An objective inquiry into value

The following lines of evidence aim to uncover and appreciate the value of the FTO inhibitor Bisantrene from an objective, exploratory, and curious perspective. I state that this is strictly not intended as financial advice and that the values I purpose are highly speculative. My understanding of oncology and particularly the FTO inhibitory space forms the foundation of my valuation. I encourage you to do your own research and form your own opinions of how to value an FTO inhibitor and what that value might look like and share it in this thread.

Brief summary of available data

Bisantrene is the most potent, clinically mature FTO inhibitor with historic efficacy in AML and Breast cancer, with the potential to be a first-in-class therapy for diseases that overexpress FTO. Historic safety and efficacy data reduces clinical risk. Since there is no currently approved compound for the inhibition of FTO and Bisantrene is more potent and clinically mature than other FTO inhibitory compounds, there is reduced commercial risk. Based on available data demonstrating the link between FTO and disease and therapy synergy, there is large potential value for Bisantrene.

Peer comparison

I have compared M&A transactions for non-FDA and FDA approved compounds to more clearly determine value for Bisantrene. Importantly, data generated in these tables were at or as close to the specific time of M&A transactions for each drug, particularly the safety and efficacy data. There may be new data that relates to each of the drugs (which in some cases I have had to include), but this does not enter into my analysis as it was not known at the time of purchase. I have included the M&A transactions of Juno Therapeutics (JCAR-017), Loxo Therapeutics (LOXO-292), Forty Seven (Magrolimab), and Immunomedics (Todelvy) to determine a potential value for Bisantrene. By comparing and contrasting the clinical maturity, therapy synergies, cancer indications, first-in-class or best-in-class status, and pipeline potential of the JCAR-017, LOXO-292, Magrolimab, and Todelvy buyouts, the evidence suggests that Bisantrene is highly competitive anti-cancer agent that could drive a multi-billion dollar deal.

Clinically maturity

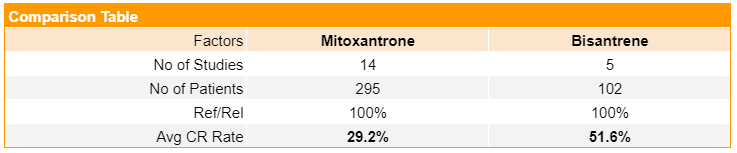

In comparison to phase I (JCAR-017 and Magrolimab) and phase I/II (LOXO-292) assets, Bisantrene has substantially more clinical data supporting its efficacy and safety in humans. This is evidenced by the 40 in-human clinical trials, established efficacy and cardiac safety profile, and approval for use in AML. Despite historic preclinical studies suggesting that it bound to topoisomerase II poorly and slowly, Bisantrene (52%) average complete response is rate greater than the FDA approved anthracenes doxorubicin (36%) (1), idarubicin (20%) (2), and mitoxantrone (29%) (3). The table below compares phase II single agent studies average complete response rates for Bisantrene and mitoxantrone. By comparison, Bisantrene achieves a response rate in ~22% more patients and as such, is ~1.8 times more potent. Importantly, the dose and regimen utilized in historic AML trials supports Bisantrene as an FTO inhibitor, which may explain the strong effects seen in humans.

More specifically, the doses of Bisantrene used in these trials were much greater than the dose theorized for an FTO inhibitor (7.5 mg/m2/d). Data from a historic phase I dose escalation study suggests that consistent low-dose Bisantrene is very safe up to 50 mg/m2/d - there were only two reported toxicities (10%) in twenty evaluable patients (below). As the dose increases beyond 50 mg/m2/d, there are more reports of toxicity. The five phase II R/R AML trials that used 250 mg/m2/d for 7 consecutive days with 3 day follow up in 95 total AML patients demonstrated that Bisantrene is safe and tolerable, which provides good evidence that lower-dose Bisantrene (<50 mg/m2/d) over consecutive days will be safe.

