The stem cell sector is gaining momentum at a rapid pace ..MSB has done eleven years of the hard yards ,and has four times as many applications as any other reg.med. company ,not only that but we have more into ph3 than some have in thier portfolio..Someone mentioned some of our 13 or so apps. appear to be neglected, not so. Not one has been abounded they all fit the long term plan ,Imagine the cost of keeping them all at the front line ..My belief is that the priority is to lead with the most important taking into account financial return ,demand,etc. There is progress with back half and that will ramp up as soon as the first few become winners ..Regardless what happened over the last month we have a CEO inplace who cannot be replaced the man is so hands on ..Most large companies have ceo,s that can and do get replaced often ie. tls ,bhp, rio, etc ..SI has about 15 years stem cell exp.......................................... Here is a bit of whats happening in Reg. Med. ........................................Forgotten Stem Cell Sector Is Making Substantive Progress

Stem Cell Stocks Have Been Poor Performers for Years But Real Progress is Being Made.

Tigenix Meets Phase III Primary Endpoint in for Allogeneic Stem Cell Treatment for Fistula.

Mesoblast Therapy for Graft vs. Host Disease Gets Recommendation for Approval in Japan.

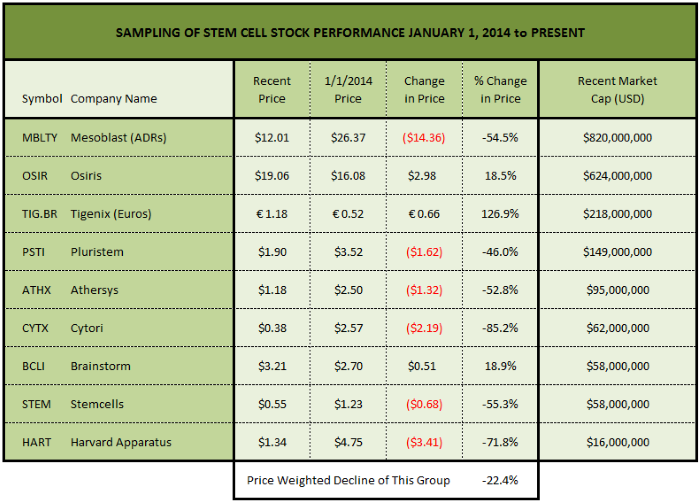

It's been a brutal couple of years for most stocks in the stem cell sector. Despite the mostly rosy forecasts from the mid tier investment banks over the last few years, most investors in this group have suffered big losses as the optimism over the pipeline potential of stem cell therapies has been met by the reality of extended timelines in conjunction with the endless need for capital. The chart below illustrates this reality: (click to enlarge)

Since January 1, 2014 this group of 9 companies in the sector has shown a cumulative price weighted loss of 22.4%. There is a story behind each of these companies but the purpose of this article is not to dig too deeply into any one company. Instead, it will focus on some recent positive industry developments and individual successes that may foretell a change in the fortunes of this sector.

Individual sectors in biotechnology sector tend to heat up as group, not only as a result of impressive data reported by one of its constituents but as a result of Wall Street analyst cheerleaders shaking their pompoms in the hope of bringing their company investment banking business. Recently, the hot sector in biotech has been CAR-T Cell Immunotherapy. Many companies in this sector have skyrocketed to multi-billion dollar valuations well before the revenue pipeline has been established. Juno Therapeutics (NASDAQ:JUNO) is a perfect example, reaching a market cap north of $6.8 billion with negligible revenues before falling back to its still hefty current market cap of $3.5 Billion. To Juno's credit it recently landed a lucrative 10 year agreement with Celgenethat helps validate its platform. Most other companies in this sector have also skyrocketed and have since fallen back. These valuations are indicative of the power of unbridled enthusiasm by investors in the "next big thing". Some of these companies may be winners while many will be losers but it will take a long period of execution to sort them all out.

