1. coaltrader.com.au/H. Bothma late March 2024 said"We believe the market’s overlooked how transformational this transaction is and expect a material re-rating once investors see the magnitude of cashflow generated from the combined operation.

The Acquisition – Doubling existing saleable production

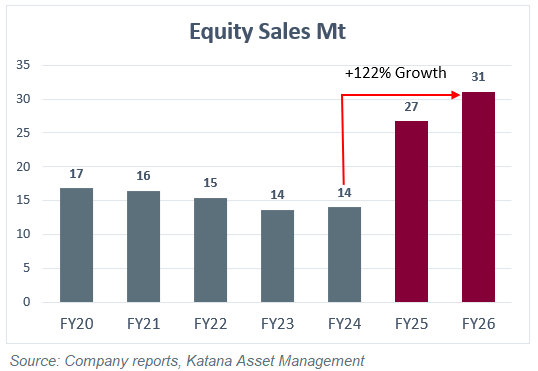

...The Daunia and Blackwater assets are in close proximity to Whitehaven’s existing operations and offers several strategic advantages. With the inclusion of these assets, sales are set to instantly double from ~14mt in FY24 to ~27mt pa. They’re also planning further growth at Maules Creek and the newly acquired assets to increase group sales to over 31mt pa by FY26. That’s an astonishing 122% (my emphasis) increase in production over a very short timeframe from FY23 (pre the acquisition) to FY26. Lets not glance over the fact that this isn’t some small operation that’s gotten bigger. This is one of Australia’s largest coal producers which is set to more than double.

The acquisition also enhances WHC’s sales mix. Historically >85% of Whitehaven’s sales are thermal coal used in energy generation, the remaining <15% of sales is metallurgical coal used in steel making. Post completion the sales mix (by volume) will be roughly even between thermal and met. This provides a more balanced exposure to the two different coal markets and also enhances their ability to blend an optimal sales mix...

Potential 20% sale of Blackwater

WHC is currently looking at the potential to sell down a 20% stake in the newly acquired Blackwater asset. This is a key near term catalyst which could occur before the end of CY24. Talks are already underway with potential partners and proceeds are estimated at US $1bn (my emphasis)

If Whitehaven achieves a sales price in this vicinity, they’ll have the flexibility to pay-out the newly acquired debt and soon be back in a net cash position. That means the cash flow generated from the larger business can flow straight to shareholders.

A key piece the market’s overlooking is there’s been no share dilution, shareholders now own a materially larger business, and the potential 20% sale of Blackwater could soon see them debt free.

Valuation / Upside

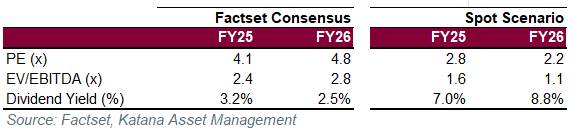

The multiples on WHC are cheap. We think there’s material upside to current consensus especially when compared to a current spot price scenario. Consensus figures are also very conservative with some analysts yet to reflect the acquisition in their forecast which understates future earnings.

The forward multiples for WHC represents exceptional value when compared to the ASX materials average of 12.1x. WHC’s PE of 4.1x represents a 66% discount to the sector, or 77% discount on current spot prices...".

Whitehaven Coal (WHC) – why a re-rate is imminent - The Coal Trader

Above quotes are only an extract from the link.

Enjoy!

2. The Australian 2.4.24 provided an analysis of the WHC purchase of Blackwater & Daunia- & its strong likelihood of doubling WHC's production & revenues (= BIG profits = Cash Machine).

https://www.theaustralian.com.au/subscribe/news/1/?sourceCode=TAWEB_WRE170_a_GGL&dest=https%3A%2F%2Fwww.theaustralian.com.au%2Fbusiness%2Fmining-energy%2Fwhitehaven-completes-64bn-deal-to-buy-queensl

Can anyone open, & post here please?

1. coaltrader.com.au/H. Bothma late March 2024 said"We believe...

Add WHC (ASX) to my watchlist

(20min delay) (20min delay)

|

|||||

|

Last

$7.18 |

Change

-0.070(0.97%) |

Mkt cap ! $6.006B | |||

| Open | High | Low | Value | Volume |

| $7.20 | $7.47 | $6.99 | $54.24M | 7.477M |

Buyers (Bids)

| No. | Vol. | Price($) |

|---|---|---|

| 2 | 4284 | $7.17 |

Sellers (Offers)

| Price($) | Vol. | No. |

|---|---|---|

| $7.18 | 70069 | 5 |

View Market Depth

| Last trade - 16.10pm 08/10/2024 (20 minute delay) ? |

| WHC (ASX) Chart |