http://seekingalpha.com/article/2968076-sunshine-heart-there-is-a-silver-lining-to-those-clouds

Sunshine Heart: There Is A Silver Lining To Those Clouds

Mar. 4, 2015 7:00 AM ET | About: Sunshine Heart, Inc. (SSH), Includes: HTWR, THOR

Disclosure: The author is long SSH. (More...)

Summary

- Some might think of the slow start to the Pivotal trial for Sunshine Heart’s C-Pulse heart assist device as clouds marring the outlook. Nothing could be further from the truth.

- The degree of success in clinical trials is heavily influenced by adequate preparedness and optimal patient selection criteria, supported by thorough training of all involved in recruitment.

- The silver lining to the clouds of a slow start is the potential to achieve success in the Pivotal trial far beyond that for the highly successful Feasibility study.

- Optimal results will increase the certainty of early PMA approval flowing from the recently approved interim analysis.

- If this sometimes looks like a tortoise and hare race, remember the tortoise won. For those with patience, the prize for winning this race is potentially in the $billions.

Article series

This article is a continuation of my series of articles developing a long term investment strategy based on an area of unmet need in the health sector, viz., enduring and effective therapies for late stage heart failure (see here, here, here and here)

The significant players are Thoratec (NASDAQ:THOR) and Heartware (NASDAQ:HTWR) with their LVADs, and Sunshine Heart (NASDAQ:SSH) with its C-Pulse. This article is the first in a multi-part sub-set about the Sunshine Heart C-Pulse heart assist system and the compelling long term investment opportunity it represents.

About the Sunshine Heart C-Pulse System

The C-Pulse system is the only prolonged use mechanical circulatory support system (NYSE:MCS) to successfully complete an FDA sanctioned feasibility and safety trial, for implantation in NYHA Class III and ambulatory Class IV late stage heart failure patients.

The C-Pulse system is currently in an FDA approved Pivotal trial with the aim of achieving PMA approval leading to commercialization in the US.

The C-Pulse System's design is based on proven balloon counter-pulsation technology to assist the heart by reducing the workload of the left ventricle.

During inflation of the balloon, blood flow is increased to the coronary arteries, thereby providing additional oxygen which is vital to a failing heart.

During deflation, the workload or pumping required by the left heart is reduced, resulting in more blood from the heart, called increased cardiac output (see here and here).

The C-Pulse technology utilizes this long proven counter-pulsation therapy applied in a different, innovative, and far safer methodology outside the blood stream.

In C-Pulse's 20 patient feasibility trial, 60% of these NYHA Class III and ambulatory Class IV advanced HF patients improved by at least one NYHA Class (a very significant improvement in quality of life) and 25% of the 20 patient cohort have become asymptomatic for Heart Failure (NYSE:HF) and have been weaned off the device. This result is unheard of with drug therapy where generally the best that can be expected is a slowing in the worsening of the condition.

The target market is estimated at 5.2 million advanced HF patients in the US and EU. Only a tiny percentage of these patients have to be implanted to achieve multi-billion dollar revenues.

The importance of Patient selection

HeartWare CEO, Douglas Godshall, on patient selection, in HTWR's 3rd quarter earnings conference call,

But when they pick the wrong patients, it becomes a huge burden on them and makes it much harder for them to manage the system. So they are improving their patient selection process, not treating all comers.

From the webcast of Sunshine Heart's 2nd quarter earnings conference call (précis in parts) -

Dave Rosa related the advice to him at the start of the Pivotal trial from a large investor who has heavy positions in both HeartWare and Thoratec -

Dave you're going to get pressured to get this trial done, and companies in the past have folded in to that pressure, and taken patients that really should not have been taken to increase enrollment. And then you get to the end of the trial and the trial comes out negative. No matter what people tell you, make sure you're getting the right patients for this therapy, because I think there is a place for it.

Mr Rosa indicated he agreed with that and the company is not in the business to take a number of deviations just to show they can enroll patients, and is being very strict about that.

Jason Mills - Canaccord Genuity

That's helpful. Obviously you're taking some lessons from the LVAD trials who have increasingly focused on patient selection and that's really helped the outcome, so that makes a lot of sense Dave.

Slow enrollments in the C-Pulse I (PIL model) Pivotal trial (the "clouds")

It should be no surprise that enrollments for the 388 patient Pivotal trial were slow to take off. A large part of the slowness has been due to the incredible amount of effort that went into preparation to ensure the success of the trial.

