Hard to be bearish on residential property

From the fixed rate mortgage cliff distress sales (that still haven’t happened), to the next pundit’s prediction that the Australian property bubble is about to burst, there is no shortage of bearish reading material this year. Putting the noise to the side, we believe the prospective return profile of the residential property market in Australia is strong because of an ongoing demand supply imbalance.

Most houses in Australia have commodity-like features, that is, are easily replaced when the development profit equation favours new supply. As such, we view the typical commodity property cycle through the below framework.

Source: Quay Global Investors

This current problem is the development equation generally doesn’t work. The cost of developing residential property in Australia is high by global standards. This is largely due to significant government-related taxes and charges, tight regulations, skilled labour shortages and persistent building material inflation.

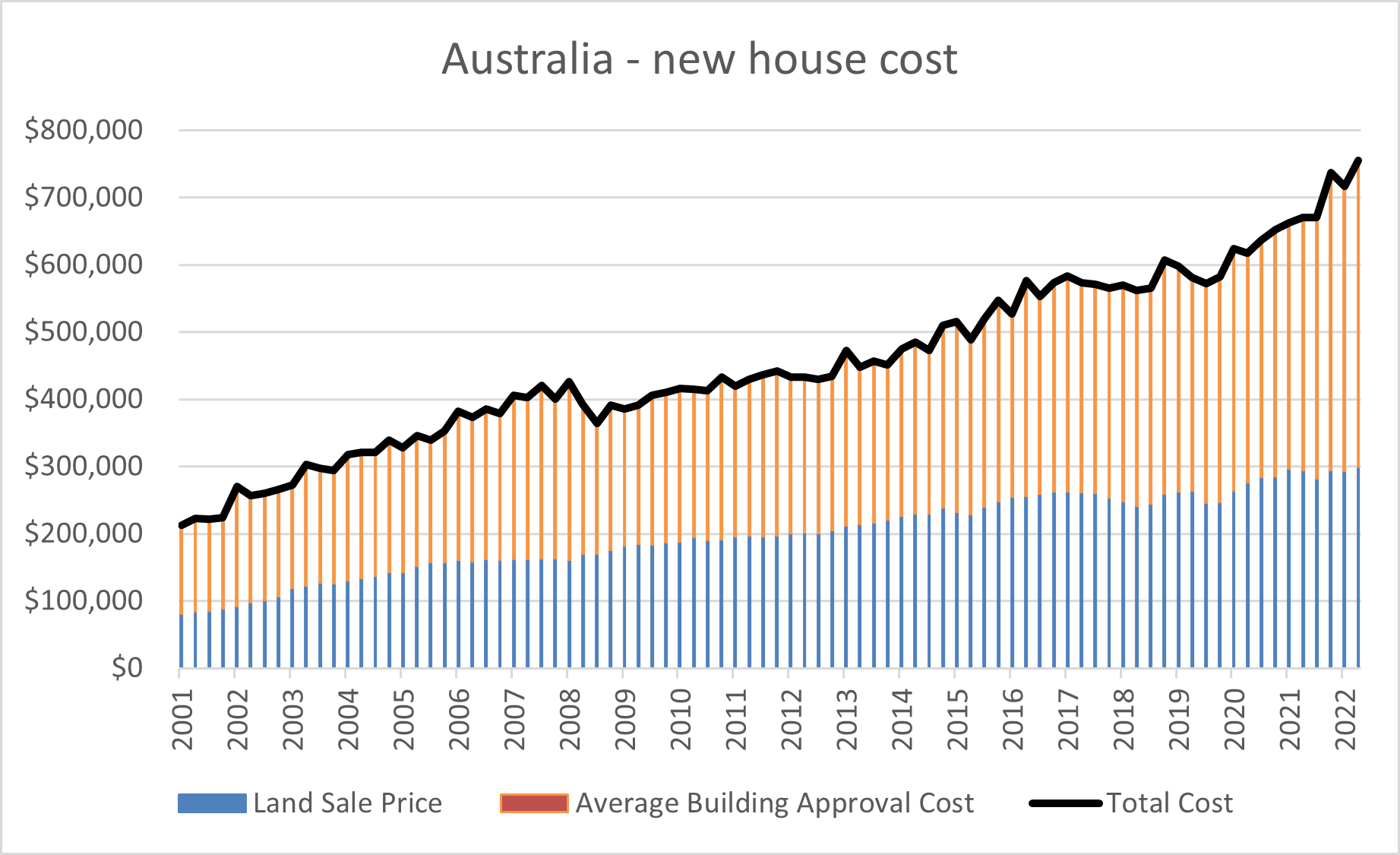

Since 2001, the cost of developing a new house in Australia has increased 6.1% per annum, accelerating to 8% p.a. since June 2019.Source: Jarden, ABS, HIA, Quay Global Investors

The RBA’s recent rate hiking regimen has only added fuel to this fire, with the cost of funding blowing previously plausible feasibilities out of the water. In short, the decisions by the RBA (and other central banks around the world), are putting a halt on new supply, just at a time when Australia needs it most.

The Australian housing ‘crisis’ will not be solved until the cost of supplying the market is lowered, or dwelling prices rise above replacement cost (very high).The challenges with supplying the housing market are evidenced in the sustained drop in new supply, now down 45% from the 2021 peak.

Source: ABS, Quay Global Investors

This constrained supply has been met with robust demand, which is being evidenced in both the ownership and rental residential markets. In the for-sale market, house prices have risen 4.9% since February (Core Logic), and in the rental market we have seen a sustained drop in the vacancy rate and strong rental growth (below).

Source: ABS, Quay Global Investors

Put simply, until developers are financially incentivised to build again, these conditions will remain, and likely gain momentum. For long-term investors, it's hard to be bearish Australian residential right now.

Source : C. Bedingfield, Quay Global Investors

Update on the supply/demand situation, page-281

-

- There are more pages in this discussion • 41 more messages in this thread...

You’re viewing a single post only. To view the entire thread just sign in or Join Now (FREE)

Featured News

Featured News

The Watchlist

CCO

THE CALMER CO INTERNATIONAL LIMITED

Anthony Noble, CEO

Anthony Noble

CEO

SPONSORED BY The Market Online