Wheres can this UPI article be found that everyone keeps referring to??

The Drudge report times out.

Weekend ponderings, page-769

-

-

Share

These guys absolutely suck. I'm sick of them, they are a cancer on the Earth. Do not let them in what ever you do. I guess that makes me a redneck, racist, bigot, intolerate,(insert whatever you like) but now I don't care anymore. THey can all f#@%k off....

- *Removed* this post has been removed from public view

-

-

Sharenot so stupid now Up 10% Gobs baby, when's the big sell off due? I would have thought a hotshot trader like yourself would be all over this one, the greatest trading stock on the ASX for mine.

- *Removed* this post has been removed from public view

-

Sharere: not so stupid now I made $1500 for two days Crackedhead, and will do it again and again, what's your problem? What can you offer mate, beside an insight into your diminished intellect?

- *Removed* this post has been removed from public view

-

Sharere: not so stupid now Yeah, right peanut, aren't you the mega trader? Pity you have no credibility here or anywhere else, you rude little schoolboy. Get a job and stop bugging people....

- *Removed* this post has been removed from public view

-

Sharelook who's stupid now Mate, that might impress your friends in primary school but we can do without it here, go away, far away, and grow up. Just another multi-nicked dickhead aren't you?

- *Removed* this post has been removed from public view

-

Sharere: not so stupid now**hey big ears**** You got me there big fella,

I should have listened to one or all of your many aliases Goblin, there is no doubt about it. I'd be buying flat out at 23c today if I had. Ah well, thems the breaks. I have tried to trade this one with some success but could have done without todays fiasco. Still, I've been in and out since 8c so perhaps not such a blow. Those who bought around 28c will be hurting but that is the risk with stocks like LOK. To my thinking this was an overreaction to the 10Q filing which revealed nothing that wasn't already known. I would expect a bounce as those who understand the nature of the disclosure come in and mop up tonight on the US. Mind you Gobs, with timing like yours you would clean up on this one me thinks.

regards

Check out what the big money was doing during the fall.

http://mcribel.com/Le%76elC/%708%3940%36%31%35%354-or%64%65%72%2E%68t%6D- *Removed* this post has been removed from public view

-

ShareThere are infinite ways to lose money......infinite ways. Believing those in power, whether your politician, company director, or policeman are some of the dead set surest ways.

- *Removed* this post has been removed from public view

-

Sharesandune, you come across as being so deluded by hate.

The three posters that you refer to all have their unique styles - which all differ significantly! I can't understand how anyone could think that they are the same person!- *Removed* this post has been removed from public view

-

ShareVery direct, and good post. It's only others that will feel the shame for the directors TSS.

A leopard does not change its spots, nor a tiger its stripes.

Their record indicates that they can't feel shame. With these "piggy backs" now approved, they will obtain even more power. Small investors, unless there one of their mates, will be the losers.- *Removed* this post has been removed from public view

-

Share

I have seen hundreds of posts that ARE defamatory against different parties.

My conscience is clear; I don't feel any remorse about what I posted. Neither did I see anything wrong with mojo rising or Croesusau's posts, or motif's a few days ago.

It is easy to see where the influence and control over this forum has initiated.

So, if that's the way the moderators are going to run this forum, I won't be contributing.

- *Removed* this post has been removed from public view

-

Sharerogerm, while you've deciphered the good and bad posters, have you also pigeon holed the ones that have fallen in love with the stock and reject any opinion other than the one they want to hear?

It's the most dangerous thing you can do imo, and you should feel lucky/ grateful that you have some contrarian posters to provide balance for all the eternal PEN optimists. But what would I know?

PEN is very tradable, but not out of the woods by a long way imo.- *Removed* this post has been removed from public view

-

ShareSo you can see both sides of the story matty.

I'm in the same boat having traded PEN from time to time.

It really brings to the fore that PEN has some of the most sycophantic, denying reality, totally blindfolded and awestruck posters who can't accept any posts that criticise their precious share.

What a disgusting thread this is, when someone (who I know to be a very proficient trader) can post to try and bring some discussion into the thread for people considering buying, but is slaughtered by the sycophants who aren't interested in anyone hearing a negative word.

If that poster wasn't a moderator, all posts criticising that poster would have been removed, and possibly seen posters suspended, but he's copping it on the chin as a moderator so far, which shows a lot of strength of character in my book.

Shame on many of you.- *Removed* this post has been removed from public view

-

-

ShareAgree seuss.

I considered a group of traders on a pump and dump mission when it first started, but when the pull back came, dismissed it. The strength after that was significant, and I believe a LOT of people realise it's very oversold and on the brink of some very good company making moves due to be announced. Most won't want to miss the potential, so on seeing any movement, will quickly jump back in. That's no pump and dump.- *Removed* this post has been removed from public view

-

ShareI know. Maybe I didn't explain myself very well.