SSH Management delayed the start of the current trial until they made multiple improvements to the device, including lengthening the PIL to reduce exit site infections. It was then necessary to go through the process of having the FDA approve these upgrades which was achieved in Q3, 2013. One outcome, since the upgrades, is exit site infections in the EU Options HF trial have been reduced by ~80% compared to the US Feasibility trial.

A huge amount of work has also been put into patient selection criteria, including briefing for over 40 Cardiologists in Q1, 2014.

This has laid the groundwork for enhanced results in the Pivotal trial, even better than the excellent efficacy and safety results in the Feasibility trial.

Improved patient selection in the Pivotal trial (the "silver lining")

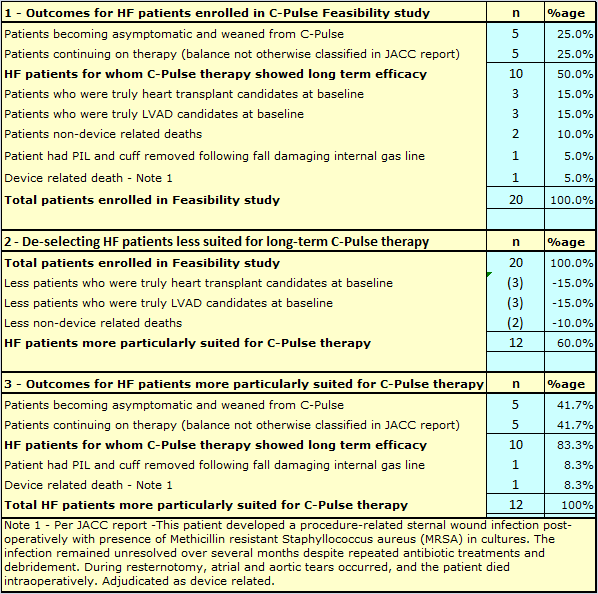

For the Sunshine Heart C-Pulse 20 patient Feasibility trial, there can be no doubt the pressure to complete enrollments caused at times a relaxation of enrollment criteria by enrolling Physicians. This extract from the JACC reported Feasibility trial results,

Some patients included in the study were in late-stage heart failure disease. While it was our intent to treat patients who were not candidates for LVAD or transplant, some of these patients were evaluated for transplant at baseline.

In the final analysis, six (6) of the patients enrolled in the trial, and initially implanted with C-Pulse, were effectively bridged to either heart transplant or LVAD implant.

That is not a bad outcome for those patients. But what if strict enrollment criteria had been adhered to and these particular patients had been excluded from the study?

The same question could be asked about the two patients who died after just 60 days and 61 days respectively from other than heart failure related causes. Could they have been identified at the time of enrollment as high risk of death from causes other than heart failure, and excluded from the study?

Table 1 below, shows a recalculation of the Feasibility trial results, after excluding those patients who were not truly candidates for long term C-Pulse therapy.

TABLE 1

The extreme importance of patient selection is demonstrated in Table 1 above.

It is acknowledged that some hindsight is used in making the adjustments, but as per the above Feasibility report extract, if not all, at least some of those patients were determined at baseline to be not suitable for long term C-Pulse therapy, but were selected and enrolled anyway.

If patient selection could be honed to perfection, the results in the Pivotal trial could be potentially lifted from 50% success to over 80% success for patients having the progression of their heart failure halted or reversed, or becoming asymptomatic for HF.

This is not to say that C-Pulse is inappropriate for bridging patients to Heart transplant or LVAD therapy.

There is a great advantage for HF patients to be bridged to heart transplant with the C-Pulse in preference to an LVAD.

LVAD implantation involves blood transfusions both in the implant procedure and to manage post-operative bleeding complications brought on by LVADs.

Blood transfusions increase antibodies in the blood stream. One of the most serious issues for heart transplant is the development of antibodies causing rejection of the transplanted heart. The already existing heightened levels of antibodies from blood transfusions prior to heart transplant increases the risk of rejection.

The option of a C-Pulse could also allow a potential heart transplant or LVAD patient to delay implantation of an LVAD with all of its attendant risks. With the uncertainty of availability of hearts for transplant this will likely prove a valuable option for advanced HF patients. But Pivotal trial results are likely to benefit from exclusion of such patients from the trial, to the extent possible.

Nevertheless, we have one documented example of a very excellent result for a heart transplant candidate enrolled in the C-Pulse Feasibility trial, as discussed below.

Case study involving a heart transplant candidate enrolled in the C-Pulse Feasibility trial

The conclusions of this case study were,

Long-term implantation of an extra-aortic counterpulsation device provided substantial hemodynamics and symptoms improvement in a Class III heart failure patient and does not appear to significantly alter the aortic wall structures.

