Medusa Mining - In Defense Of A Turnaround Story

Nov. 14, 2014 11:26 AM

Summary

Medusa Mining has declined 75% year to date, making it one of the most unloved gold miners of any of its peers.

The new management team is changing the philosophy of the company, ensuring that guidance is set at a level that the company can beat, unlike under the prior management team.

The initial portends look good - with Medusa exceeding its third quarter production guidance at the lowest cost so far this year.

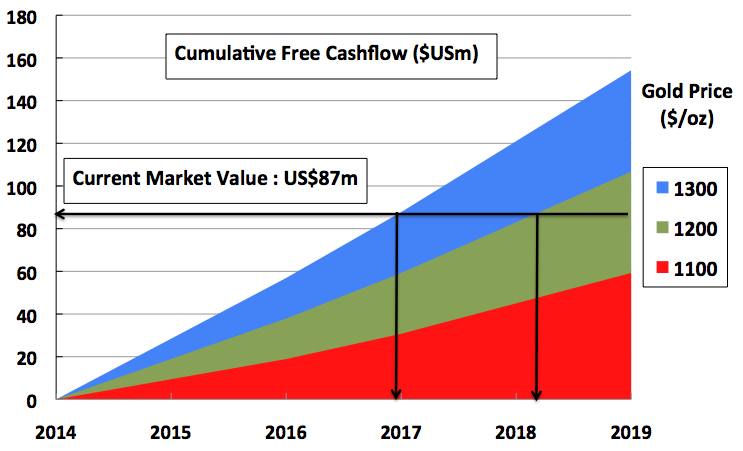

Medusa is set to generate its market value in cash flow by June 2018, based on a constant gold price of $1200/oz and management's production and cost guidance, released last week.

Medusa's market valuation is now at a point where it represents a compelling investment.

(Editor's Note: Investors should be mindful of the risks of transacting in securities with limited liquidity, such as MDSMF. Medusa Mining's listing in Australia, MML.AX, offers stronger liquidity.) Medusa Mining - An introduction and recap

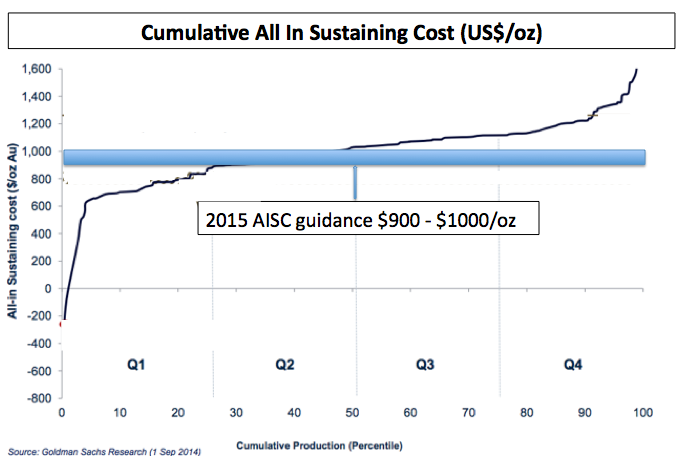

Medusa Mining (OTCPK:MDSMF) is an ASX listed junior gold miner with mining operations based on the Philippine island of Mindanao. Last fiscal year (to 30 June 2013) it produced 60 koz of gold at an average C1 cost of US$418/oz and head grade of 4.76 g/t. For the year to 30 June 2015, management has forecast production of 90 - 100 koz at an average C1 cash cost of US$400 - US$450/oz and All In Sustaining Cost (AISC) of $900 - $1,000/oz. Results for the first quarter (to 30 September 2014) are encouraging - 21 koz at C1 cash costs of US$382/oz and head grade 5.02 g/t.