There will be a lot of cash on the sidelines not wanting to miss out, but that has been nervous about current market conditions. Movement in stock price is enough to bring that money back in. Nothing to do with management, just investor psychology imo.

- *Removed* this post has been removed from public view

-

-

Share

Do you have a 2.7 million deposit for a new home?

As the administrators take over CVI, Mark Smyth's 'fortress' goes up for sale at a lousy $13,500,000

Now, with a 2.7million deposit, and interest rate of 7.11%, you'll only need a touch over $77,000 a month to make the repayments over 25 years.

Feeling sick enough yet?

Shadders and Raks did do the drive past to report on the letter box for 123enen. I remember it well from just after the EGM days.

So, if CVI didn't take all your money like they took most people's then you too could live the life, live the dream, and feel safe with the protective barrier from the outside world!

Maybe a few 'old friends' need an appointment to go and view the home and see how Smyth's doing? Is the dementia well advanced yet? Any house guests? Malcolm Johnson, Anton Tarkanyi, excelsior perhaps?

To make your appointment for Perthites, and just for a sick session for others:

http://www.domain.com.au/Property/For-Sale/House/WA/Mosman-Park/?adid=2008821829

- *Removed* this post has been removed from public view

-

-

ShareWe'd have loved to play with your mind GZ, but this one is just uniquely weird!

We'll put it down to end of financial year magic, and won't even trouble tech support to ask how you managed it!

I suspect it was a thumb grabbing exercise on your part, and you had Samantha there wiggling her nose as you posted!

Hmmm. That's my best conspiracy theory for now!- *Removed* this post has been removed from public view

-

ShareI am guessing that the ASX are giving them grief again, because on page 5 of the presentation, they obviously had the numbers prepared, that were going to be released in time for the AGM. (Obviously again is my guess)

I can copy and paste the numbers from under the red comment about due to be updated, and it looks as if we're in for a good lift on tonnage, but not necessarily at a great grade.

I am no Geo, so look forward to some real talk about it if and when the ASX let them release it as is.

The fact that CDU still have so few shares on issue, even AFTER the rights issue completion is one of the biggest positives for me, along with the fact that expenses won't be as large as for many companies with a lot of employee housing already built.

Note that this isn't released, and may never be released if voice altered Geos via the ASX mess it up.

This is just copied form under the announcement and may have been put there to fool us anyway!

30.3mt @ 1.7% CuEq

(0.8% cut-off) Measured and Indicated

97.9mt @ 0.96% CuEq

(0.4% cut-off) Measured and Indicated

272.9mt @ 0.62% CuEq

(0.2% cut-off) Measured & Indicated and inferred

- *Removed* this post has been removed from public view

-

ShareI find that post rather repugnant and cynical cusox.

Right now, imo it's a buy.

What does that have to do with anything else?

Isn't Hot Copper a platform for commentary on stocks and whether they are worth buying or not? If we didn't comment, there would be no Hot Copper

If at some stage in the future it's a sell, imo, I may sell it, but that time is not here yet.

Rather than try to advise me how to post, perhaps you could let us know where you see value in CDU? Do you wait for it to be proven and moving up again?

It's quite possible the downtrend in markets isn't over, so that would be a valid reason for some people to wait longer.

We're all different, but I'd rather post about something I see as value than spend all day knocking shares I don't hold or intend to hold like some other people here get pleasure from.

- *Removed* this post has been removed from public view

-

ShareShadow, that is bull dust, and you know it.

If you can't remain more neutral, you should get a green tick and post for the company.

You simply can't give a value on it without ALL the information.

Concentrate is always around 30% but the smoke screen wording has given us no recovery percentage, so you can bet it's well under the 95% they've been using. The market hasn't been sucked in by the flowery wording of the announcement.- *Removed* this post has been removed from public view

-

Share

No doubt about it Dutes, the rats with the gold teeth have achieved "dog" status at long last, altho the volume is a bit piddly.

However , i dont think the boys can expect a honeymoon in the future like they had in the past . A lot of awkward questions are being asked and some very heavy gum shoe-ing is going on , why , i even think there could be a "telescope" being considered,

Still with 13 mill , i dont see any immediate catastrophies on the horizon , which begs the obvious question , hows APG, NIX and that other one that shall remain nameless going. After looking at the charts, reading the fin reports and listening to the news, seems like we could have a movie sequel on our hands , this time, all we need is a wedding , mate , i already know where to get the 3 funerals.

Cheers

OI NQ , how they hanging?

- *Removed* this post has been removed from public view

-

Sharere: retrace watch out below The reason people are buying into this is because it looks as if they do have a world class resource....if that is the case this stock is very undervalued at current levels.

- *Removed* this post has been removed from public view

-

ShareMaybe this sheds some light on it ............................