The clinical assessments of this heart transplant candidate, before and after C-Pulse implant, are described as follows -

A 58-year-old female presented with shortness of breath, orthopnea, paroxysmal nocturnal dyspnea, and an ejection fraction of 15% (NYHA class III). She was diagnosed with non-ischemic cardiomyopathy and treated with medical management and a dual chamber pacemaker. Her condition did not improve despite optimal medical therapy and she was listed for heart transplant.

A C-Pulse Heart Assist System was implanted 7 months after her first diagnosis as a bridge-to-transplant.

One month after implantation, her symptoms improved from NYHA class III to class I and her cardiac output increased from 3.5 to 5.5 L/min. Echocardiography showed a decrease of her baseline mitral regurgitation from moderate to mild. Her MLWHF questionnaire score decreased from 77 to 13. At 12 months, her 6MWT had increased from 305m at baseline to 457m.

Her later course was complicated by persistent S. aureus driveline infection. She was upgraded to UNOS status 1A and received a heart transplant 21 months post device implantation.

But for the driveline infection, who knows how long this patient might have been supported by C-Pulse beyond the 21 months indicated. Of course, subsequent improvements to the C-Pulse system have reduced driveline infections by ~80%, and the proposed fully implantable model will eliminate the percutaneous driveline and associated infection risks.

This particular case study, of what is probably a Class IIIB HF patient eligible for transplant, must be of enormous concern to Thoratec and HeartWare. But for the availability of C-Pulse, this patient would have almost certainly had an LVAD implanted.

If C-Pulse can be effective in a subset of Class IIIB patients eligible for transplant, then the absence of the horrific potential adverse events, the minimally invasive operation, and the shorter operation time and hospital duration, compared to an LVAD, will almost certainly drive such patients to C-Pulse.

The importance of patient selection to the proposed Interim Analysis

In the Sunshine Heart 2nd quarter conference call, Kimberley Olesen, Senior Vice President, Clinical Affairs, explained the Interim analysis process.

Should interim analysis be agreed by the FDA, there would be a requirement to be able to demonstrate efficacy at an adjusted very aggressive pre-set performance level set at a very low P value.

The results to date at the interim analysis point would be reviewed by the Data Safety Monitoring Board (DSMB) with three possible outcomes.

Firstly, the trial could be stopped early if results at interim analysis indicated a low chance of success.

Secondly, if results at interim analysis were satisfactory but not up to the pre-set aggressive performance level, the trial would be allowed to continue to completion with efficacy judged at the original performance level.

Thirdly, if the pre-set aggressive performance level were met, there could be a request to stop the trial or to modify the trial design.

That would not mean an automatic move to PMA, but discussions and negotiations could then take place with the FDA towards that end.

As has been shown in Table 1 above, patient selection is influential in being able to demonstrate efficacy at a very aggressive pre-set performance level.

There is a distinct trade off between slower patient enrollment due to strict enforcement of patient selection criteria, and the possibility of halving the numbers of enrollments required through success at an interim analysis.

Such a strategy not only potentially shortens the time to PMA but also gives the possibility of outstanding trial results.

Outstanding trial results would in turn be expected to accelerate the commercialization phase.

There will be a need for a capital raise

A couple of truisms in the world of investment are -

In respect of 1 above, SSH have added some very highly credentialed members to their Management team over the last twelve months as follows -

- The three most important things to look for in a company are Management, Management, and Management; and

- The best time to raise additional capital is when you do not need it.

Claudia Drayton is likely to have been instrumental in securing the recently announced growth capital loan for up to $10M.

- Kimberly Olesen, formerly Vice President of Global Clinical Operations at Medtronic ;

- Brian Brown, formerly R & D, Vice President Cardiovascular at Boston Scientific for the past 10 years.

- Claudia Drayton, formerly Chief Financial Officer and Senior Finance Director for Medtronic Inc.'s Integrated Health Solutions Business

The condition for the drawdown of the final tranche of that loan is for SSH to achieve 100 enrollments in the C-Pulse Pivotal trial by September 30, 2015.

Obviously, SSH believe 100 enrollments are achievable by 30 September or earlier, perhaps by August.

Achievement of 100 enrollments will take C-Pulse past the half way point for the interim analysis.

With additional sites being progressively activated, and increasing enrollment rates per site, I believe investors will see the end in sight once that magic figure of 100 enrollments is achieved.

And that would be a fortuitous time to raise additional capital.

Table 2 below projects what the cash position of the company might have been without the growth capital loan.