The stem cell sector of biotech has been around for over a decade with the long held promise to have a major impact on the health care system. There have been a few recent achievements by two non-U.S. based companies in the stem cell sector that may be precursors of future success by other companies in the sector in an area of biotech that lost its mojo many years ago.

The first bit of encouraging news comes from Tigenix (OTC:TGXSF). Tigenix is a Belgium based stem cell company that most in the U.S. have never heard of. However, they have recently released significant news, not only for the company but for the entire stem cell sector: LEUVEN, Belgium, Aug. 23, 2015 (GLOBE NEWSWIRE) -- TiGenix NV (Euronext Brussels: TIG), an advanced biopharmaceutical company focused on developing and commercialising novel therapeutics from its proprietary platforms of allogeneic expanded stem cells, announced today that its lead compound Cx601 met the primary endpoint in the Phase III ADMIRE-CD trial in Crohn's disease patients with complex perianalfistulas. Cx601 is a suspension of allogeneic expanded adipose-derived stem cells (eASC) injected intra-lesionally. A single injection of Cx601 was statistically superior to placebo in achieving combined remission at week 24, in patients with inadequate response to previous therapies, including anti-TNFs. The study results confirm the favourable safety and tolerability profile of Cx601.

Meeting a primary endpoint on a Phase III is a value creator and the shares have recently rallied smartly as a result. This Seeking Alpha article provides an analysis of this important success for Tigenix. For the industry as a whole, it is clear evidence that adipose derived cells have a place as an effective therapy for this difficult to treat disease. If these stem cells work for fistula what else will they work for?

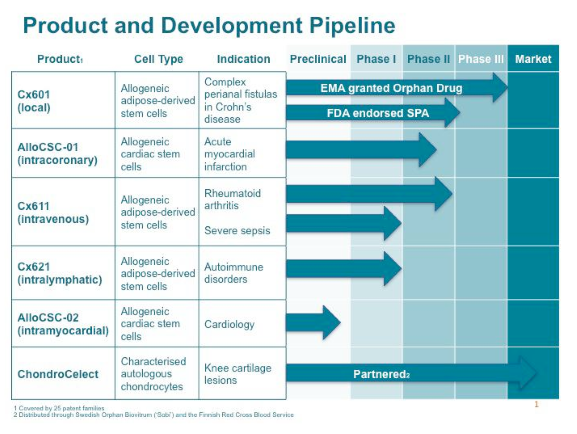

This is what the Tigenix pipeline looks like today:

Tigenix closed 2014 with about $15 million in cash at today's exchange rate and reports its financial statements semi-annually. It is scheduled to report interim results for the six months ended June 30, 2015 on September 15, 2015.

The next bit of exciting news for the sector comes out of Australia and Japan. Mesoblast (OTCPK:MBLTY), the 800lb Australian gorilla of the stem cell space by virtue of its 2010 agreement with Cephalon followed a year later by Teva Pharmacuetical's acquisition of Cephalon, also has had some encouraging recent news. The first bit was this press release regarding its Congestive Heart Failure Phase III trial:

We are particularly pleased with the outcome of the recent meeting between our development and commercialization partner Teva Pharmaceutical Industries Ltd (NYSE:TEVA) and the United States Food and Drug Administration (FDA) regarding our Phase 3 chronic heart failure program. The ongoing Phase 3 trial continues to recruit well and, as a result of the FDA meeting, has the potential for early completion based on overwhelming efficacy."

To explain this announcement in simple terms, the FDA has agreed to allow an interim analysis to be performed when 50% of the primary endpoints, Heart Failure-Major Adverse Cardiac Events (HF-MACE) have been achieved. When that certain pre-specified (not disclosed) number of events has occurred, the study stops and the data is analyzed. If these data are strong enough, and the threshold is met, the study will be stopped due to overwhelming efficacy. Asimilar scenario played out with Osiris (NASDAQ:OSIR) and its Grafix wound healing study in 2013.