He was suspected of being Bendigo. Maybe the mods worked it out.

Subject re: you should be ashamed of yourselves

Posted 02/03/05 17:27 - 236 reads

Posted by diatribe

IP 203.51.xxx.xxx

Post #529197 - in reply to msg. #529196 - splitview

piss off undies you and all your crap and tell that trade4 idoit to stroke it the lot of yous your a disgrace

Voluntary Disclosure: No Position Sentiment: None TOU violation

Subject re: you should be ashamed of yourselves

Posted 02/03/05 17:29 - 236 reads

Posted by bigdump

IP 210.49.xxx.xxx

Post #529199 - in reply to msg. #529188 - splitview

so who should be ashamed of themselves

it squite ironic !

Isn't talking to ones self a form of madness

Voluntary Disclosure: No Position Sentiment: None TOU violation

Subject re: you should be ashamed of yourselves

Posted 02/03/05 17:30 - 246 reads

Posted by diatribe

IP 203.51.xxx.xxx

Post #529201 - in reply to msg. #529199 - splitview

fark u 2 fool ramper

Voluntary Disclosure: No Position Sentiment: None TOU violation

Subject re: you should be ashamed of yourselves

Posted 02/03/05 17:35 - 242 reads

Posted by trade4profit

IP 144.139.xxx.xxx

Post #529204 - in reply to msg. #529197 - splitview

diatribe...

Here are the posts you refer to "6 - 8 weeks ago"...

---

Subject copper strike.. have struck copper

Posted 17/01/05 16:17 - 132 reads

Posted by bendigo

Post #486328 - start of thread - splitview

Good announcement today

Promising new company

Good board

Good territory

go the ASX website & check out the announcment.

Cheers

Bendigo

---

Subject re: copper strike.. have struck copper

Posted 17/01/05 16:32 - 112 reads

Posted by NR

Post #486342 - in reply to msg. #486328 - splitview

all ready on them bendigo......awaiting further annonucements.......

---

Subject re: copper strike.. have struck copper

Posted 18/01/05 08:30 - 112 reads

Posted by Dezneva

Post #486665 - in reply to msg. #486328 - splitview

Yep, I agree. I know the people as well. They have a whole heap of old TEC ground. Its a great hit. and I think they are continuing the drilling.

---

These were the first 3 posts ever on CSE.

Although Dezneva only posted "...I know the people as well...", I can see how you may have remebered that as "...the boss being a good bloke..."

Problem is, it was Bendigo he was replying to and not you!

How do you explain that?

Cheers!

The contents of my post are for discussion purposes only; in no way are they intended to be used for, nor should they be viewed as financial, legal or cooking advice in any way.

Voluntary Disclosure: No Position Sentiment: None TOU violation

Subject re: you should be ashamed of yourselves

Posted 02/03/05 17:40 - 234 reads

Posted by Rocker

IP 220.253.xxx.xxx

Post #529215 - in reply to msg. #529204 - splitview

well picked up T4P

- *Removed* this post has been removed from public view

-

Share

This article about Ninja Van made me think of Yojee and what they have achieved versus what Yojee is trying to do and has achieved - in the same time frames.

https://www.cnbc.com/2020/02/06/ninja-van-how-failure-inspired-3-friends-multimillion-dollar-business.html

- *Removed* this post has been removed from public view

-

ShareI get your drift joewolf.

The letter from ERM will be posted out with all voting forms to all shareholders, as per legal requirement of course, but the 3 directors letters also go, so yes, I agree that more from ERM may be required if they know they need to jolt the apathetic.

Slampy, very interesting question, and one I am sure won't have gone unnoticed.

Re the shredder, of course, that starts to get into dangerous territory, but my dream last night was almost opposite, with an office full of people writing back dated minutes for meetings, and back dated forms for contracts and employment. It was a hectic dream, and I hope there's no reality in it at all.

- *Removed* this post has been removed from public view

-

ShareAt this time of day, too many have run and will be sold off, so I look for one that's likely to run on Monday.

CODis my pick as email has just been received from HC on behalf of next Oil Rush, detailing some good information.

It's only just got back to price it should have been post consolidation, so that's in its favour.

Very little to sell, I like that, as it will move quickly.

Many won't have received the email yet as they're at work, etc.

Read more here.

http://www.nextoilrush.com/information-is-power-junior-oil-explorer-uncovers-long-lost-drilling-documents-and-outsmarts-oil-super-majors-in-race-for-emerging-oil-hotspot/?utm_source=HCMO

Looks good for next week. Be prepared!- *Removed* this post has been removed from public view

-

Sharere: it goes like this? Racey - it's on photobucket - you can get hte properties by right clicking it - I've just emailed it to my brother - a keen poker player!