TABLE 2

The clear and imminent need for cash at end of 3rd quarter 2015 would have been, for investors, like blood in the water to sharks. This is particularly so, leading into the Christmas holiday period.

This would likely have depressed the price at which capital could be raised despite the enrollment achievements.

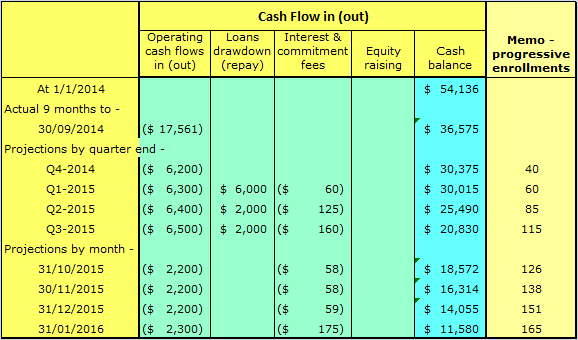

Table 3 below shows the cash situation with the growth capital loan factored in.

TABLE 3

It can be seen from Table 3, the growth capital loan has completely changed the picture.

Should SSH initiate a capital round in September 2015, on the back of good enrollment figures, it will still have at that stage cash reserves sufficient for the next nine (9) months.

SSH will be seen to be raising capital at a time when it does not have an urgent need to raise capital.

This was the case for the last major round back in September 2013, with 4.38M shares issued at a price of $10.50 per share.

Immediately before that 2013 capital round, SSH had ~$16.8M in cash, sufficient for the next 8 to 9 months. So the cash position at 30 September 2015 is likely to be better than at the time of the highly successful September 2013 capital round.

Conclusions and what is ahead

The silver lining to the clouds of a slow start is the potential to achieve success in the Pivotal trial far beyond that for the highly successful Feasibility study.

If this sometimes looks like a tortoise and hare race, remember the tortoise won. The conduct of this trial might come, in time, to be considered a textbook example of how to conduct a trial of this nature.

For those with patience, the prize for winning this race is potentially in the $billions (see this article's Tables 1 and 2).

Quite apart from any projections I might make, Analysts 12 month price target range for SSH is $9 to $16, with consensus price of $13.50.

That is a range of around 2 to 3 times the current share price, for a company with a device addressing a market over 20 times larger than the market shared by THOR and HTWR.

Conversely, the combined market caps for THOR and HTWR total $3.6Bn, over 36 times greater than the less than $100M market cap for SSH.

With continuing improvement in enrollment rates, and announcements on progress with the fully implantable model, I do not see why the pricing of a capital round in September 2015 would be less than the consensus price shown above, and possibly much higher.

I believe the evidence to date shows a level of efficacy for C-Pulse far beyond what any necessarily conservative medical professional could express, because of the limited number of implants.

Drugs undergoing trials are subject to unknown side effects and the impact on patients with differing genomic and phenomic attributes cannot be identified without very large trials.

But C-Pulse is not a drug.

C-Pulse is a medical device, applying a therapy, counter-pulsation, successfully used for decades. The limitation for intra-aortic Balloon counter-pulsation has been the short time (measured in hours) the therapy can be applied, because it has the same blood contacting curse as the LVADs from THOR and HTWR.

C-Pulse, being outside the bloodstream, does not have those complications, and can therefore be used for prolonged periods, allowing its convalescent effect on the heart to be fully effective.

In my next article, I will seek to demonstrate how we can make some educated judgments on the likely outcomes of C-Pulse versus optimal medical therapy. This should give some pointers, some color, to how C-Pulse might perform at the Interim Analysis for the FDA approved Pivotal trial.

Caution: The information above is not intended to replace the advice of a doctor. I disclaim any liability for any decisions you might make based on this information.

Additional caution: As always, please do your own research before any buy or sell decisions. Use of information and research in the article above is at your own risk.

The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stock/s mentioned. Past performance of the company/s discussed may not continue and the company/s may not achieve any projected earnings or dividend growth. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. I do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for their specific situation.

Investing in micro cap companies is not suitable for all investors, and can be risky. It's important that investors thoroughly perform their own due diligence and analyze the potential risks. Due to illiquidity, share prices can fall despite strong fundamentals and possible inability to raise sufficient additional cash to continue to fund ongoing operations is always a serious concern. Fuller details of risks associated with Sunshine Heart as identified by the company may be found with their form 10-12B/A registration filing with the SEC and their other SEC filings.

Editor's Note: This article covers one or more stocks trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks.

Add to My Watchlist

What is My Watchlist?