But then of course longere term there is this;

By Lisa Abramowicz

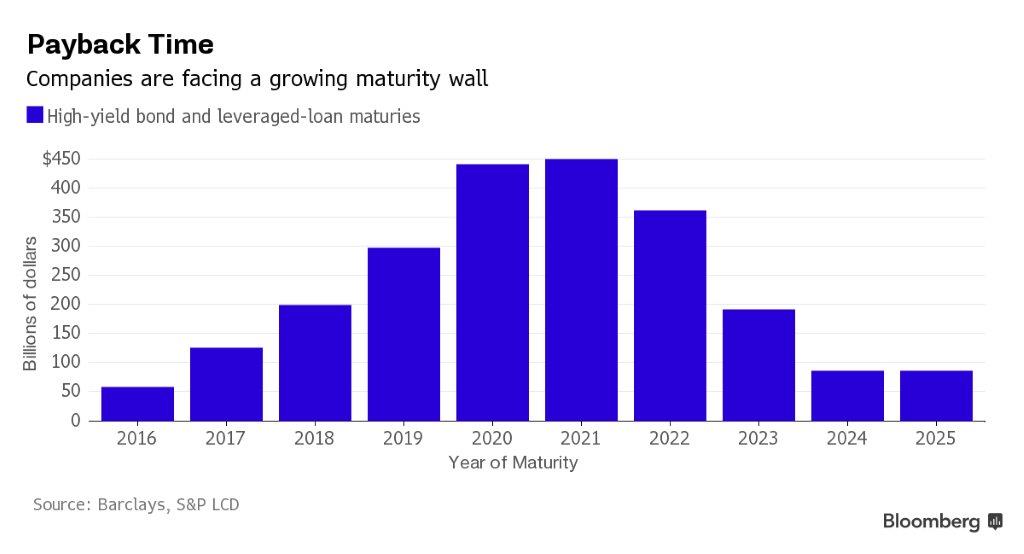

How’s this for a potential disaster: Traders are betting that the Federal Reserve will steadily raise borrowing costs just as companies face an accelerating rash of debt coming due.

While interest rates have been about zero since 2008, enabling companies to borrow trillions of dollars relatively cheaply, derivatives traders are betting the Fed will raise those benchmark rates to 1.83 percent by November 2018, data compiled by Bloomberg show. Speculative-grade corporations have about $200 billion of debt coming due that year alone, according to data compiled by Barclays.

The wall of debt maturities steepens from there. The companies will have more than a trillion dollars of debt maturing in the three years after that, the data show. And it’s already becoming more costly for lower-rated companies to refinance their bills, even with interest rates bottomed out. Average yields on junk bonds have already risen to 7.9 percent from the record low of 5.7 percent in June 2014.

The best-case scenario is that the economy accelerates drastically, allowing these companies to pay off their investors without incurring more debt, regardless of whatever action the Fed takes. The worst-case scenario, on the other hand, is that investors refuse to lend more money to these companies, which are forced to lay off employees and file for bankruptcy, helping push the U.S. back into recession.

Of course, the predictions by derivatives traders may turn out to be wrong and the Fed may wait longer to push up rates. U.S. central bankers have already said they plan to hold rates relatively low for a longer-term period because they are not anticipating inflation to rise sharply in the near future. And bond traders have generally agreed. Yields on 30-year Treasuries are at 3.1 percent, compared with 4.8 percent on average over the past two decades.

But after an unexpectedly robust U.S. jobs report on Friday, which exceeded nearly all analyst projections, traders started to think that perhaps U.S. wages and consumer prices are poised to increase a little more than they’d thought before, forcing central bankers to increase benchmark rates a bit faster. Traders are now betting there’s a 70 percent chance the Fed will raise rates next month for the first time in more than a decade, from just a 56 percent likelihood on Thursday before the employment report.

Futures traders now bet there’s more than a 20 percent chance the Fed will have raised rates above 1 percent by this time next year, data compiled by Bloomberg show.

That could create a conundrum. Let’s say yields on the safest U.S. debt start increasing steadily, regardless of continuing monetary stimulus in Europe and China. Unless the U.S. economy surprises everyone and accelerates without the help of meteoric growth in developing countries, why wouldn’t investors plow into Treasuries? They could actually earn something real, unlike the post-crisis years when yields on 10-year U.S. government debt fell as low as 1.4 percent. They would have far less incentive to pour more money into highly leveraged companies, just when those companies needed it the most. And even if investors were inclined to buy more of their debt, they would certainly demand a hefty premium, driving up the costs for the companies.

Historically, the Fed raised benchmark borrowing costs to tame inflation and prevent growth from spinning out of control. This economy doesn’t appear to be at risk of overheating. If derivatives traders are right, the Fed could be setting it up on a collision course with a deepening default cycle.

(20min delay)

(20min delay)