Medusa Mining's December Quarterly Result Is (Yet) Another Step On The Road To Recovery

Jan. 30, 2015 12:23 PM ET Summary

Since taking over mid last year, Medusa Mining's new senior management has continued to deliver and rebuild investor confidence.

This month, Medusa has released a flurry of positive news, culminating in yesterday's release of its December quarterly result which exceeded production expectations due to higher grades and recoveries.

This follows the successful completion of the L8 Shaft upgrade and the announcement of a new, potentially large exploration target at Guinhalinan.

Although still at an early stage, the new Guinhalinan prospect is potentially comparable to the 1.14 moz Bananghilig Project to the north.

The continuing trend of positive news and outperformance since the new management team took over last year continues to push the company along the road to recovery.

Backgroundand Recap

Medusa Mining (OTCPK:MDSMF) is an ASX listed junior gold miner with mining operations based on the Philippine island of Mindanao. Last fiscal year (to 30 June 2014) it produced 60 koz of gold at an average C1 cost of US$418/oz and head grade of 4.76 g/t.

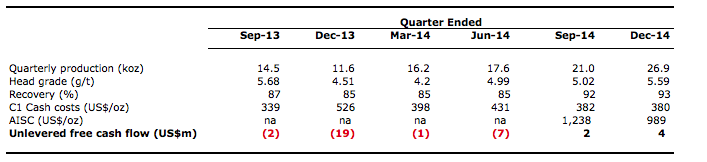

For the year to 30 June 2015, management has forecast production of 95 - 100 koz at an average C1 cash cost of US$400 - US$450/oz and All In Sustaining Cost (AISC) of $900 - $1,000/oz and with grades over 5%. Results for the second quarter (to 31 December 2014) continue to be encouraging - 27 koz at C1 cash costs of US$380/oz, AISC of US$989/oz and head grade 5.6g/t and take first half year production to 48koz. At 48koz, first half production exceeded earlier guidance of 40 - 45koz for the half.

Last November, I published a note on Medusa which argued the company was, following a long period of profound disappointment, back on the road to recovery and was poised to rerate. I suggested that the recent history of disappointing performance and missed management forecasts was coming to an end with the return of the company's founder (Geoff Davis) to the CEO position - drawing a line under the previous management of the company. You can find the article here. Back then the share price was A49c/share.

One of the things I particularly liked about the new management team and approach was its commitment to meeting its stated guidance and forecasts. It rightly saw this as fundamental in rebuilding confidence with the investment community which had too often been let down by the previous team. Since taking over last year, the new CEO has delivered on a number of fronts:

Kicked off a comprehensive review of the company's operations in order to optimize the Co-O mine's long-term mine planning. This culminated in the company releasing 2015 production guidance of 95 - 100koz, which was greater than many expected

Completed the restatement of the company's reserves to the latest JORC standard - delivering a better result than many expected (or rather a less worse result)

Completed the L8 shaft upgrade on time, which is key to the company's efforts to lift monthly mine production from 45kt to 60kt; bringing it closer to the mill's capacity

Restored the company to positive cash flow generation in both the September and December quarters

Further, the company looks set to continue to improve over the next six months with comments by the CEO at the November AGM meeting suggesting that the company's AISC for the full year to June 2015 could come in below its current guidance of US$900-US$1,000/oz; getting down to US$800-US$900/oz over the next 6 months as its efficiency program begins to bear fruit.

As you'd expect, with the continued progress towards rebuilding the company has gradually restored confidence in the company and, as a result, since my last note in November, MML's share price has outperformed many of its peers and the wider junior gold index, having risen 50%. (click to enlarge)

Source : Googlefinance Two Positive quarters in a row ... both cash flow positive.

MML's December quarter was the second successive quarter of cash flow profitability; delivering again on one of the key pledges of the new management team - to restore MML to cash flow profitability.

MML improved on its September results, which was itself a big improvement on early quarters. Importantly, the improvement was across nearly all metrics.

Production for the first half of 2015 was 48koz, which was significantly above management's guidance back in November of 40 - 45koz. Given this, I would expect MML to exceed its full year production guidance of 95 - 100koz for the year to June 2015 as the mine capacity has now been increased from around 45kt/month to 60kt/month, with the successful upgrade of the L8 Shaft.

Further, its likely MML will also beat its full year ASIC guidance of $900/oz - $1,000/oz. During the AGM in November, the CEO mentioned that he believed ASIC from that time onwards would be closer to $800/oz - $900/oz on account of efficiency programs that the company had put in place. If that is the case, it will bring ASIC comfortably below guidance for the whole year. (click to enlarge)

Source : Author Guinhalinan ... Potentially another Bananghilig

In the September quarterly result, MML mentioned that it was undertaking an extensive soil geochemical survey and mapping exercise on the Guinhalinan prospect, to the south of 1.14moz Bananghilig Deposit.

