I have refrained from posting over the past couple of weeks to avoid toxic bickering with non-holders and he-who-must-not-be-named, who are quite obviously & unsuccessfully trying to down ramp the stock with weak misinformation & spite, likely in the hope that shareholders here might shift their position into the stock that they have fallen in love with.

I’m sure everyone has now had time to digest the information released by the company and see the incredible value that can be crystallised here.

Many of us bought in several years ago hoping for BGS (now MLL) to be able to delineate ~1Moz at ~1g/t, and JV with Randgold (now Barrick) for a 35% stake in anything mined from our tenements.

Well now we get 80% (the maximum amount possible) of the mine, for peanuts, and 1.3Moz thrown in for free, let alone all of our gold sitting in our 685km2 contiguous tenements that surround the mine and continue along the Morila-Domba Shear Zone.

Barrick are a behemoth, a 40% stake in producing 50,000 ounces per year is immaterial to them. It makes sense why they have sold us Morila so cheap for a quick and easy sale and remove any further obligations to them. We were certainly in the right place at the right time.

We know that Barrick perhaps imprudently have not committed to any serious exploration here for the last 10 years, so the likelihood of exploration success is extremely high.

The company is basically a new IPO and RSG jumping on board at ground level is a huge vote of confidence, plus I would not be surprised if some savvy funds jumped in on the raise also.

I see immense potential here and have never been so optimistic about how large the company can now grow in the near term.

The following is basically how I see the strategy playing out maximise value to shareholders broken into 3 key components:

The “low” case = stage 1 of the broader strategy of the company, and appears very low risk (read basically guaranteed at this point) for a very high reward is to build ore reserves grading 1 – 2g/t to become a sustainable producer at >150,000 ounces per annum with a LOM >20 years:

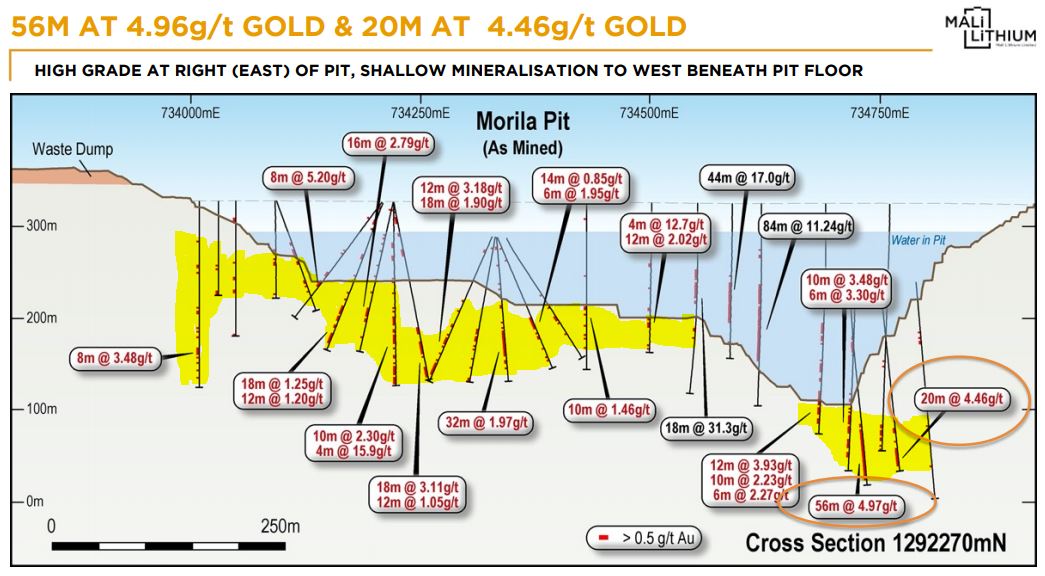

The Current JORC resource (no exploration risk) below the main pit = 32Mt @ 1.26g/t = 1.3Moz at $1250 gold price therefore ~$1000/oz AISC and 7 year LOM.

Based only on this known resource, we should conservatively be able to achieve a solid 1Moz reserve at 1.25g/t. Up the gold price assumption to $1850 and we probably get over 2Moz but at a lower average grade.

Not to worry though, Morila has historically treated “low” grade 1g/t ore and still demonstrated extremely low cash costs (not to mention ridiculously low cash costs when treating higher grades of 3g/t i.e. ~$150/oz!) due to excellent mineralogy and low cost environment.

When the resource is remodelled at say $1850 gold price and lower cut off grades, perhaps we could end up with circa 2Moz i.e. 63Mt @ 1g/t.