There is also this recent news from Mesoblast regarding progress in Japan that represents an even shorter timeline to revenues: NEW YORK and MELBOURNE, Australia, Sept. 3, 2015 (GLOBE NEWSWIRE) -- Mesoblast Limited (ASX: MSB; USOTC: MBLTY) today announced that the allogeneic mesenchymal stem cell-based regenerative medicine product JR-031, developed by Mesoblast's Japanese partner JCR Pharmaceuticals Co. Ltd., was recommended for approval on 2 September at a meeting organized by the Committee on Regenerative Medicine Products and Biological Technology of Pharmaceutical Affairs and Food Sanitation Council of the Japan Ministry of Health, Labour and Welfare. JCR said marketing approval of JR-031 is anticipated in the near future.

JR-031 is a treatment for acute Graft Versus Host Disease (GvHD), a severe complication arising from hematopoietic cell transplants, which JCR has been developing in Japan utilizing technology under a licence from Mesoblast. JCR stated that clinical trials demonstrated the efficacy and safety of JR-031 which led to their filing for a marketing approval in September 2014.

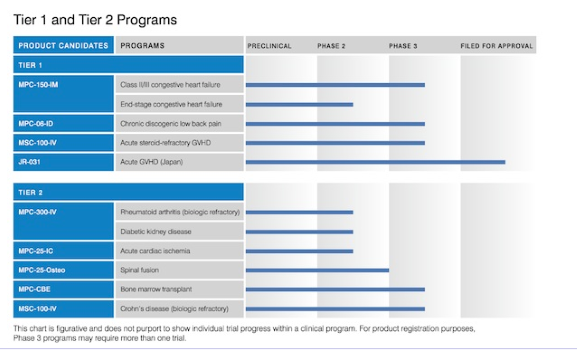

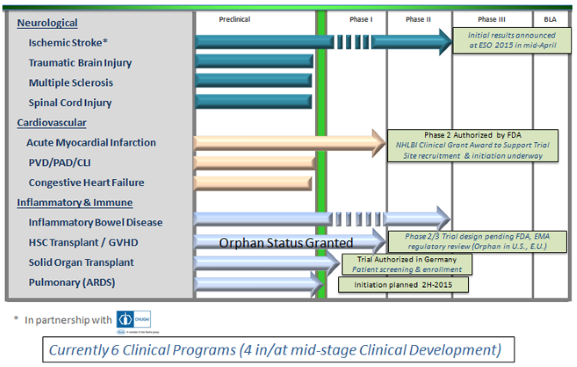

This is what the Mesoblast pipeline looks like today:

Mesoblast closed fiscal 2015 (June 30) with $101 million in cash on hand.

I highlight these three news articles because they represent significant progress in a sector that has been lacking significant positive news for some time now. The new fast track stem cell laws in Japan have been discussed for some time and this is concrete evidence that Japan is serious about encouraging regenerative therapies in the hope that they can help with an aging population and rising healthcare costs. I also highlight these news articles because I see them as relevant to two companies I have followed closely.

Cytori Therapeutics (NASDAQ:CYTX) uses the same cell source as Tigenix but uses an autologous (cells derived from the same patient during the same surgical procedure) model. Make no mistake about it, there are advantages to the allogeniec model. However, Cytori's system for extracting regenerative cells form fat is cost effective and the autologous model has already spread throughout the United States by virtue of the use of often inferior, unapproved competing technologies. While FDA guidance makes it clear that approval is needed the treat patients with their own adipose derived cells, this little detail hasn't stopped a burgeoning industry from growing rapidly. This recently published article called, Our Fat Future: Translating Adipose Stem Cell Therapyis a must read for those who want to get up to speed on this topic. Cytori, withfunding from BARDA, is developing a next generation system that will not only be faster and more efficient at extracting cells but will bring down up front capital costs dramatically. Relevant to Mesoblast progress in Japan with its partner JCR, Cytori recently announced the commencement of enrollment in a pivotal trial on stress urinary incontinence for which trial costs are substantially supported by Japan's Ministry of Health, Labour and Welfare. Can a company ask for a better partner in Japan than the Japanese government? Shares trade near all time lows as balance sheet concerns remain. However after a recent dilutive capital raise, the company reports $23.8 million in cash as of June 30, 2015 and states in its most recent quarterly release that this amount is enough to cover cash requirements for at least 12 months.