Both Bisantrene and Todelvy are phase III assets and have generated enough efficacy data to drive approval for a cancer indication, with Bisantrene having no current FDA approval. While Todelvy has largely focused on TNBC (ORR 35%, CR 4%) and metastatic urothelial cancer (mUC) (ORR 27%, CR 6%), Bisantrene was focused on variable breast cancer (ORR 19.2%) and AML (CR 52%). In 2019, there were a number of clinical programs underway for Todelvy, which were mostly in TNBC and mUC (below; 4). In comparison, Bisantrene has safety, tolerability, and efficacy data in >40 in-human clinical trials. Hence, it appears that Bisantrene and Todelvy are at least comparable in terms of clinical maturity, with Trodelvy being more valuable with a current FDA approval.

1 https://www.pfizer.com.au/sites/pfizer.com.au/files/g10005016/f/201311/PI_Adriamycin_212.pdf

2 https://pubmed.ncbi.nlm.nih.gov/2192943/

3 https://pubmed.ncbi.nlm.nih.gov/9352324/

4 https://www.annualreports.com/HostedData/AnnualReports/PDF/NASDAQ_IMMU_2019.pdf

Anti-cancer therapy synergies

There are more current and potential anti-cancer therapy synergies known for Bisantrene and an FTO inhibitor than comparable drugs prior to M&A transaction. There is in-human data demonstrating Bisantrene synergizes with the FDA approved compound cytarabine (Ara-C) and preclinical data showing synergy with nucleoside analogs, a hypomethylating agent, and a Bcl-2 inhibitor. While limited synergistic opportunities were available for JCAR-017 and LOXO-292, the synergies ascribed to Magrolimab are taken from the clinical trials website and may not have been known at the time of the transaction. In-human data suggests that magrolimab synergises well with Azacitidine. However, as a single agent, azacitidine demonstrated a 49% ORR in MDS patients (12% CR; 25% PR; 12% hematological improvement), which may have influenced the response rate seen in the phase 1b combination trial (1). Also, a phase I/II study of Magrolimab in combination with an EGFR inhibitor for colorectal cancer released just prior to purchase indicates that it has relatively poor efficacy with a 6.7% ORR (2). These data question the efficacy of Magrolimab as a single agent, and strengthen the relative value of Bisantrene.

Todelvy is an antibody-drug conjugate, which means it’s a two for one: 1) trop-2 antibody; and 2) topoisomerase II inhibitor (SN-38). Interestingly, Bisantrene also has a dual mechanism of action, where it potently binds to FTO as well as topoisomerase II in high enough concentrations over enough time. This dual action may explain the high CR rates in AML patients where the dose was great enough to completely inhibit FTO, while allowing a concentration of Bisantrene to act on topoisomerase II. Although, without clear in-human data, this remains a speculative point.

There were 5 potential synergies known for Todelvy prior to the transaction. Todelvy had preclinical data demonstrating synergy with PARP inhibitors and microtubule inhibitors as well as an ABCG2 inhibitor (3-4). There was a phase I/II TNBC trial underway for a combination with anti-PD1 therapies at buyout, and results from a phase I/II trial in combination with a PARP inhibitor suggests that toxicities may make the combination not an effective treatment option (5-6).

There are currently 10 potential synergies known for Bisantrene. Bisantrene was shown to safely and effectively synergise with Ara-C in a heavily pretreated, poor prognosis R/R AML paediatric population achieving a CR of 46% (7). The City of Hope demonstrated that Bisantrene synergised with hypomethylating agents in vivo (8), while the MD Anderson centre confirmed the synergistic effects of Bisantrene with nucleoside analogues and Bcl-2 inhibitors in vitro (9). In comparison to Todelvy, Bisantrene has more established synergies both in human and preclinical, as well as more theorised synergies that have been determined through preclinical FTO knockdown/inhibition models. It is not yet known how many synergies may be possible for Todelvy or Bisantrene.

