From the AFR - Interesting how crowded it is getting and how important it is to have patent protected bit in the middle.

i.e the ad hoc decision at the time of purchase

Flood of new BNPL entrants cranks risk for investorsThe stunning growth of the sector is bringing new regulatory attention and highlights how merchant fees may be vulnerable to pressure.

Tom RichardsonJul 27, 2021 – 5.09pmHuge valuations for buy now, pay later players will be tested over the August reporting season as new research underlines how this year’s dramatic evolution of the space threatens to hurt profit margins if merchants demand cheaper fees.

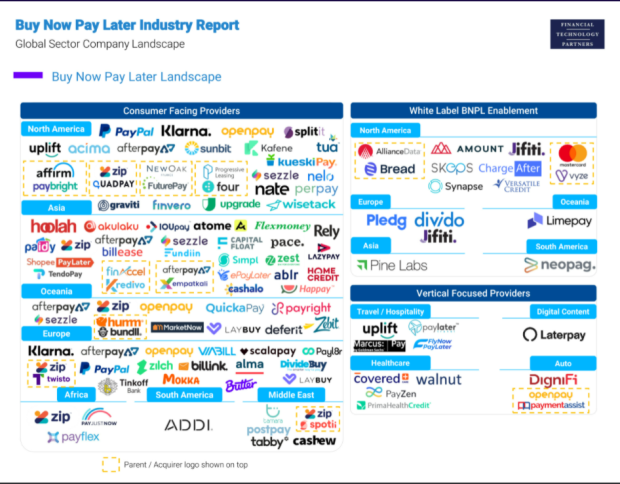

The report, by US investment bank Financial Technology Partners (FTP), highlights the incredible amount of competition to enter the sector since April 2020. American Express, JPMorgan, Citi, Citizens Bank, Goldman Sachs, ICICI Bank, National Australia Bank, Commonwealth Bank, Royal Bank of Canada, Tencent and Visa, among others, have all announced new product initiatives in the space.

A starker picture is of the rush of new direct players aiming to win market share globally. In the US and European markets that are key to growth for Afterpay, Zip and Sezzle, direct new entrants include PayPal, Tua Pay, Uplift, Acima, Kafene, DivideBuy, Zilch, Payl8r, FuturePay, Four, NeloPay, Nate, Perpay and Scalapay, among numerous others.

The number of pure buy now, pay later players is growing rapidly globally. Financial Technology Partners

The growing competition among new entrants and established players is relevant because influential analysts partly base their valuations on sales growth forecasts and the lenders’ potential to maintain, or grow, margins driven by merchant fee take rates.

Analysts at Morgan Stanley expect Afterpay to swing from a $59 million loss in financial 2021 to a $159 million profit in financial 2022 and $359 million profit in financial 2023. The broker has a $145 valuation on the stock, broadly in line with the market, but if the profit growth forecasts are cut by the market, the shares face downside risk.

For investors, it is worth noting that in business, falling profit margins are nearly always a symptom of too much competition, weak moats, or both. Rising margins and sales can be a potent combination as even loss-making businesses such as Afterpay, Zip, or Sezzle could swing to profit on them. For now the future remains unknown.

Regulatory attention

Another big issue around the rocketing number of new market entrants is that it is bringing the entire sector onto the radar of global lawmakers wary of businesses exploiting less creditworthy consumers.

In the US on July 15, Democratic Senators Dick Durbin, Jeff Merkley, Richard Blumenthal and Sheldon Whitehouse reintroduced legislation that would implement a federal rate cap of 36 per cent on annual percentage rates (APR) levied by consumer lenders.

If passed, the laws would mean all consumer lenders must calculate how late fees and other instalment fees increase the APR levied on debt owed. The legislation aims to protect US consumers who cannot get credit cards or bank loans from predatory lending, which are a big part of the buy now, pay later demographic.

Calculating APR fees for different lenders masquerading as fintechs is complicated. For example, Afterpay charges a $10 late fee on sales below $40, a late fee that will not exceed 25 per cent annualised on sales from $40 to $272, and a late fee that will not exceed $68 on sales over $272.

If a consumer were to default on a $100 purchase after paying $25 upfront, the $75 default attracts a $10 late fee plus $7 per bill cycle. This is 22.6 per cent annualised interest in six weeks, which is equivalent to top tier penalties on credit cards.

An unpaid debt of $30 on a $40 purchase will attract $10 in late fees on $30 owed after eight weeks, which is 36 per cent annualised interest. This is right on the proposed new legislative cap. This might make the glass half full for Afterpay bulls, but the glass half empty view is that it exposes the late fees as borderline outrageous and as bad as any credit card product gouging consumers.

So even if the ballooning number of new fintech lenders escape new APR caps, it is no surprise they are coming into greater regulatory focus in the US, Britain and the EU.

In Australia, the imposition of the “no surcharging” rule on merchants gets harder to defend as the sector grows as a percentage of payments on a daily basis. Meanwhile, the nation’s unique status as a mature buy now, pay later market perhaps shows investors growth can peak as a market saturates.

Afterpay’s underlying sales in Australia and New Zealand over the March quarter were $2.1 billion, versus $2.6 billion in the prior Christmas 2020 quarter, and $2.2 billion in the September 2020 quarter – a downward trajectory that gives cause for concern in the context of a toughening outlook at home and abroad.

Watch This Space, page-5103

-

-

- There are more pages in this discussion • 2,932 more messages in this thread...

You’re viewing a single post only. To view the entire thread just sign in or Join Now (FREE)

Featured News

Add SPT (ASX) to my watchlist

Currently unlisted public company.

The Watchlist

LPM

LITHIUM PLUS MINERALS LTD.

Simon Kidston, Non--Executive Director

Simon Kidston

Non--Executive Director

SPONSORED BY The Market Online