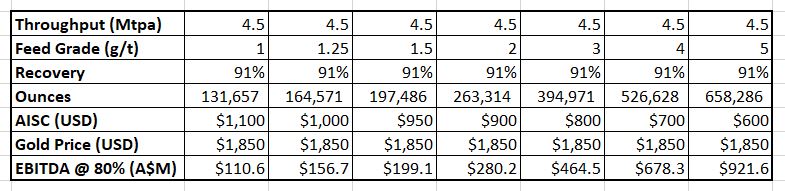

This results in an absolute base case of >130,000 ounces produced each year with a LOM of ~14 years generating an EBITDA of $110M AUD each year.

See table below which shows how the feed grade of the ore influences returns as the plant is capped at 4.5Mtpa (appears that it may be capable of achieving 5.5Mtpa) but high-grade zones can multiply potential earnings:

I think that in reality, the average feed grade will be higher than 1g/t and there will be many pockets of ore at ~2g/t and above that will boost earnings considerably.

It may take over 6 months for the main pit to be dewatered, infill drilled & stripped ready for mining, however this is where our satellite pits come in.

We know there are >300,000 ounces of gold at our satellite pits, Ntiola, Viper & Domba that were not mined by Randgold, let alone what we have found at the Koting discovery. Everywhere that we have drilled has intersected gold bearing ore bodies, so it is very likely that we will continue to do so at shallow depth & grades between 2 – 3g/t.

We will have >$25M to spend on exploration from tailings income, of which only a fraction will be required to pay for the drilling & studies required to convert these ounces to reserves.

These deposits have the potential to provide ore to feed the plant for several years if it were required, while the main pit is dewatered, infill drilled and stripped ready for mining which could be accomplished within 6 months.

The beauty here is we don’t need to build a processing plant, we have one already paid off, no additional dilution or debt required, no 2 year construction delay, and very little commissioning risk as the plant is already configured for Morila and its satellites’ ore.

All of the key commissioning & processing risks are eliminated or at least considerably reduced here. As soon as we hit pay dirt, we can start extracting cash from it. Not to mention we already have a considerable amount of known pay dirt awaiting our shovels.

From here we have choices, we can high grade production from any of the satellites or the Morila pit to maximise returns.

We know that the area hasn’t been seriously explored in 10 years, so there is huge obvious and extremely likely exploration upside with easy conversion to reserves by expanding the existing pit shell.

Don’t forget the existing tailings operation to provide additional income in the interim before things really ramp up - $17M USD is nothing to sneeze at, and I’m sure there will be plenty of more income from this stream as most of the overburden to be stripped will be able to be processed through here.

Another source of income down the track could be high grade underground zones near the main Morila lode i.e. Samacline that could be developed to expand the production profile if desired once the mine is back up to full operations.

So much potential upside with comparatively little downside risk:

What if other juniors offer up their high grade satellites to be toll treated by us where we now take 90% of the profits?

What if we pick up other ground for cheap that we can exploit with our paid off plant?

What if we have further exploration success (which is very likely) – particularly high grade zones?

What if the price of gold goes to $2,500/oz?

Therefore I see us mining satellites while the main pit is prepared, then cherry picking the highest grade or from our existing satellites, new satellite discoveries and the Morila pit to generate the most amount of income as quickly as possible to deliver maximum value to shareholders.

The cash generated can be injected back into exploration to continue to identify additional ounces resulting in a sustainable (and very highly profitable) operation.

This conservative and likely low case already provides ridiculous earnings relative to our current market capitalisation. Now we can get to the more optimistic/blue sky component of this proposition…

The optimistic case, or what I would put as stage 2 which would shoot the company into the stratosphere is what if we find another Gorilla?

This is what gold exploration shells on the ASX are trying to achieve, yet they generally only have ~$5M in the bank to drill their random plot of dirt.

We hold 685km2 of highly prospective ground in elephant country, sitting along the same trend that hosts Morila which is one of the largest and most geologically impressive mines in the world which is why it was able to generate billions of dollars for Randgold, AngloGold Ashanti and the Mali Government.

We will have >$25M to spend on exploration from tailings income, which will allow for tens of thousands of metres of drilling.

Twenty-five million chances to hit the motherlode.

Go back to the table I posted above. If we find significant tons of 5g/t ore, we are looking at almost 1 billion dollars in before tax earnings in one year of operations alone.

Even if we do not hit the motherlode, finding significant additional satellite resources is almost guaranteed.

Next year on the low case, we will have another $100M in free cash flow that we can throw back into exploration to continue the hunt.

This is the beginning of a sustainable mining operation, or “prospect generator” model as Kevin Joyce had initially envisioned for the company but was unable to execute on.

Thank our lucky stars that we now have Alistair Cowden leading the company to a potential 1 billion dollar and beyond valuation by getting this deal through.

Again, what happens if gold goes to $3,000 and beyond as some are predicting?

Who knows, another Gorilla could be located on our tenements, or Morila could only be a small part of a much larger feeder zone adjacent to the existing pit, luckily, we own all of the surrounding land so can go swiss cheese it and see.