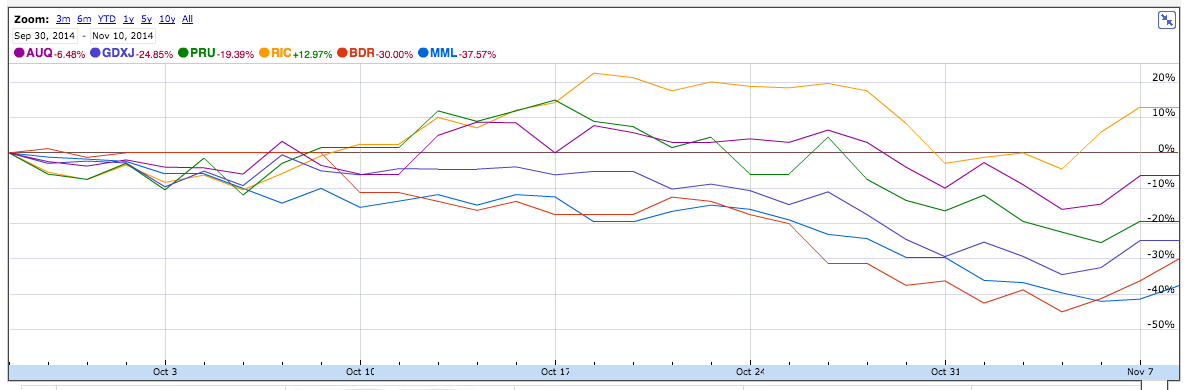

Despite the promising start to the 2015 fiscal year, Medusa's (MML) share price has slipped further, underperforming many of its peers. (click to enlarge)

Source: Google Finance

Last month, I published a note on Medusa which argued the company was undervalued. You can find it here.

In the article, I suggested that the recent history of disappointing performance and missed management forecasts was coming to an end with the return of the company's founder (Geoff Davis) to the CEO position and the appointment of a mining consultant (whose report is due to be finalized this month) to review MML's operations - drawing a line under the previous management of the company. I believed that the company's September quarterly results would be the trigger for a re-rating.

A month later, and although the share price has slipped further, I continue to believe that the company has turned the corner. New management has made a particular point in ensuring it meets its released guidance and its initial test (the third quarter results) was passed.

Medusa's valuation is now at a point where, even if it doesn't improve any further on the cost side (notwithstanding the efficiency improvements that the company has initiated in July) and even if gold were to remain at $1200/oz over the period between now and June 2018, the company would generate its own market value in free cash flow - US$87m - in that time. Medusa Mining - The (past) ugly, the bad ...

Without a doubt, Medusa has had a lackluster couple of years and has been plagued by a number of issues. Some of these issues were undoubtedly the existing management team at the time's fault, and some of them were just bad luck and outside its control.

These issues included the commissioning of the new mill, which took many months longer than it should have due to problems with its power cells. Then, once it was commissioned earlier this year, problems with one of the crushers meant it was operating below capacity and at a significantly higher cost.

There was also the spectre of the revision of the company's reserves and resources under the more recent 2012 JORC code (which is particularly punitive on thin vein deposits like MML's).

Then there was the issue of the company's record over the last couple of years of failing to meet its guidance and live up to the expectations set by its previous management team.

Lastly were the concerns in the minds of some - in the absence of any real firm guidance in the past on AISC, it must be said - of the cash flow viability of the company. ... and the good

So what's changed at Medusa these last few months to address the challenges above? The short answer is quite a bit: i) Management changes

In replacing the old CEO with the founding CEO - who has a long history with South East Asian mining projects - there is more reason to believe the mistakes of the past won't be repeated. What gives me confidence is that the new team seems to understand the need to rebuild credibility with investors and, as a result, is taking the whole process of setting guidance more seriously and cautiously. So far, in the weeks since taking over, the new team has announced (and met or bettered) guidance on third quarter production, grade and cost. This gives me confidence that they will likely likewise meet the full year production and AISC guidance (released just last week). ii)Appointment of a mining consultant to redesign and optimize the mine plan

Early September, the company announced that it had set about commissioning a "comprehensive review of the company's operations" in order to optimize the Co-O mine's long-term mine planning. Last week the company said the review is due to be completed this week and the results presented to the board shortly thereafter. One of the key outcomes of the review was production guidance for the 2015 fiscal year, which the company has now released and set at 90-100 koz. This was a positive development, given earlier guidance for the 6 months to December 2014 was set at 40-45 koz and suggested perhaps production below 90 koz for the full year. Along with the guidance, the company also announced that "Operational efficiencies and cost reductions are being instituted as the review progresses" which provides some hope that the recent large reduction in manning levels announced in July are starting to come through the numbers. iii) JORC restatement

MML's reserves and resources had been stated under the JORC 2004 code (which did not impose limits on vein widths - just minimum grades). The company recently restated its reserves and resources to the newer JORC 2012 standard - which imposes minimum vein thicknesses. The upshot is that whilst a reduction was anticipated, at 120 koz, it was not as severe as some expected. Further, finalizing the new reserves and resources removed one of the main sources of uncertainty overhanging the stock. Importantly, although the 120 koz of excluded reserves no longer meets the required vein thickness (and is thus not included in the revised reserves and resources), it nevertheless remains present and high grade and thus remains minable. iv) Released production and cost guidance for 2015