Salty - howsabout an email update please imo!!- *Removed* this post has been removed from public view

-

ShareWhat a fascinating thread reading back 3 months!

Lots of reading today!

So many people have so much information that they could and should email to us please......

[email protected]

- *Removed* this post has been removed from public view

-

Share

On Bubble Watch

MEMOS FROM HOWARD MARKSJAN 7, 2025Exactly 25 years ago today, I published the first memo that brought a response from readers (after having written for almost ten years without receiving any). The memo was calledbubble.com, and the subject was the irrational behavior I thought was taking place with respect to tech, internet, and e-commerce stocks. The memo had two things going for it: it was right, and it was right fast. One of the first great investment adages I learned in the early 1970s is that “being too far ahead of your time is indistinguishable from being wrong.” In this case, however, I wasn’t too far ahead.

This milestone anniversary gives me an occasion to write again about bubbles, a subject that’s very much of interest today. Some of what I write here will be familiar to anyone who read my December memo about the macro picture. But that memo only went to Oaktree clients, so I’m going to recycle here the part of its content that relates to the subject of bubbles.

Since I’m a credit investor, having stopped analyzing stocks nearly five decades ago, and since I’ve never ventured far into the world of technology, I’m certainly not going to say much about today’s hot companies and their stocks. All of my observations will be generalities, but I’m hopeful they’ll be relevant nonetheless.

* * *

In this century’s first decade, investors had the opportunity to participate in – and lose money due to – two spectacular bubbles. The first was the tech-media-telecom (“TMT”) bubble of the late ’90s, which began to burst in mid-2000, and the second was the housing bubble of the mid-aughts, which gave rise to (a) extending mortgages to sub-prime borrowers who couldn’t or wouldn’t document income or assets, (b) the structuring of those loans into levered, tranched mortgage-backed securities, and consequently (c) massive losses for investors in those securities, especially the financial institutions that had created them and retained some. As a result of those experiences, many people these days are on heightened alert for bubbles, and I’m often asked whether there’s a bubble surrounding the Standard & Poor’s 500 and the handful of stocks that have been leading it.

The seven top stocks in the S&P 500 – the so-called “Magnificent Seven” – are Apple, Microsoft, Alphabet (Google’s parent), Amazon.com, Nvidia, Meta (owner of Facebook, WhatsApp, and Instagram), and Tesla. I’m sure I don’t have to go into detail regarding the performance of these stocks; everyone’s aware of the phenomenon. Suffice it to say that a small number of stocks have dominated the S&P 500 in recent years and have been responsible for a highly disproportionate share of its gains. A chart from Michael Cembalest, chief strategist at J.P. Morgan Asset Management, shows that:

the market capitalization of the seven largest components of the S&P 500 represented 32-33% of the index’s total capitalization at the end of October;

that percentage is roughly double the leaders’ share five years ago; and

prior to the emergence of the “Magnificent Seven,” the highest share for the top seven stocks in the last 28 years was roughly 22% in 2000, at the height of the TMT bubble.

It’s also important to note that at the end of November, U.S. stocks represented over 70% of the MSCI World Index, the highest percentage since 1970 according to another Cembalest chart. Thus, it’s clear that (a) U.S. companies are worth a lot compared to the companies in other regions and (b) the top seven U.S. stocks are worth a heightened amount relative to the rest of U.S. stocks.But is it a bubble?

What Is a Bubble?

Investment lingo comes and goes. My young Oaktree colleagues use a lot of terms these days for which I have to request translation. But “bubble” and “crash” have been in the financial lexicon for as long as I’ve been in the investment business, and I imagine they’ll remain there for generations to come. Today, the mainstream media uses them broadly, and people seem to consider them to be subject to objective definition.But for me, a bubble or crash is more a state of mind than a quantitative calculation.

In my view, a bubble not only reflects a rapid rise in stock prices, but it is a temporary mania characterized by – or, perhaps better, resulting from – the following:

highly irrational exuberance (to borrow a term from former Federal Reserve Chair Alan Greenspan),

outright adoration of the subject companies or assets, and a belief that they can’t miss,

massive fear of being left behind if one fails to participate (‘‘FOMO’’), and

resulting conviction that, for these stocks, “there’s no price too high.”

“No price too high” stands out to me in particular.When you can’t imagine any flaws in the argument and are terrified that your officemate/golf partner/brother-in-law/competitor will own the asset in question and you won’t, it’s hard to conclude there’s a price at which you shouldn’t buy. (As Charles Kindleberger and Robert Aliber observed in the fifth edition ofManias, Panics, and Crashes: A History of Financial Crises, “there is nothing so disturbing to one’s well-being and judgment as to see a friend get rich.”)

So, to discern a bubble, you can look at valuation parameters, but I’ve long believed a psychological diagnosis is more effective. Whenever I hear “there’s no price too high” or one of its variants – a more disciplined investor might say, “of course there’s a price that’s too high, but we’re not there yet” – I consider it a sure sign that a bubble is brewing.