1 https://www.ncbi.nlm.nih.gov/pmc/articles/PMC3627328/

2 https://ascopubs.org/doi/abs/10.1200/JCO.2020.38.4_suppl.114

3 https://www.globenewswire.com/news-release/2015/11/09/785105/10155584/en/Immunomedics-Announces-Sacituzumab-Govitecan-Is-Synergistic-With-Chemotherapeutics-That-Target-Cell-Division-in-Triple-Negative-Breast-Cancer.html?culture=en-us4 https://pubmed.ncbi.nlm.nih.gov/27207776/

5 https://www.preprints.org/manuscript/202012.0062/v1

7 https://pubmed.ncbi.nlm.nih.gov/8259097/

8 https://www.cell.com/cancer-cell/pdfExtended/S1535-6108(20)30216-6

Cancer indications

It’s clear that when compared to JCAR-017, LOXO-292, and Magrolimab, Bisantrene has substantially more cancer indications. Briefly, CAR-T therapy is currently applicable to blood cancers only, and RET inhibitors (LOXO-292) are effective in 2% of lung and 30% of thyroid cancer patients (~5000 patients). Magrolimab has a larger range of cancer indications than the prior two drugs, although more research is needed before strong conclusions can be made about indications for Magrolimab.

The 13 cancer indications linked to Todelvy were known prior to the transaction. By comparison, overexpression of the FTO protein is currently linked to 19 different cancer types. Based on this data, Bisantrene has the potential to be used in a larger number of cancer types than Todelvy. While not known at the time of transaction, a basket phase I/II trial for Todelvy demonstrated 15-30% partial responses in 6 of 17 different cancer types (1). As an FTO inhibitor, Bisantrene has established efficacy in 5 different cancer types in preclinical models. A major limitation of the historic clinical data for Bisantrene is that dose and dosing regimen as well as therapy combinations were not optimized for an FTO inhibitor and thus, it is difficult to accurately determine the number of cancer indications where Bisantrene may be effective. Based on the evidence available, Bisantrene has more cancer indications than all other previous M&A compounds, which implies that it has greater market potential.

1 https://www.sciencedirect.com/science/article/pii/S0923753421008838

First-in-class / best-in-class

Aside from JCAR-017, the transactions I have listed are for first-in-class drugs. What is important to note from the table is pharmaceutical companies are prepared to pay multi-billions for a drug that is first and that demonstrates strong efficacy. A review paper has compared the advantages of first-in-class drugs to best-in-class drugs, and found that on average, it pays to be first (1). A key point worth consideration is that the paper discusses how the risks of being first include the drug not being efficacious in humans, which is a major point of difference and value driver for Bisantrene when compared to other phase 1 (or 1/2) assets (JCAR-017, LOXO-292, and Magrolimab). The historic clinical efficacy data in AML, where the dose and dosing regimen would have supported its FTO inhibitory properties, provides very clear evidence that Bisantrene is effective in humans (below) and may, therefore, reduce the clinical risks associated with a first-in-class drug outlined in the paper. Additionally, the paper explains that if the second drug is not launched within two years, then the first drug will have substantially more market capture and thus, generate more relative revenue (1). Again, the established clinical maturity of Bisantrene reduces the risk of complications in FTO-directed clinical trials and increases the likelihood of fast approval relative to competitors.

Additionally, Bisantrene is at least 3-times more potent than the next most potent FTO inhibitor, which highlights it is also currently best-in-class (below). To put this into relative terms, you would need three times the dose of Bisantrene to confer the same effect, which opens up the possibility of side effects that may be unfavorable. Thus, these data highlight that Bisantrene is comparable to other first-in-class M&A transactions.

In summary, evidence clearly suggests that pharmaceutical companies are prepared to pay multi-billions for first-in-class products. Also, while Bisantrene has the potential to be a first-in-class FTO inhibitor, it also has substantial clinical maturity that decreases the risks associated with first-in-class purchases. In comparison to other known compounds, Bisantrene appears to be a more attractive first-in-class purchase.

1 https://www.nature.com/articles/nrd4035

Pipeline Comparison

The review paper that I discussed above highlights that an important additional factor to determining value is if the drug has a breadth of indications broadening its market (1). The example they use is Aripiprazole, an atypical antipsychotic, which was the sixth drug to market and would theoretically have trouble competing with established drugs, but because it has multiple approved indications in schizophrenia, bipolar disorder, depression, and irritability associated with autism, it has outsized market value relative to its competitors. Understanding this concept is key to understanding the point of difference for Bisantrene and RAC compared to other M&A transactions. All of the M&A transactions that I have listed are for therapies that only target cancer. While oncology is a very large and lucrative market, it restricts the potential for use relative to an FTO inhibitor. Of course, the buyouts for these drugs included other preclinical or clinical compounds, which will be discussed below.