The next catalyst for Cytori could come from its Phase IIb knee osteoarthritis clinical trial that recently completed enrollment. Cytori desperately needs solid results in order to attract a partner with upfront cash. Cytori will share interim results in the first quarter of 2016. Cytori will also host an online investor's conference this week.

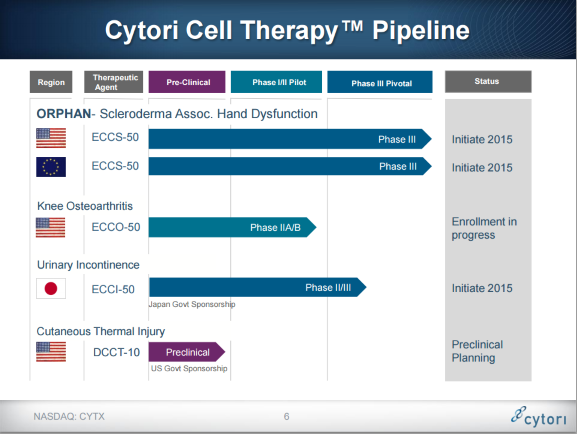

This is what the Cytori pipeline currently looks like today:

Another interesting aspect regarding Cytori is that even with its terrible performance there has been an interesting surge of recent insider buying that seems to be discounting the past:

Athersys (NASDAQ:ATHX) has much in common with Mesoblast but its market cap is not one of them (see chart above). Both companies use a cell type that is derived from bone marrow and both use the allogeneic model. However, the cell type used by Athersys (MAPC) has the very significant advantage of being able to proliferate into millions of doses from a single donor. Mesoblast cell types (MPC, MSC and DPSC) have limited expandability due to a loss of efficacy with each doubling, resulting in a more limited scalability from a single donor and likely an increased cost of goods sold.

The pending Japan approval by Mesoblast partner JCR for GvHD is relevant to Athersys in a couple of ways. First of all, Athersys is awaiting an important decision to be made by their stroke partner in Japan, Chugai Pharmaceuticals. Chugai must decide shortly whether to make a payment to Athersys in the amount of $7,000,000 in order to go forward with its option and continue working with Athersys on the stroke program in Japan. While the Athersys Phase II Stroke trial failed to meets its endpoints, results from a shorter treatment window and post-hoc analysis were encouraging. One can imagine that Chugai has been in contact with the appropriate officials of the Japan Ministry of Health, Labour and Welfare in trying to determine its next move and the positive news from Mesoblast and JCR Pharmaceuticals has to be considered an encouraging sign that demonstrates that Japan's commitment to regenerative therapies is genuine. I had interviewed the CEO of Athersys last year in this article before the Phase II stroke results were released. Also in common with Mesoblast is that Athersys has a program in Graft vs. Host Disease and has been granted Orphan Status in both the United States and the European Union. The Athersys therapy for GvHD seeks to treat patients in conjunction with a bone marrow transplant to prevent the disease from taking hold in the first place.

This is how the Athersys clinical pipeline looks today:

Athersys reported $32 million in cash as of June 30, 2015 and, according to their recent filing, this is enough to meet to meet their short-term liquidity needs. Future capital requirements will be highly dependent on the Chugai decision on stroke and the eventual path for this and other clinical programs.