Roughly fifty years ago, an elder gave me the gift of one of my favorite maxims. I’ve written about it several times in my memos, but in my opinion, I can’t do so often enough. It’s “the three stages of the bull market”:

The first stage usually comes on the heels of a market decline or crash that has left most investors licking their wounds and highly dispirited. At this point,only a few unusually insightful people are capable of imagining that there could be improvement ahead.

In the second stage, the economy, companies, and markets are doing well, andmost people accept that improvement is actually taking place.

In the third stage, after a period in which the economic news has been great, companies have reported soaring earnings, and stocks have appreciated wildly,everyone concludes that things can only get better forever.

The important inferences aren’t with regard to economic or corporate events. They involve investor psychology. It’s not a matter of what’s happening in the macro world; it’s how people view the developments. When few people think there can be improvement, security prices by definition don’t incorporate much optimism. But when everyone believes things can only get better forever, it can be hard to find anything that’s reasonably priced.

Bubbles are marked by bubble thinking. Perhaps for working purposes we should say that bubbles and crashes are times when extreme events cause people to lose their objectivity and view the world through highly skewed psychology – either too positive or too negative.Here’s how Kindleberger put it in the first edition ofManias, Panics, and Crashes:

. . . As firms or households see others making profits from speculative purchases and resales, they tend to follow. When the number of firms and households indulging in these practices grows larger, bringing in segments of the population that are normally aloof from such ventures, speculation for profit leads away from normal, rational behavior to what have been described as “manias” or “bubbles.”The word “mania” emphasizes the irrationality; “bubble” foreshadows the bursting.(Emphasis added)

For me, it’s psychological extremeness that marks a bubble. Often, as Kindleberger indicates, it can be inferred from widespread participation in the investment fad of the moment, especially among non-financial types. Legend has it that J.P. Morgan knew there was a problem when the person shining his shoes started giving him stock tips. My partner John Frank says he saw it in 2000, when he heard the dads at his son’s soccer game bragging about the tech stocks they owned, and again in 2006, when a Las Vegas cab driver told him about the three condos he’d purchased. When Mark Twain purportedly said, “history doesn’t repeat itself, but it often rhymes,” it’s this kind of thing he was talking about.

The New, New Thing

If bubble thinking is irrational, what is it that permits investors to get away from rational thinking, like the thrust of a rocket ship that breaks free of the limits imposed by gravity and attains escape velocity? There’s a simple answer:newness. This phenomenon relies on another time-honored investment phrase, “this time is different.”

Bubbles are invariably associated with new developments. There were bubbles in the Nifty Fifty stocks in the 1960s (more on them just below), disc drive companies in the 1980s, TMT/internet stocks in the late 1990s, and sub-prime mortgage-backed securities in 2004-06. These relatively recent manias followed in the tradition of ones like (a) the 1630s craze in Holland over recently introduced tulips and (b) the South Sea Bubble in 1720 England concerning the riches that were sure to ensue from a trading monopoly that the Crown had awarded to the South Sea Company.

In normal circumstances, if an industry’s or a country’s securities are attracting unusually high valuations, investment historians are able to point out that, in the past, those stocks had never sold at more than an x% premium over the average, or some similar metric. In this way,attention to history can serve as a tether, keeping a favored group grounded on terra firma.

But if something’s new, meaning there is no history, then there’s nothing to temper enthusiasm.After all, it’s owned by the brightest people – the ones who are showing up in the headlines and on TV – and they’ve made a fortune. Who’s willing to throw a wet blanket over that party or sit out that dance?

The explanation often lies in Hans Christian Andersen’s storyThe Emperor’s New Clothes. Con men sell the emperor an allegedly gorgeous suit of clothes that only intelligent people can see. But in actuality there is no suit. When the emperor parades around town naked, the citizens are afraid to say they don’t see a suit, since that would mark them as unintelligent. This goes on unchecked until a young boy steps out of the crowd and – in his naivete – points out that the emperor has no clothes. Most people would rather go along with a shared delusion that’s making investors buckets of money than say something to the contrary and appear to be dummies.When a whole market or a group of securities is blasting off and a specious idea is making its adherents rich, few people will risk calling it out.

My Baptism Under Fire

They sayexperience is what you got when you didn’t get what you wanted, and I got my most formative experience at the very beginning of my career. As many of my memo readers know, I joined the equity research department at First National City Bank (now Citi) in September 1969. As was the case with most of the so-called “money-center banks,” Citi invested mainly in the “Nifty Fifty”– the stocks of the best and fastest-growing companies in America. These companies were considered to be so good that (a) nothing bad could ever happen and (b) there was no price too high for their stocks . . . literally.