The M&A transactions included in this analysis all contained additional compounds, with the majority being preclinical. It’s clear that in all cases the transaction was for the headline oncology drug. While Vitrakvi of Loxo Therapeutics was estimated to bring in USD $844 M in annual sales, LOXO-292 was estimated at USD $1 B peak sales at the time of the transaction (2). Clearly, though, Vitrakvi may have influenced the price paid in the acquisition of LOXO-292. Importantly, while not mentioned in the table above, Immunomedics controlled the patent to link that connected the trop-2 antibody to SN-38, which was included in the Gilead transaction of Todelvy (3). The linker technology was advanced for antibody drug conjugates and very valuable.

Currently, Bisantrene is the most potent and clinically mature FTO inhibitor available. FTO has been associated with a number of non-cancerous diseases including obesity, type 2 diabetes (T2D), non-alcoholic fatty liver disease (NAFLD), polycystic ovarian syndrome (PCOS), Alzheimer’s disease (AD), Parkinson’s disease (PD), addiction, and neuropathic pain. Currently, the estimated number of patients with these conditions is >4 billion and the global combined market value was estimated at USD $325 B in ~2019 and is expected to be worth USD $641 B by around 2026 (4). Currently, there are no FTO inhibitors approved for use in any of the diseases mentioned and of course, a compound that is approved for use would only access a percentage of that potential revenue.

Currently, RAC is undertaking a preclinical heart safety study to determine the mechanism of action that confers heart safety. Despite the historic efficacy in AML and breast cancer, Bisantrene has shown virtually no cardiac toxicity. Raw data from a phase II study investigating Bisantrene in AML patients and a phase III study in breast cancer patients highlights the lack of cardiac toxicity despite large cumulative doses of Bisantrene used (7080 mg/m2 and 5440 mg/m2, respectively). Recent FTO-directed data suggests that FTO inhibition increases a cellular mechanism known as autophagy, a cellular cleaning process, that may oppose the anthracene-induced cardiotoxicity implicated by anthracenes. Taken together, these data support the notion that Bisantrene may have been targeting FTO in non-cancerous cells in humans. If indeed Bisantrene is found to inhibit FTO in non-cancerous cells, then it would open up the potential to be a first-in-class therapy for metabolic disease indications.

A major consideration for pipeline potential is whether or not Bisantrene crosses the blood brain barrier (BBB) to influence the pathogenesis of neurological diseases. Bisantrene achieved a partial response in an EMD AML patient with CNS involvement (5), indicating that it may indeed pass the blood brain barrier. However, early partitioning studies in dogs and monkeys found very small traces of the compound in the brain (6). RAC is undertaking an EMD AML mouse model study that may include CNS involvement and may be an indicator of whether Bisantrene can cross the BBB. This study may utilize Bisantrene in combination with an advanced drug delivery technology to facilitate movement across the BBB. If Bisantrene can cross the BBB and influence the pathogenesis of neurological diseases, then it could open the potential to be a first-in-class therapy for neurological disease indications.

Like Trodelvy had secured patents to its linker technology, RAC may also have patents surrounding the measurement of FTO or intracellular methylation/demethylation. Companion diagnostic tests are essential tools for increasing the likelihood of efficacy for targeted or precision therapies (7). Securing patents for this technology would be very valuable for RAC in an M&A transaction situation.

Hence, in comparison to the M&A pipelines above, Bisantrene is extremely competitive. This is based upon the potential for Bisantrene to become a first-in-class therapy for metabolic and neurological diseases, and neuropathic pain, as well as other diseases that may come to light that are influenced greatly by overexpression of FTO.

