flavia Cicuttini, Monash University

(20min delay)

(20min delay)