We break down buy now pay later services available in Australia. Klarna is just one. Image source: rosstomei, Shutterstock.

We break down buy now pay later services available in Australia. Klarna is just one. Image source: rosstomei, Shutterstock.The buy now pay later (BNPL) industry has changed the payments landscape in Australia, with the services being used as a spending and budgeting tool by some, but racking up debt for others.

ASIC released a reporton the buy now pay later industry in November 2020 which revealed the substantial growth to the sector. The number of BNPL transactions increased from 16.8 million in the 2017-18 financial year to 32 million in 2018-19, representing an increase of 90%.

As a result, there’s been a considerable increase in BNPL debt in 2020, as revealed in Canstar’s latestConsumer Pulse Report. Close to one in five (18%) people surveyed said they have debt in the form of one BNPL service, up from 10% in 2019. The majority (56%) of Australians with debt still hold most of it on a credit card, but that’s down from 67% in 2019.

The COVID-19 pandemic appears to have played a part in the increasing use of BNPL services. From a survey of 1,000 people, Openpay revealed that nearly a quarter of consumers who held BNPL accounts in Melbourne and Sydney only started using them since the COVID-19 outbreak. And 31% of respondents reported having at least one BNPL account – of these, around a third held more than one account.

While the usage of BNPL services continues to rise, the industry that is exempt some of the regulation applied to other forms of credit, such as the National Credit Code, hasn’t escaped scrutinyabout how vulnerable consumers could be accumulating more debt and be worse off financially by using these payment methods.

To help you understand what BNPL involves for consumers, who some of the main providers are and how it could impact your finances, this article covers:

What is ‘buy now pay later’?

Buy now pay later (BNPL) is a service that allows consumers to purchase goods or services and pay for them in installments over a period of time. It has similarities with the lay-by system you might have used previously to buy a toy at Big W, for instance. Where lay-by sees a store put goods aside for you and then pay for them in two or more instalments, before taking your purchase home, BNPL services generally involve the provider paying the retailer for goods, allowing customers to take them home immediately. The customers then pays for the goods in instalments, which go to the BNPL service instead of the store. The services can be used at a growing number of retailers in Australia, in-store or online.

BNPL allows customers to buy things without having to take out a traditional loan, credit card or pay interest (in some cases). However, there are often late payment fees attached and the payment method could wind upcosting you the same as taking out a credit card or personal loan.

You might think a service like BNPL would mainly be used to buy relatively low-cost clothes and accessories, but this is not necessarily the case. With Afterpay, for instance, you can pay formore expensive goods and servicessuch as IVF treatment purchasing glasses or contact lenses, going to the dentist or getting veterinary care for your pet.

Buy now, pay later services can be used to pay for items such as prescription glasses. Image source: Zodiacphoto (Shutterstock).

Buy now, pay later services can be used to pay for items such as prescription glasses. Image source: Zodiacphoto (Shutterstock).How does buy now pay later work?

BNPL services are offered at certain retailers as another method of payment, rather than using your typical cash, debit card,credit card or PayPalaccount.

You can apply to use BNPL via the provider’s app or website and then log into your account during an online transaction or display a purchase code via the app in a store. Alternatively, you could have an account set up for the first time during the transaction process at a retailer and wait to receive approval for your spend amount from the BNPL provider. Approvals for BNPL are generally processed shortly after you provide your details.

Whether or not you can use BNPL will depend on if the retailer is partnered with the service.

The repayments you pay would typically be deducted automatically from the card or bank account you have attached to your BNPL account. This happens at regular instalments – commonly fortnightly. If you don’t have enough money in your account at the time of the deduction, the BNPL provider may charge you a late fee. Some BNPL services may also charge additional fees or interest if you fail to fully repay a purchase within a certain timeframe.

Compare buy now pay later providers in Australia

Below are some of the buy now pay later providers in Australia (listed alphabetically), and some information about how they work and what they cost. It’s important to check with individual providers to confirm details about the service.

Affirm (not yet launched)

Afterpay

Brighte

Bundll

Humm

Klarna

Latitude Pay

Laybuy

Openpay

Payright

Sezzle

Splitit

Zip Money

Zip Pay

Are buy now pay later services worth it?

BNPL services can be convenient forms of payment for some, and may appeal to people who want to spread out their payments but still receive a product instantly, without having to use a credit card. But there could also be some of the following significant financial risks involved:

People who may already be financially vulnerable are relying on these services the most

Roy Morgan Research in 2019 found people aged between 14-34 accounted for the biggest pool (55.9%) of Australian BNPL users, of whom most tended to be employed, but earning an average or relatively low wage.

In areport released in November 2020, ASIC found one in five consumers in the past year had missed or were late paying other bills in order to make their BNPL payments on time. Missed payments included things such as household bills (44%), credit card payments (32%) and home loan repayments (22%).