Success in a few applications by a couple companies does not necessarily translate into success by the entire industry. However, there is much in common among the many companies in the adult stem cell space and we ARE finally witnessing seeing strong evidence that adult stem cells work. Will this sector get hot again? That is the big question ...but those companies that can execute, whether it be by choosing the right clinical path or partner, raising capital at the right time or by designing a clinical trial that succeeds, will be the companies that reward their shareholders with long term and sustainable appreciation.

stocks................................................................................ CAR-T looks great in the clinic, but how do you commercialize it?

Novartis ($NVS), Juno Therapeutics ($JUNO) and Kite Pharma ($KITE) have made headlines around the world with a new technology for modifying T cells to better attack cancer. But translating clinical promise into a marketable product will likely prove difficult if and when so-called CAR-T therapies win approval.

Column 1

0

1

Depiction of a CAR-T cell--Courtesy of Juno

As Reuters reports, each contender is working to get ahead of the issue by investing in in-house, commercial-scale manufacturing operations, deciding against the more common practice of relying on outsourcers.

Creating therapeutic CAR-Ts requires extracting cells from patients, genetically modifying them and then re-infusing the new material in a process that takes about two weeks per person, according to Reuters. That's a stark contrast to the scalable processes behind the small- and large-molecule therapies that dominate the market for most diseases, and making CAR-T cells for commercialization promises to be a complicated, expensive proposition.

Date: Wednesday, January 20 | 2pm ET / 11am PT

Regulators are becoming wary of self-assessments captured on paper, so join this session to learn what is currently driving ePRO decisions. Reserve Your Spot Today!

Novartis, expected to be the first to market a CAR-T therapy, has been churning out experimental doses of its product through a facility shared with its partners at the University of Pennsylvania and has acquired a commercial-scale plant from Dendreon, whose own attempts to market a cell therapy ended in bankruptcy. Juno is weaning itself off of contract manufacturing after leasing a Washington plant to crank out its investigational candidate, expecting to bring the facility online next year. And Kite has signed agreements to lease two production hubs, one for making experimental doses and another for commercial manufacturing.

In clinical data released over the past two years, CAR-T therapies have charted stellar results in rare cancers with particularly bleak prognoses, extending patients' lives and delivering complete remissions. Assuming each company can follow through on that promise in late-stage testing, the therapies are likely to win FDA approval, but the cost and complexity of manufacturing doses could limit the immediate market potential of the CAR-T class............................................................................................................... This article is part of a series The Conversation Africa is running on stem cell research and therapy. Read the rest of the series here.

Exploration into the use of stem cells has created a cauldron where scientists and regulators are increasingly pressurised to find ways of fast-tracking promising research into novel therapies.

Many countries are developing guidelines and legislation to balance the provision of stem cell therapies as quickly as possible, while still ensuring the safety and efficacy of treatments.

At the centre of this is the accelerated, or conditional, approval of medicine still under clinical development. This is opposed to medicine already proven to be safe and effective in humans, formally approved by the relevant regulatory authority and legally available for sale to the public.

Although the South African legal systems do not provide for any accelerated or conditional approval, heed should be taken of global developments. This will ensure that legal systems allow local scientific innovation to keep up with global pace setters and that patients are protected. Stem cells and investigational medicine

The use of investigational medicine, as we know it today, came about in the late 1980s. In an attempt to address lengthy drug development cycles and a growing AIDS epidemic, the US was forced to reconsider its strict guidelines around investigational medicine. It eventually amended them to allow access to investigational medicine under certain conditions.

This developed into the Food and Drug Administration’s (FDA) system of expanded access. This allows patients with serious conditions to receive investigational medicine that has not yet undergone formal product approval.

There are three prescribed categories of people who can get expanded access to investigational medicine:

individuals;

intermediate-size patient populations; and

widespread use under a treatment protocol.

For individual patients, the decision lies with a physician. They need to confirm that the medicine does not pose a greater risk to the patient’s health than the disease itself.