So to summarise, we are getting ongoing cracks at finding a mother lode deposit with tens of millions of dollars in exploration budget each year, without having to worry about running out of cash as we will be continuing to receive huge profits from our sustainable mining operation.

Plus, if we do make a major discovery, production will be swift, we don’t have the typical commissioning & production risks, no need to finance and build a processing plant, so no additional dilution, debt, or years of construction time.

The third major component of the company that we must not lose sight of, is our Goulamina lithium project. This is a tier 1 hard rock lithium project, probably the most economic and geologically superior project in the world based on the figures in the PFS which are set to improve in the imminent DFS.

With reduced operating costs, it’s not unreasonable to think that that the DFS could demonstrate a ~1.5B NPV valuation up from the $1B NPV in the PFS and generate strong returns at current spodumene concentrate prices which may finally catalyse some strong commercial interest in the asset as developing mines and existing mines produce at $300 - $400/t and above while current spodumene concentrate pricing is around $400/t.

Remember that this is only assuming a 2Mtpa operation when the resource justifies 4Mtpa and beyond if sufficient market demand for the product returns, as the resource has significant scope to expand. If the project scale is increased to 4Mtpa, this will more than double the NPV of the project for a comparably small increase in capital investment.

The project is a lowest cost quartile producer and strategically located in close proximity to Europe.

Looking at our closest comparable, AVZ and LTR, we should be trading at a $200M market capitalisation at the moment, at minimum based on this asset alone.

Perhaps the income and increased market cap we will receive from Morila will allow investors to seriously rate Goulamina as an asset that can be developed and will price it accordingly.

With cash coming in from Morila, and a rerating of our market cap inevitably imminent, we will now have the ability to fund the lithium project when adequate demand for spodumene concentrate returns.

My personal preference would be to JV the project 50/50 and construct a lithium carbonate processing plant at the port of Abidjan. This would multiply profits again, decouple the company from the spodumene concentrate market and allows the strategic location to be taken advantage of by selling direct to battery manufacturing facilities in Europe.

Regardless, the project is incredibly valuable and I am confident that Alistair, a provendeal maker will be able to maximise shareholder value for it, whether it be JV, developing alone, spinning out into new entity, or even selling it to the highest bidder.

An entry at 16c (~$125M) MC is a steal of a ground floor entry into the behemoth of a company this could become.

I think this should rerate to $500M in quick time, with $1B on the cards in 12 months if management continue to kick goals, proving and executing production on the reserves and costs I have speculated on above.

If we hit the motherlode, the sky is the limit.

Don’t forget the lithium.

I am backing my conviction by purchasing more at these levels and will be taking my full allocation in the SPP.

The only realistic risks I see to the strategies outlined are time delays and budget overruns, but these are minor risks when looking at the big picture. Once this train gets going, minor impediments like this (if they occur) are not going to stop it.

The current price action reminds me of ADT when it retraced from its 20c IPO price and then once the normal enormous potential of its project (that had plenty of historical data much like Morila) was on the radar of major institutions, the SP rocketed to >$2.50

To reiterate, the base case alone of getting to a sustainable operation at 130,000 ounces per annum will result in considerable earnings for the company (~$110M EBITDA), and the risk of this not playing out is extremely low as we have the resource, we have the plant and we have the funding. In all likelihood the average grade will be higher and result in 165,000 – 200,000 ounces ($150M - $200M EBITDA).

The rough figures I calculated assume a gold price of $1850, however the price of gold is currently materially higher than this, therefore, these figures are conservative and will likely be higher again. Plus we have no debt so don’t require hedging, enabling us to benefit fully if the price of gold increases further.

Everything from here is upside, more tons, higher grades, lower costs, increased price of gold, and the ongoing chance of finding another Gorilla.

The satellites will be mined until the Morila pit is ready for mining, and then the highest-grade zones on our tenements will be cherry picked to front end production, maximising earnings.

Those earnings will then be reinjected into the ground to continue to generate additional mining reserves to continue the operation indefinitely, with the potential to discover another Gorilla.

Alistair is going about this the way it should be done, hard and fast – they are going to drill the day we get the keys to the plant, and fast track to production.

We don’t need to wait for red & green tape, we don’t need to wait for funding, we don’t need any additional dilution to fund, any debt to fund, we don’t need to wait 2 years for a processing plant to be built, and take on the commissioning risk that goes with a new plant.

If all goes well, we could be breaking ground at Ntiola and Viper to dig up some sweet high grade ore to get the plant back up to nameplate within 3 months of taking over.

Don’t forget the lithium.

MLL Price at posting:

15.5¢ Sentiment: Buy Disclosure: Held

(20min delay)

(20min delay)