WSA

August 24, 2021 FAT-AUS-1034AUD$3.04SpeculativeBWSA Snapshot

FY21; nickel prices partially to the rescue and IGO

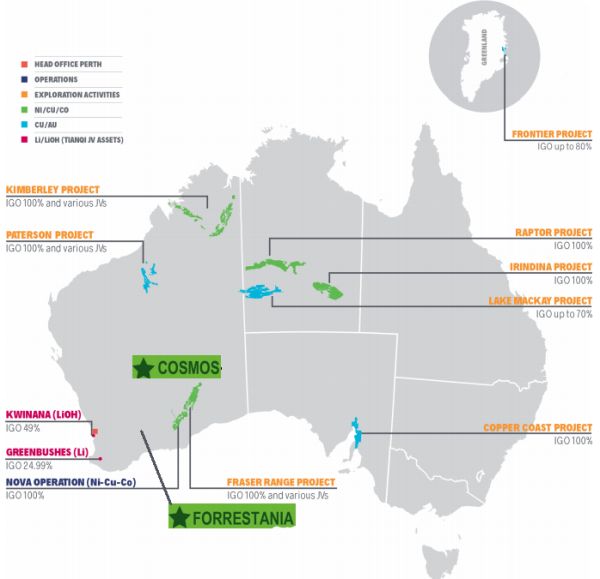

Western Areas, in response to media speculation has announced that it is in preliminary talks with IGO Group (IGO) in relation to a change of control proposal. It is early days in this process and a proposal may not be forthcoming, but we are of the view Western Areas has first class nickel assets that can generate future long-term value as a standalone company. We expect the demand for nickel to rise strongly in the years ahead, propelled by the electric vehicle market. Details of the proposal are yet to be released but we are of the view that the two company’s combined assets would make a compelling story, with a significant production profile in both nickel and lithium. The following image shows the assets of the two companies (Cosmos and Forrestania belong to Western Areas and their positioning is approximate):

Source: IGO/Western Areas

We must wait for the outcome of the talks and of course the value proposition in the IGO merger if it proceeds. No action is required at this time, and we will advise Members of appropriate action when required.

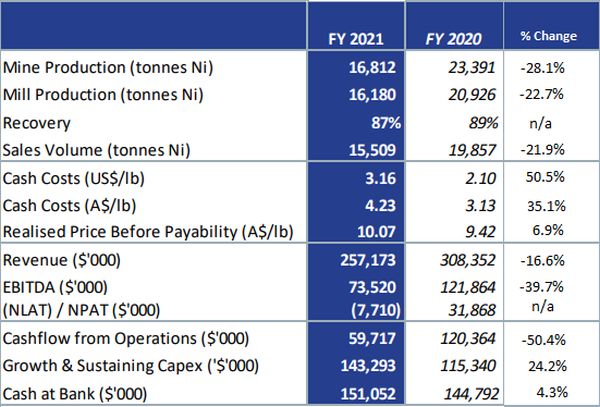

During the merger talks with IGO, Western Areas released its full year financial results for 2021, revealing a loss on the back of a one off tough operational year. Higher nickel prices were a partial offset over the year but were not sufficiently high enough to pullback falls across all Western Areas key financial metrics. The balance sheet, through good management, stepped up the quality structure for 2021. Shareholders took a hit with no dividends paid in 2021. The following table shows the key metrics for Western Areas 2020 results (Ni – nickel, NPAT – net profit after taxation:

Source: Western Areas

We consider the headline result was a poor one but was driven by transitory operating issues in the first half of the year, that are now being rectified. While the lack of a dividend for 2021, exacerbated the negative feel of the result, there were a couple of outstanding features. It is unfortunate that Western Areas was not able to leverage into higher nickel prices for the year.

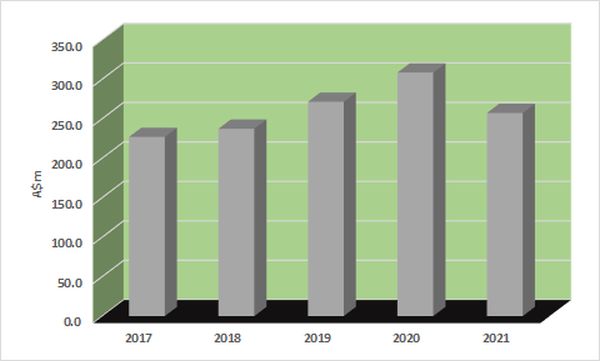

Revenue for 2021 fell 16.6% year-on-year (yoy) to A$257.2 million. The following chart shows annual revenue:

Source: Western Areas

The primary driver of the result was lower production numbers, cushioned partially by higher realised nickel prices for 2021. A standout, but beyond Western Areas control, was its higher realised nickel price before pay-ability, following the reporting of a 6.9% yoy rise, to A$10.07 per pound.