When large numbers of patients are involved, the FDA must still find evidence that it is safe to use. To qualify, the FDA must determine whether the condition is serious or immediately life-threatening, and that there are no alternative satisfactory treatments available. Access to investigational medicine must also not interfere with the necessary clinical trials required to receive formal product approval.

Similar to all other therapeutics that qualify as biological medicine, stem cells must go through lengthy clinical trials to prove their safety and efficacy before they can be approved by the relevant regulatory authority for public use. Before they received the final approval, stem cells remain investigational medicine.

This should not be confused with the countless bogus stem cell treatments often advertised online. Many of these treatments have not:

undergone clinical trials;

passed the first phase of these trials; or

received the go-ahead from authorities to be used as an investigational medicine.

Expanded access is gaining momentum

In many countries, access to stem cell treatments still classified as investigational medicine, is gaining momentum.

In addition to the US’s expanded access guidelines, the Right to Try Act was introduced in July this year. If passed, the bill, which is complementary to similar state laws, will stop the federal government from taking action to stop expanded access of investigational drugs to terminally ill patients. This will severely limit the FDA’s regulatory authority over expanded access in these instances.

Although federal laws trump state laws, twelve states have already enacted so-called “right-to try” legislation. This has created enormous legal ambiguity as these state laws are not really enforceable. But, in practice, the fear of violating the FDA’s requirements causes a reluctance to actually use these state laws.

Similarly, the European Medicines Agency has started a public consultation process of revised guidelines to implement accelerated access and conditional marketing authorisation. These are based on less complete clinical data. This will also accelerate patients’ access to medicines and address unmet medical needs.

The guidelines are specifically aimed at innovative medicines and target diseases where no treatment is available. It could provide patients with a major therapeutic advantage over existing treatments.

This public consultation process is hot on the heels of the highly debated Stamina Foundation debacle. This involved an Italian court ruling that unproven stem cell therapy on a three-year-old child with Krabbe disease, an incurable neurological condition, could continue.

The decision was based on the compassionate use of the therapy in patients with severe incurable diseases as a last resort. It also followed an official endorsement by the Italian Government in March 2013. The government decreed that the Stamina Foundation were allowed to continue stem cell therapy on 32 terminally ill patients. Their permission came without proof that the cell-based therapies were manufactured according to Italy’s legal safety standards.

After enormous criticism from Italian stem cell scientists, the treatments were halted by the Italian Ministry of Health in September 2014.

In Japan, the revised Pharmaceutical, Medical Devices and other Therapeutic Products Act came into effect in November 2013. It contains a specific section for regenerative medical products and allows for conditional, time-limited marketing authorisation to be given. The authorisation will only happen if a product’s safety is ensured.

The available clinical trial results should also predict likely efficacy. But the authorised products will still be subject to further safety and efficacy tests between conditional and final approval. Covering South Africa’s landscape

Stem cell therapy holds the possibility of curing a large number of diseases. However, almost all of these therapies are still in early development and clinical trial stages.

Access to these therapies prior to regulatory approval might not only relieve human suffering, but will also legally enable scientists to test and prove their efficacy via an alternative means (other than in the clinical trial setting).

Although the benefits from the developer’s perspective are apparent, the patient’s safety and best interest must remain top-of-mind. Most importantly, the expectations of potentially vulnerable patients should be managed sensitively and accordingly.

The universal nature of stem cells therapy begs for harmonised international regulation, and South Africa can learn and benefit from current global developments. This article based on a paper published in a special South African Medical Research Council flagship edition of the South African Journal of Bioethics and Law.

MSB Price at posting:

$1.69 Sentiment: Buy Disclosure: Held

A personalised tool to help users track selected stocks. Delivering real-time notifications on price updates, announcements, and performance stats on each to help make informed investment decisions.

Tweet

(20min delay)

(20min delay)