The new management team has been cautious in setting cost and production guidance - rightly realizing the need to be very sure of meeting it in order to restore investor confidence. Last week, the company set production guidance at 90-100 koz and AISC US$900-$1000/oz. Whilst this is not first quartile, it is firmly within the second and, with gold prices currently range bound US$1150-US$1250/oz, allows a comfortable margin for free cash flow generation, even allowing for the expansion capex the company has set for the L8 and E15 shafts ($1m this year for L8 and $12m over 2.5 years for E15). (click to enlarge)

Source : Oceanagold Investors need to keep in mind what Medusa ISN'T when evaluating it

Before going into an analysis of MML's current valuation, it's important to realize what MML isn't. It isn't a tier one operation, but nor does it promise to be. It's a second quartile ASIC operation, with the potential to possibly move further down the cost curve once the optimization and cost cutting measures it is putting in place take effect. Also in its favor, incidentally, is the fact that a significant portion of its costs are non-USD denominated, and with continued appreciation of the USD, this should help offset any declines in the gold price on account of USD appreciation.

But the above is fine in my view because the attraction with MML lies in the fact that its share price has now fallen so far that it represents compelling value on a risk adjusted basis, despite not being a tier one first cost quartile operation. In fact the valuation is now so low that it provides a significant margin of safety. A declining risk profile...

One of the issues with MML up to now has been the high degree of uncertainty hanging over the company. There was the uncertainty around the company's reserves and resources under the new JORC, there was the uncertainty related to the fact that the company only provided guidance for 6 months to December 2014 (rather than for the full fiscal year to June 2015) and then there was the uncertainty around the mill performance. MML has been busy addressing each of these - removing this uncertainty as it goes. Whilst there is still some tweaking of the mill performance to bed down, much of the underperformance of the mill which plagued the company earlier this year has been arrested. ... contributes to what is a compelling valuation proposition

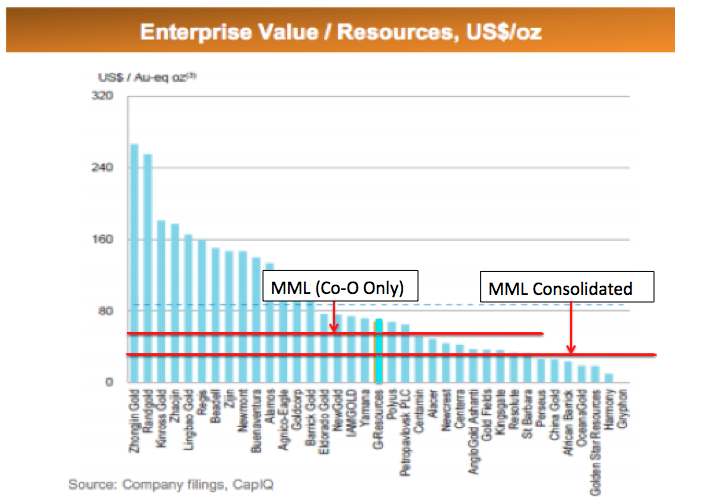

On a range of valuation metrics, MML looks cheap relative to its peers. It trades below the average on an EV/resources basis, even if you only take the resources of the Co-O mine into account (i.e. ignoring the Bananghilig deposit). (click to enlarge)

Source : G Resources

On a reserves basis, MML trades at a narrower discount to the average - about $190/oz compared to the average of its peers (around $200/oz-$230/oz). Part of the reason for this is the removal of 120 koz of reserves, forfeited in moving to the new JORC standard. These 120 koz of previously certified reserves are now ineligible for inclusion in the company's certified reserves due to vein width - however, they are high grade and haven't disappeared. They remain available to the company to mine.

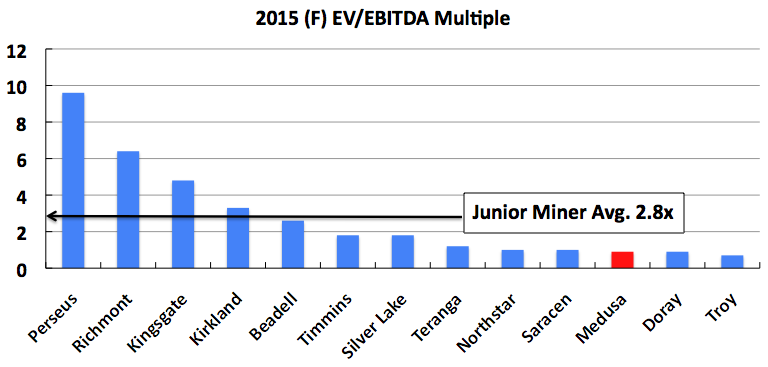

On an EV/EBITDA basis also, MML offers compelling valuation. The chart below is based on GS data and shows MML now trades at a significant discount to its junior miner peers. (click to enlarge) Source : GS

