All good points made here, but I agree with JGunter's line, specifically the low costs forecasted in Kipoi, is what attracts investors to TGS. This is an exert from an proactive investors article dated 26/11/13 regarding the Judeira resource announcement:

"Analysis

Growth is the name of the game at Tiger Resources and the additional resources at Judeira will be off near-term benefit to the company if it can be processed at Kipoi.

The Judeira resource underlines the prospectivity and sheer scale building at the Kipoi project.

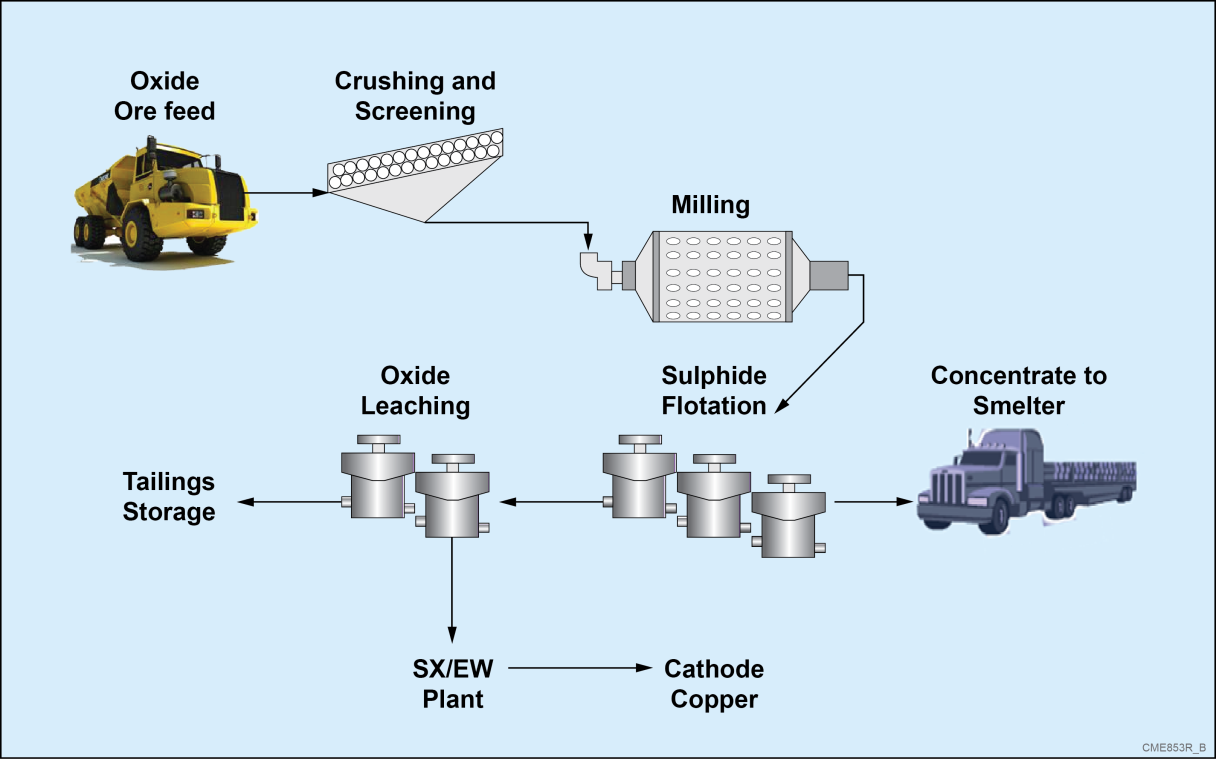

The company’s SXEW plant to produce copper cathode is already 74% completed with a offtake agreement in place.

That there is potential to increase the resource at the Judeira Deposit beyond 6.1 million tonnes grading 1.2%, or 71,000 tonnes of contained copper, further underscores the company’s growth potential.

Kipoi’s expected production of 50,000 tonnes of copper cathode per annum places it within the same peer group as the Pinto Valley Copper Mine in Arizona, Eagle Mine in Michigan and Northparkes Copper and Gold Mine in New South Wales.

Where it stands out is the fact that it has among the lowest cash costs within this peer group, a key reason we believe will draw corporate interest, especially from Chinese or Asian and minerals groups that are actively seeking copper production with low quartile operating costs, high margins and long project life.

Put in perspective, on a gold equivalent basis, Judeira would be a 400,000 ounce gold discovery at 2.5g/t gold, just 6 kilometres from a 300,000 ounce per annum gold plant with OPEX of just $400 an ounce fully funded. and planned to produce 300,000 ounces of gold in 2014.

This highlights the under-valuation of Tiger Resources, perhaps missed by sections of the market."

What makes Kipoi special in my view is the ability to inject Australian management smarts and guidance into a market that provides for low cost labour. This doesn't mean the local labour force is unable to reach the same productivity, in fact the HMS plant and zero injuries is testament to what good management can achieve. Now the SXEW is more complex to operate, but imoh, is not beyond the capacity of the local workforce.

The recent announcement on bringing forward upgrades in the electricity distribution, and the conveyor are aimed at making the process more efficient. As the plant transfers from diesel generated power to grid, more savings can be realised.

Rather than the upgrade to 50kt/pa being a catalyst to SP growth, I think if the forecast opex cost of 70-80c/lb is achieved early based on a nameplate production level or greater will see the SP leave these levels far behind. There is not an ASX peer close to it on opex cost basis, nor one that produces CATHODE (a value added product).

Also potentially missed is the upside, the HMS potentially may offer Phase II SX. It may remove the need to build (in the short term) additional crushing / screening / milling equipment required to lift cathode production. You still need additional heap leach capacity (pads 3-4 are being built now), and electro-winning capacity (need more electrical infrastructure - being upgraded now). I'm hoping there are some savings that can be realised in deferring some items in Phase II by utilising the HMS short term. see below:

gltah

TGS Price at posting:

29.2¢ Sentiment: Buy Disclosure: Held