Source : Medusa Mining

This week, MML provided an update of its analysis of Guinhalinan, which suggests the presence of a regionally significant, consistent and extensive corridor of "gold in soil" anomalies approximately 5 km long (open to the south) and up to 2 km wide. Within this corridor there appears to be two distinct sub-parallel sub-corridors of gold in soil anomalism representing at least two separate zones of gold mineralisation.

Although things are still at an early stage for Guinhalinan, MML's CEO has described it as : " a major regionally significant exploration target with potential to rival the 'open in all directions' 1.14 million ounce Bananghilig mineralised system immediately to the north." If this does indeed turn out to be another Bananghilig, adding another 1.14moz to MML's resources, it would have the potential to significantly add to MML's mine life, which, currently at around 5 years on a reserve basis, continues to be one of the chief concerns amongst some investors.

On the topic of mine life, however, I think it is important to note that whilst MML's reserve life is about 4-5 years, the company has been successful over the past 7 years in replacing the resources at its Coo that is mines every year. Further, as the existing resource at Coo remains open in ALL directions, there is no reason to believe it will come to an end any time soon. Remember, the mine has been operating since the late 1980s.

Importantly, giving some further comfort regarding the bona fide of Guinhalinan, is the fact that, although still described as "gold in soil anomolies" uncovered as part of an extensive geochemical survey covering some 1200 samples, the company has done some drilling back in 2011, so there is high confidence that there is mineralisation there.

The next step in defining the size of the new discovery will be a full exploration program of further drilling, which the company is saying they will likely kick off in April this year. L8 Shaft upgrade complete ... Which should drive a significant production expansion and cost decline over the next few months

MML successfully completed its long planned upgrade of its L8 Shaft on time earlier this month. This involved both an increase in the haulage tonnage by replacing the existing 3.6t skip with a 4.8t skip as well as replacement of the single cage configuration with a double cage one. The net effect of the change is an increase in the mine production from the previous 45kt/month to 60kt/month and thus much closer to the new mill's capacity. Changing to a double cage configuration means that the change over time between shifts is much lower, further increasing the mine's efficiency. A compelling valuation ... notwithstanding the 50% re rating since November

So what does all this translate to in terms of valuation? Well, on a range of valuation metrics, MML looks cheap relative to its peers - no doubt. It trades below the average on an EV/resources at about US$50/oz, compared to the current gold sector average of circa $90/oz - $100/oz.

On an EV/EBITDA basis, which is closer to a simple cash flow valuation than EV/resources multiple, it is well below average. In fact, compared to where it was trading last November at the time of my last article on MML, it still trades at much the some discount to the peer group now as it did back then. I find this surprising because comparing the business now to back then, I see a business that has a substantially lower risk profile and a lot of positive momentum behind it.

If I had to suggest a reason for MML's discount to its peers, it might be perhaps because of the perceived short reserve life the MML has; frequently cited by some investors as a key concern. However, I would suggest that this is really a non issue as for the last 7 years, MML has successfully replaced the resources it has depleted through mining via exploration success and further drilling of the ore body. Given the ore body remains open in all directions right now, there is reason to believe that MML will continue well beyond the current reserve life of 4-5 years. (click to enlarge)

Source : Author, UBS

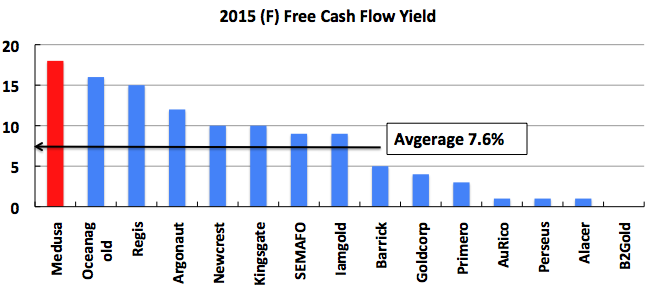

Anyone who reads my articles will know that I'm always hammering on about cash flow and what price an investor is paying for it. When it comes to investing, this is really the only thing that matters. Cash is king, especially in this environment of enhanced commodity price risk and volatility. Thus, One of the purest measures of value as far as I'm concerned is cash flow yield. Again, MML is a leader here. (click to enlarge)

Source : Author, UBS Conclusion

MML's release of its December quarterly result yesterday was demonstration of a company well on the path to recovery. MML's production was significantly above guidance and, together with the September quarterly result, becomes the second quarter in row that the company has remained cash flow positive.

Further, the December result comes after a number of other positive developments this month; the successful completion of the L8 Shaft upgrade and the discovery of a potentially major new exploration target with the Guinhalinan Project.

Notwithstanding the recent positive developments and the substantially lower risk profile investors in MML face today vis a vis 3 months ago, MML still trades at a substantial discount to its peers. Not as great as it was 3 months ago (owing to MML's 50% share price increase since November)

MML Price at posting:

82.5¢ Sentiment: Buy Disclosure: Held

(20min delay)

(20min delay)