On the nickel price, our long held positive view on the sea change now encompassing and accelerating in the auto industry, and the ongoing growth in stainless steel production, are delivering tailwinds. Government stimulatory programmes is seeing trillions of dollars being committed to infrastructure projects to the benefit of steel and steel derivatives demand. The sea change in the auto industry is the accelerating conversion from carbon powerplants to electric powerplants and the need for batteries. The combination of these two events could generate a real demand storm for nickel in the years ahead.

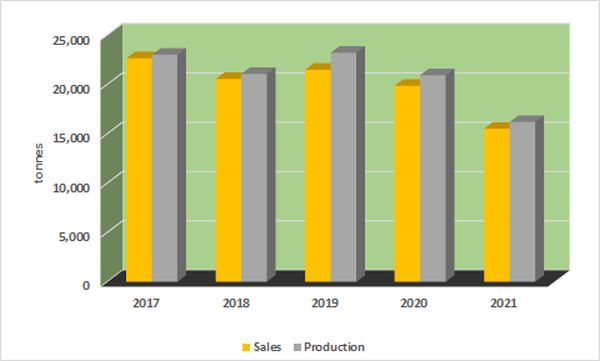

Operations were unfortunately not able to leverage into the higher nickel prices on offer in 2021, following a fall in production. Nickel production fell 28.1% yoy, to 16,812 tonnes. Nickel production came in toward the top end of the revised guidance for 2021 in the range of 16,000 to 17,000 tonnes, from the previous range of 17,000 to 19,000 tonnes. The following chart shows annual nickel sales and production:

Source: Western Areas

Driving this result was falling nickel grades at Flying Fox and Spotted Quoll with Western Areas undertaking transiting activities at both sites. Nickel sales followed production lower in 2021, falling 21.9% yoy, to 15,509 tonnes. Sales unfortunately fell, despite global nickel demand remaining quite robust in 2021.

Western Areas is forecasting nickel production for 2022 to be in the range of 16,000 to 17,000 tonnes.

An outstanding feature was the improvement in operating costs for 2021, following the printing of a 5.9% yoy improvement, to A$161.6 million, as Western Areas continues to optimise costs. Australian Dollar unit costs, unfortunately, went the other way, on falling production numbers, with the reporting of a 35.0% yoy rise, to A$4.23 per pound. This outcome was, disappointingly, toward the top end of the revised Australian Dollar unit cash cost guidance for 2021, of A$3.75 to A$4.25 per pound range. The prior 2021 guidance was in the range of A$3.50 to A$4.00 per pound. In US Dollar terms, unit cash costs rose by 50.5% yoy, to US$3.16 per pound on adverse currency moves.

Western Areas is guiding 2022 Australian Dollar unit cash costs to be in the range A$4.25 to A$4.65 per pound.

Free operating cash flow for 2021 fell on the softer revenue performance and a rise in capital spending (due to Odysseus and Cosmos development activities), with the reporting of a fall of 50.4% yoy, to A$59.7 million.

The balance sheet was the standout in 2021, and this was despite the softer financial result for the year. Western Areas carried no debt as of 30 June 2021. Cash as of 30 June 2021 stood at A$151.1 million, which compares favourably to the A$144.8 million from a year earlier. We consider Western Areas to be well resourced and we have no concerns over the structure of its balance sheet.

The poor financial performance for 2021 buried the dividend for the year, which was disappointing. The Board refrained from paying a 2021 dividend compared to a full year dividend in 2020 of A2.0 cents per share.

The full year result for 2021 could have been a good lead in for IGO to propose a merger with Western Areas. Although the headline numbers were average for 2021, the underlying development activities and strong Western Areas balance sheet really are a feature and may require a good premium to get hold of these.

With a very strong balance sheet to fund exploration and development and prospective ground at its Odysseus mine and Cosmos project, the ingredients required to generate future shareholder value are all in place. The final key for us, going forward, is our positive view on the nickel price and Western Areas ability to leverage into our scenario of higher nickel prices over 2021 and beyond.

Despite the current M&A action, we believe Western Areas is a sound standalone operation and consequently, and despite the share price bounce, we continue to recommend Western Areas as a buy for Members with no exposure to the stock.