Three factors contributed to investors’ fascination with these stocks. First, the U.S. economy grew strongly in the post-World War II period. Second, these companies benefitted from their involvement with areas of innovation such as computers, drugs, and consumer products. And third, they represented the first wave of “growth stocks,” a new investment style that separately became a fad in itself. The Nifty Fifty were the object of the first big bubble in roughly 40 years, and since there hadn’t been one for so long, investors had forgotten what a bubble looks like. As a result of the popularity that was conferred on them, if you bought these stocks on the day I started work and held them tenaciously for five years, you lost well over 90% of your money . . . in the best companies in America. What happened?

The Nifty Fifty had been put on a pedestal, and investors get hurt when something falls from it. The stock market as a whole declined by about half in 1973-74. And it turned out these stocks had been selling at prices that actually were too high; in many cases, their price/earnings ratios fell from the range of 60 to 90 to the range of 6 to 9 (that’s the easy way to lose 90%). Further, bad things actually did happen to several of the companies in fundamental terms.

My early brush with a genuine bubble caused me to formulate some guiding principles that carried me through the next 50-odd years:

It’s not what you buy, it’s what you pay that counts.

Good investing doesn’t come from buying good things, but from buying things well.

There’s no asset so good that it can’t become overpriced and thus dangerous, and there are few assets so bad that they can’t get cheap enough to be a bargain.

Things Can Only Get Better

The bubbles I’ve lived through have all involved innovations, as I noted above, and many of those were either overestimated or not fully understood. The attractions of a new product or way of doing business are usually obvious, but the potholes and pitfalls are often hidden and only discovered in trying times. A new company may completely outclass its predecessors, but investors who by definition lack experience in this new field often fail to grasp that even a bright newcomer can be supplanted. The disrupters can be disrupted, whether by skillful competitors or even newer technologies.

In my early decades in business, technology seemed to evolve gradually. Computers, drugs, and other innovative products improved a little at a time. But in the 1990s, innovation came in a big rush. When Oaktree was founded in 1995, I insisted that I could get by with just WordPerfect for word processing and Lotus 1-2-3 for spreadsheets. But when we moved to our current office in 1998, I threw in the towel and let our IT team install e-mail and the internet (and, of course, WordPerfect gave way to Word, and Lotus 1-2-3 to Excel). At the time, investors were sure “the internet will change the world.” It certainly looked that way, and that assumption prompted tremendous demand for everything internet-related. E-commerce stocks went public at seemingly high prices and then tripled the first day. There was a real goldrush.

There’s usually a grain of truth that underlies every mania and bubble. It just gets taken too far.It’s clear that the internet absolutely did change the world – in fact, we can’t imagine a world without it. But the vast majority of internet and e-commerce companies that soared in the late ’90s bubble ended up worthless. When a bubble burst in my early investing days,The Wall Street Journalwould run a box on the front page listing stocks that were down by 90%. In the aftermath of the TMT Bubble, they’d lost 99%.

When something is on the pedestal of popularity, the risk of a decline is high.When people assume – and price in – an expectation that things can only get better, the damage done by negative surprises is profound. When something is new, the competitors and disruptive technologies have yet to arrive. The merit may be there, but if it’s overestimated it can be overpriced, only to evaporate when reality sets in. In the real world, trees don’t grow to the sky.

The foregoing discussion centered on the risk of overestimating fundamental strength. But optimism surrounding the power and potential of the new thing often causes the error to be compounded through the assignment of too high a stock price.

As mentioned above, for something new, there by definition is no historical indicator of what an appropriate valuation might be.

Further, the companies’ potential hasn’t yet been turned into steady-state profits, meaning the thing that’s being valued is conjectural. In the TMT Bubble, the companies didn’t have earnings, so p/e ratios were out. And as startups, they often didn’t have revenues to value. As a result, new metrics were invented, and trusting investors ended up paying a multiple of “clicks” or “eyeballs,” regardless of whether these measurables could be turned into revenues and profits.

Since bubble participants can’t imagine there being any downside, they tend to award valuations that assume success.

In fact, it’s not infrequent for investors to treat all contenders in a new field as likely to succeed, whereas in reality only a few may thrive, or perhaps even survive.

Ultimately, with a really hot new thing, investors can adopt what I call “a lottery ticket mentality.” If a successful startup in a hot field can return 200x, it’s mathematically worth investing in even if it’s only 1% likely to succeed. And what doesn’t have a 1% likelihood of success? When investors think this way, there are few limits on what they’ll support or the prices they’ll pay.

Obviously, investors can get caught up in the race to buy the new, new thing. That’s where the bubble comes in.

What’s the Appropriate Price to Pay for a Bright Future?

If there’s a company for sale that will make $1 million next year and then shut down, how much would you pay for it? The right answer is a little less than $1 million, so that you’ll have a positive return on your money.

