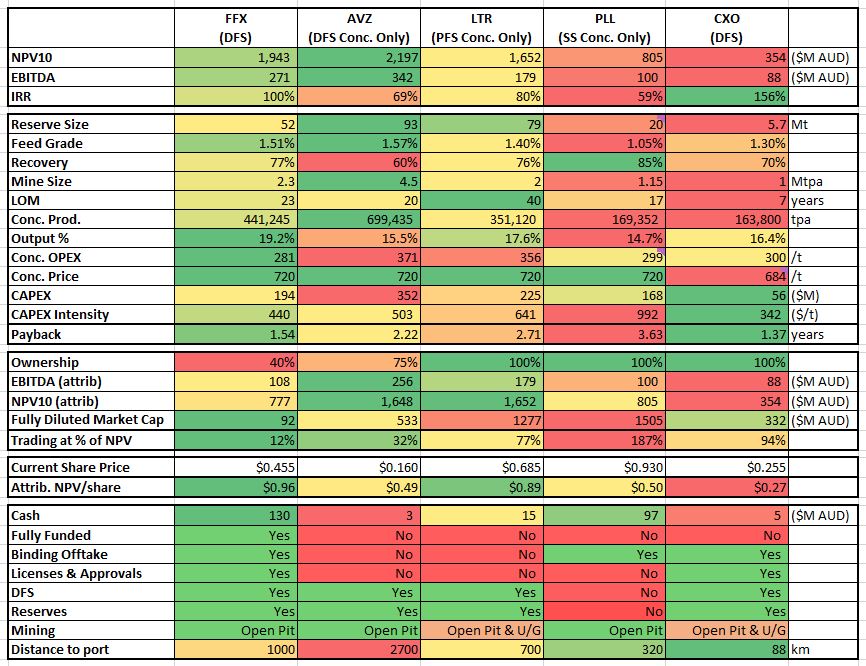

Now that FFX has well and truly earnt the title of developer, I think it’s time to revive the infamous comparison table against our closest peer explorers & developers.

With this deal, we are now completely green lit to production. Fully funded, with binding offtake. This should unlock significant value in line with peers who aren’t nearly as advanced, yet trade at multiples higher.

In my market cap assumption, I have assumed that 25% of FFX’s current MC is attributable to the lithium (around $0.10 of the current share price), however I would say that it is likely even less than that.

According to my model, looking at peer valuations, the ~$0.10 of the SP attributable to Goulamina has scope to go up to $0.96 (100% of NPV) and beyond – depending on where the market values the project as our peers are valued between 40 - 167% of the NPV calculated by my model.

Given FFX's GREEN light to production, we should expect to be within the upper end of the bracket, so perhaps $0.80 would be an appropriate initial target (for the lithium).

Then add $0.70 (Sprott's target for the gold) to that, to get a

complete share price target of $1.50/share.

I will have to add spodumene producers to the table next, as that is what we will soon be compared against.

Producers obviously trade even higher again, for example PLS with a MC >$4B who are currently producing 330ktpa vs FFX to produce ~450ktpa at a lower cost/ton… $4B would be a nice target for us…

This model of course doesn't factor in mine upgrades i.e. increasing plant throughput from 2.3Mtpa to 5Mtpa, or participation in secondary processing (lithium carbonate & hydroxide) which could very likely be on the cards now we are partnered with Ganfeng to supply directly to Europe...