ASIC also found some consumers were experiencing financial hardshipin an attempt to make BNPL payments on time, with reports of people cutting back on or going entirely without essentials such as meals, or taking out additional loans.

While most of the services are interest-free, costs can still quickly add up

Afterpay, for instance, has been reported to makea significant chunk of its income from late fees, with the remainder coming from surcharges on its retailers. It since implemented a cap on late fees following scrutiny of its business model by consumer groups and regulators, cutting fees for each order above $40 off at 25% of the purchase price or $68 (whichever is lower). For orders less than $40, a maximum of $10 in late fees can be applied per order.

Most of the BNPL services listed in this article say they will notify customers of upcoming payments, and suggest getting in touch if you think you might be unable to make a payment on time.

BNPL services are not subject to the National Credit Code

ASIC stopped short of recommending new consumer protections for the BNPL industry, in its review published in November last year. The industry is not subject to the National Credit Code, meaning that customers who use these services do not have the same kind of protection as they do with credit cards or personal loans, which are regulated by the Code. It also means there is no requirement for a BNPL service provider to adhere toresponsible lendingobligations, such as by checking if you can actually afford to make the repayments.

ASIC has recommended BNPL platforms take steps to ensure their products are only targeted to appropriate customers, and that new checks and balances be implemented in a voluntary code of conduct, which is expected to be launched in March 2021.

BNPL providers have previouslyarguedthat applying theNational Credit Codewould slow down the approval process for customers, which currently tends to be rapid and easily accessible.

What’s more financially responsible: Credit cards or buy now pay later?

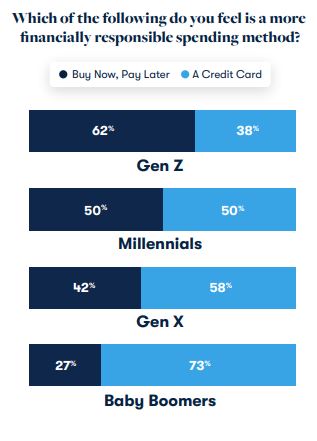

Canstar asked consumerswhat form of payment they felt was more financially responsible: a credit card or buy now, pay later services such as Afterpay and Zip. Of those surveyed, 60% said they viewed credit cards as more financially responsible, down from 68% the year before.

The younger generations had a more favourable opinion of buy now pay later services. Canstar’s research showed 62% of Gen Z thought buy now pay later was more financially responsible than using a credit card, while only 27% of Baby Boomers thought so.

Canstar Consumer Pulse Report 2020.

Canstar Consumer Pulse Report 2020.| Base interest only | Total interest including bonus | ||||

|---|---|---|---|---|---|

| Up Savers |

| 0.00% | 1.10% | ||

| Flexi Saver |

| 0.05% | 0.85% | ||

| Serious Saver Account |

| 0.05% | 0.90% |

Do buy now pay later providers do a credit check?

Most BNPL providers say they may perform a credit check on you. This could be done when you apply for an account, and some providers may also do this when you make a transaction to make sure you can make the repayments. In some cases, a credit check may be recorded on your credit report.

It’s worth also noting, that yourcredit scoremay be affected on other ways if you use these services, according toASIC. This is because if you take on more credit than you can afford and can’t keep up with repayments, your BNPL provider may report any late payments or defaults to credit reporting agencies.

But whether or not a credit check is conducted and whether your credit score will be impacted will largely depend on the BNPL platform you are using. That’s why it’s important to read their terms and conditions carefully before deciding to sign up or make a purchase with a BNPL provider. Here are some examples what some of the prominent BNPL providers in Australia say they do when it comes to credit checks for their customers.

Afterpay

- Afterpay says it may order a credit report and perform “other repayment capability checks” to assess your ability to make payments, and may report any negative activity on your Afterpay account to credit reporting agencies. Such activity could include late payments, missed payments, defaults or chargebacks.

→ More details:Does Afterpay affect your credit score?

Bundll

- Bundll says it won’t check your credit history or leave an enquiry footprint on your credit file, but it will for those who access superbundll.

Laybuy

- Laybuy performs a credit check on all new customers who register for its payment platform. Any payment default may result in its debt collection service contacting you, and your credit score may be affected.

Openpay

- For some purchases with Openpay, customers may be asked to consent to a credit check before making the purchase.

Splitit

- Splitit claims credit ratings will not be impacted at all by declined payments and there is “no impact” on customers’ credit scores.

Zip

- Zip says it may perform a credit check upon application to the service, to confirm you can make repayments. The checks are actually performed by third parties Equifax or illion.

If you’d like to read more information about buy now, pay later services, you may be interested in the following articles:

This story has been updated. Feature image source: rosstomei (Shutterstock).

This article was reviewed by ourDeputy Editor Sean Callerybefore it was updated as part of ourfact-checking process.