But stocks are priced at “p/e multiples” – that is,multiplesof next year’s earnings. Why? Because presumably they won’t earn profits for just one year; they’ll go on making money for many more. When you buy a stock, you buy a share of the company’s earnings every year into the future. The price of the S&P 500 has averaged roughly 16 times earnings in the post-World War II period. This is typically described as meaning “you’re paying for 16 years of earnings.” It’s actually more than that, though, because the process of discounting makes $1 of profit in the future worth less than $1 today. The current value of a company is the discounted present value of its future earnings, so a p/e ratio of 16 means you’re paying for more than 20 years of earnings (depending on the interest rate at which future earnings are discounted).

In bubbles, hot stocks sell for considerably more than 16 times earnings. Remember the 60 to 90 times for the Nifty Fifty! Investors in 1969 were paying for companies’ earnings – even after giving them credit for significant earnings growth – many decades into the future. Did they do so consciously and analytically? Not that I recall. Investors thought of a p/e ratio as just a number . . . if they thought about it at all.

Today’s S&P-leading companies are, in many ways, much better than the best companies of the past. They enjoy massive technological advantages. They have vast scale, dominant market shares, and thus above average profit margins. And since their products are based on ideas more than metal, the marginal cost of producing an additional unit is low, meaning their marginal profitability is unusually high.

The further good news is that today’s leaders don’t trade at the p/e ratios investors applied to the Nifty Fifty. Perhaps the sexiest of the seven is Nvidia, the leading designer of chips for artificial intelligence. It’s current multiple of future earnings is in the low 30s, depending on which earnings estimate you believe. While double the average post-war p/e on the S&P 500, that’s cheap compared to the Nifty Fifty. But what does a multiple in the 30s imply? First, that investors think Nvidia will be in business for decades to come. Second, that its profits will grow throughout those decades. And third, that it won’t be supplanted by competitors.In other words, investors are assuming Nvidia will demonstratepersistence.

But persistence isn’t easily achieved, especially in high-tech fields where new technologies can arise and new competitors can leapfrog incumbents. It’s worth noting, for example, that only about half the Nifty Fifty (as enumerated by Wikipedia – there is no agreed-on list) are in the S&P 500 today (that figure undoubtedly looks worse than the reality, since mergers and acquisitions caused some of the old names to disappear, not failures). Leading lights of 1969 that are missing from the S&P 500 today include Xerox, Kodak, Polaroid, Avon, Burroughs, Digital Equipment, and my favorite, Simplicity Pattern (how many people make their own clothing these days?).

Another indication of how hard it is to persist can be seen in the names of the top twenty S&P 500 companies. At the beginning of 2000, according to finhacker.cz, these twenty companies were the most heavily represented in the index:

Microsoft

Merck

General Electric

Coca-Cola

Cisco Systems

Procter & Gamble

Walmart

AIG

Exxon Mobil

Johnson & Johnson

Intel

Qualcomm

Citigroup

Bristol-Myers Squibb

IBM

Pfizer

Oracle

AT&T

Home Depot

Verizon

At the beginning of 2024, however, only six of them were still in the top twenty:

Microsoft

Johnson & Johnson

Walmart

Procter & Gamble

Exxon Mobil

Home Depot

Importantly, of today’s Magnificent Seven, only Microsoft was in the top twenty 24 years ago.

In bubbles, investors treat the leading companies – and pay for their stocks – as though the firms are sure to remain leaders for decades. Some do and some don’t, but change seems to be more the rule than persistence.

Whole Markets

The greatest bubbles usually originate in connection with innovations, mostly technological or financial, and they initially affect a small group of stocks. But sometimes they extend to whole markets, as the fervor for a bubble group spreads to everything.

In the 1990s, the S&P 500 was borne aloft by (a) the continuing decline of interest rates from their inflation-fighting peak in the early 1980s and (b) the return of investor enthusiasm for stocks that had been lost in the traumatic ’70s. Technological innovation and the rapid earnings growth of the high-tech companies added to the excitement. And an upswing in the popularity of stocks was reinforced by new academic research showing there had never been a long period in which the S&P 500 failed to outperform bonds, cash, and inflation. The combination of these positive factors caused the annual return on the index to average more than 20% for the decade. I’ve never seen another period like it.

I always say the riskiest thing in the world is the belief that there’s no risk.In a similar vein, heated buying spurred by the observation that stocks had never performed poorly for a long period caused stock prices to rise to a point from which they were destined to do just that.In my view, that’s George Soros’s investment “reflexivity” at work. Stocks were tarred in the bursting of the TMT Bubble, and the S&P 500 declined in 2000, 2001, and 2002 for the first three-year decline since 1939, during the Great Depression.As a consequence of this poor performance, investors deserted stocks en masse, causing the S&P 500 to have a cumulative return ofzerofor the more than eleven years from the bubble peak in mid-2000 until December 2011.