1 https://www.nature.com/articles/nrd4035

2 https://www.reuters.com/article/us-bayer-loxo-vitrakvi-idUSKCN1Q41V7

3 https://www.annualreports.com/HostedData/AnnualReports/PDF/NASDAQ_IMMU_2019.pdf

4 https://hotcopper.com.au/threads/rac-primer.5627186/page-440?post_id=53654079

5 https://onlinelibrary.wiley.com/doi/abs/10.1111/ejh.13544

6 https://pubmed.ncbi.nlm.nih.gov/7083220/

7 https://www.fda.gov/medical-devices/in-vitro-diagnostics/companion-diagnostics

Limitations

I recognise my own limitations in evaluating scientific literature and biases. I have attempted to cite all of my work extensively to counteract my biases and personal limitations. However, there will be statements made that do not have citations, as I have extensively referenced the topic in other well-known and liked posts. The conclusions I draw are based on my own interpretation of the data and as new data comes to light, I may then change how I perceive the data and relationships observed in this peer comparison. I acknowledge the difficulties associated with finding and interpreting the data that would have been known to pharmaceutical companies just prior to a transaction, which may have influenced my interpretations of the data and the comparisons I have made. Also, I have assumed that Bisantrene was functioning mainly as an FTO inhibitor in all clinical trials, which as more data comes to light may prove to be wrong. I have provided an in-depth analysis of evidence supporting Bisantrene as an FTO inhibitor over an anthracene (1-2). Indeed, there may be better peer M&A transaction comparisons available, which would more accurately determine the value of Bisantrene.

1 https://hotcopper.com.au/threads/rac-primer.5627186/page-199?post_id=52881188

2 https://hotcopper.com.au/threads/rac-primer.5627186/page-238?post_id=52963436

Valuation

This estimation is based on a comparison of peer M&A transactions of first-in-class or best-in-class drugs within the last 3 years. Key points for evaluation were clinical maturity, anti-cancer therapy synergies, cancer indications, first-in-class or best-in-class status, and a pipeline comparison. The available evidence very clearly demonstrates that Bisantrene is superior clinically and has greater synergy potential, cancer indications, and pipeline potential than the buyouts of Juno Therapeutics, Loxo Therapeutics, and Forty Seven. Taking the average of the three buyouts provides a baseline value of AUD $9.4 B ($55.3 per share; 170M SOI) for Bisantrene.

The data above indicates that Bisantrene is comparable to Immunomedics antibody drug conjugate Todelvy, which was purchased for USD $21B in 2020. Bisantrene does not have current FDA approval, which decreases relative value compared to Todelvy. However, the available evidence suggests that Bisantrene is as clinically mature as Todelvy, and has greater potential therapy synergies, cancer indications, and pipeline potential than Todelvy prior to its purchase in 2020. The evidence suggests that an upper limit of value for Bisantrene may be approximately AUD $27 B ($160 per share; 170M SOI). However, due to the lack of data currently known for the true potential of Bisantrene, it is unknown whether the true value would be above or below this point. The FTO-directed clinical and preclinical programs underway for Bisantrene may help to elucidate the true value.

Future Work

To more accurately determine the value of Bisantrene, I encourage those evaluating my work to present a case where Bisantrene is worth less than the buyouts of Juno Therapeutics, Loxo Therapeutics, and Forty Seven. Hypothetical situations without current and critical evaluation of the evidence will not be considered substantial. Hopefully, this will fortify a baseline value for Bisantrene. Additionally, future work should evaluate the strengths and weaknesses in comparison to Todelvy, so that a top end value for Bisantrene can be more accurately determined. This work may focus on areas outside of those I have covered here or may review them and rewrite them from a fresh perspective.

Speculative M&A Transaction Analysis

Add RAC (ASX) to my watchlist

(20min delay) (20min delay)

|

|||||

|

Last

$1.41 |

Change

0.095(7.22%) |

Mkt cap ! $234.3M | |||

| Open | High | Low | Value | Volume |

| $1.32 | $1.41 | $1.32 | $249.8K | 182.9K |

Buyers (Bids)

| No. | Vol. | Price($) |

|---|---|---|

| 2 | 2826 | $1.40 |

Sellers (Offers)

| Price($) | Vol. | No. |

|---|---|---|

| $1.43 | 40000 | 1 |

View Market Depth

| Last trade - 16.10pm 10/05/2024 (20 minute delay) ? |

|

|||||

|

Last

$1.37 |

Change

0.095 ( 6.64 %) |

||||

| Open | High | Low | Volume | ||

| $1.34 | $1.41 | $1.32 | 16145 | ||

| Last updated 15.53pm 10/05/2024 ? | |||||

| RAC (ASX) Chart |