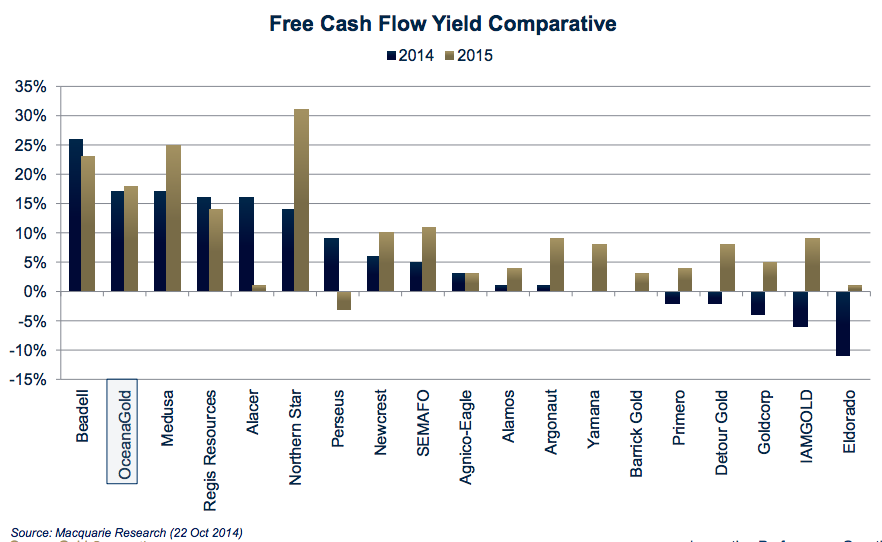

And lastly, on a free cash flow yield basis, again the data points to MML trading at a material discount to the peer group average. This is perhaps the most telling chart of all. It suggests that MML should generate 25% of its total market value in free cash flow in 2015. Also interesting is the size of the cash flow increase forecast for 2015 over 2014. The analysis comes from a November Oceanagold presentation which cites Macquarie bank as its source. (click to enlarge)

Source : Oceanagold, November 2014 At the end of the day, cash is king

The last chart above points to the compelling valuation of MML based on its cash generation fundamentals, and sourced from Macquarie Bank data.

My own analysis builds in more conservatism. I use constant gold prices for the period June 2014 to June 2019. Macquarie's average (used in the above chart) for 2015 is $1,330/oz, and increases each year after this. My analysis also assumes AISC of US$950/oz and production of 95 koz (i.e., the midpoint of management's guidance last week), as well as including the $12m (which I assume is expansion capex and outside of MML's AISC forecast) for the completion of the E15 shaft over 2.5 years. My analysis is based on June year ends and shown below. (click to enlarge)

Source : Author

My analysis suggests that at a constant gold price of $1200/oz over the forecast period, based on MML's forecast production and AISC, the company will generate its own cash adjusted market value by June 2018. If you assume that gold averages $1300/oz, then it drops a year sooner - to June 2017, i.e., a cash payback period of 2.5 years. So why has Medusa continued to underperform since it released its third quarter results?

A recent article on the essence of value investing I think is very pertinent and points to the patience required for successful value investing. You can find it here.

In it, the author cites the fathers of value investing, Dodd and Frank, in pointing out that often successful value investing yields short-term declines in value. This is because value investment opportunities, by their nature, are created when underlying value dislocates from current market value. One of the principal drivers of this dislocation is market sentiment. In other words, it is often negative sentiment surrounding a stock that drives it lower than its intrinsic value - often significantly overshooting it. At that point, a catalyst is required to alert investors to the undervaluation, which can be an earnings release, an acquisition of some other piece of positive news.

Value investing under these circumstances can be testing, as although analysis of the company's underlying position suggests it's undervalued (in the case of MML, its likely cash generation potential compared to its market value), often the share price will drift lower over the short term. Conclusion

Medusa has had a torrid time this year. Its share price has fallen over 75% year to date - making it one of the worst performers of its gold mining peers.

Part of the problem is a loss of investor confidence - years of missing guidance and operational uncertainties have weighed on the company's share price.

But that is now changing. Much of the uncertainty overhanging the stock has now been removed or addressed and with a new management team in place, the culture has shifted to one of making sure any guidance issued is met, as was done most recently last month with the company exceeding its third quarter guidance.

Medusa's valuation has now fallen so far that it trades at price to book value of 0.2x. Its cash flow generation, however, remains solid, with the recently released 2015 production and cost guidance suggesting its free cash flow yield will be 25% in 2015 and 17% this year - making it one of the most attractive investments in the junior gold space.

Source : GS

(20min delay)

(20min delay)