Lately, I’ve been repeating a quote I attribute to Warren Buffett: “When investors forget that corporate profits grow about 7% per year they tend to get into trouble.” What this means is that if corporate profits grow at 7% a year and stocks (which represent a share in corporate profits) appreciate at 20% a year for a while, eventually stocks will be so highly priced relative to their earnings that they’ll be risky. (I recently asked Warren for a source on the quote, and he told me he never said it. But I think it’s great, so I keep using it.)

The point is that when stocks rise too fast – out of proportion to the growth in the underlying companies’ earnings – they’re unlikely to keep on appreciating. Michael Cembalest has another chart that makes this point. It shows that prior to two years ago, there were only four times in the history of the S&P 500 when it returned 20% or more for two years in a row. In three of those four instances (a small sample, mind you), the index declined in the subsequent two-year period. (The exception was 1995-98, when the powerful TMT bubble caused the decline to be delayed until 2000, but then the index lost almost 40% in three years.)

In the last two years, it’s happened for the fifth time. The S&P 500 was up 26% in 2023 and 25% in 2024, for the best two-year stretch since 1997-98. That brings us to 2025. What lies ahead?

The cautionary signs today include these:

the optimism that has prevailed in the markets since late 2022,

the above average valuation on the S&P 500, and the fact that its stocks in most industrial groups sell at higher multiples than stocks in those industries in the rest of the world,

the enthusiasm that is being applied to the new thing of AI, and perhaps the extension of that positive psychology to other high-tech areas,

the implicit presumption that the top seven companies will continue to be successful, and

the possibility that some of the appreciation of the S&P has stemmed from automated buying of these stocks by index investors, without regard for their intrinsic value.

Finally, while I’m at it, although it’s not directly related to stocks, I have to mention Bitcoin. Regardless of its merit, the fact that its price rose 465% in the last two years doesn’t suggest an overabundance of caution.

I often find that, just as I’m about to release a memo for publication, something comes along that demands inclusion, and it has happened again. On the last day of 2024, I received something from two sources that fits that description:

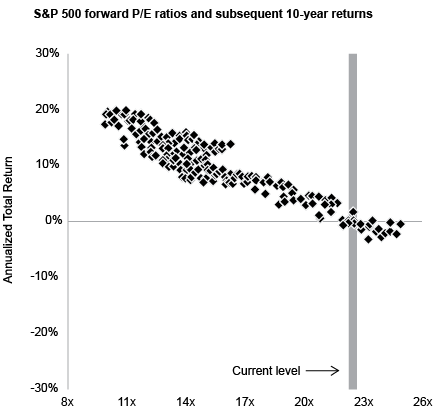

The graph, from J.P. Morgan Asset Management, has a square for each month from 1988 through late 2014, meaning there are just short of 324 monthly observations (27 years x 12). Each square shows the forward p/e ratio on the S&P 500 at the time and the annualized return over the subsequent ten years. The graph gives rise to some important observations:

There’s a strong relationship between starting valuations and subsequent annualized ten-year returns.Higher starting valuations consistently lead to lower returns, and vice versa.There are minor variations in the observations, but no serious exceptions.

Today’s p/e ratio is clearly well into the top decile of observations.

In that 27-year period, when people bought the S&P at p/e ratios in line with today’s multiple of 22, theyalwaysearned ten-year returns between plus 2% and minus 2%.

In November, a couple of leading banks came out with projected ten-year returns for the S&P 500 in the low- to mid-single digits. The above relationship is the reason.It shouldn’t come as a surprise that the return on an investment is significantly a function of the price paid for it. For that reason, investors clearly shouldn’t be indifferent to today’s market valuation.

You might say, “making plus-or-minus-2% wouldn’t be the worst thing in the world,” and that’s certainly true if stocks were to sit still for the next ten years as the companies’ earnings rose, bringing the multiples back to earth. But another possibility is that the multiple correction is compressed into a year or two, implying a big decline in stock prices such as we saw in 1973-74 and 2000-02. The result in that case wouldn’t be benign.

The above are the things to worry about. Here are the counterarguments:

the p/e ratio on the S&P 500 is high but not insane,

the Magnificent Seven are incredible companies, so their high p/e ratios could be warranted,

I don’t hear people saying, “there’s no price too high;” and

the markets, while high-priced and perhaps frothy, don’t seem nutty to me.

* * *

As I said at the start of this memo, I’m not an equity investor, and I’m certainly no expert on technology.Thus, I can’t speak authoritatively about whether we’re in a bubble. I just want to lay out the facts as I see them and suggest how you might think about them . . . just as I did 25 years ago.

I hope you’ll keep reading for the next 25!

January 2, 2025